Updating fleet insurance is the formal process of modifying an active commercial policy through endorsements, re-quoting, or carrier changes to reflect accurate vehicle, driver, and operational details. When your fleet changes and your policy does not, you face coverage gaps, compliance failures, and potential contract breaches. The fleet insurance update process is not optional paperwork. It is a critical operational checkpoint that protects your business financially and legally. This guide covers exactly what triggers a policy change, how to execute the fleet insurance update process correctly, and how to avoid the most costly mistakes fleet managers make.

How to update fleet insurance: what triggers a change

Fleet insurance updates are required any time your vehicles, drivers, or operational details change in a way that affects your risk profile. Adding a truck to your fleet, hiring a new driver, changing the garaging location of a vehicle, or expanding your operating radius all require a formal policy endorsement. Removing a vehicle or driver also requires an update, since carrying coverage on assets you no longer operate wastes premium dollars and creates administrative confusion.

The specific data your insurer or broker needs to process an endorsement includes the vehicle identification number (VIN), year, make, model, gross vehicle weight rating (GVWR), intended use, garaging location, and current market value. For driver additions, you will need the driver’s license number, date of birth, years of commercial driving experience, and Motor Vehicle Record (MVR). Missing vehicle or driver data can delay endorsement processing by days, leaving a newly acquired truck operating without confirmed coverage.

One detail many fleet managers overlook is the newly acquired vehicles provision. Most commercial auto policies include a short grace period, often around 30 days, during which a newly purchased vehicle may carry temporary coverage while the endorsement processes. However, some policies carry no grace period at all. Treating zero days as your guaranteed safe window is the only reliable standard. Add every new vehicle to your policy before it moves.

Changes in how you use your vehicles also matter. A truck that shifts from local delivery to long-haul interstate routes represents a fundamentally different risk. Failing to report that change means your coverage may not respond correctly if a claim occurs. Reviewing your fleet coverage options when operational use shifts is just as important as reporting a new vehicle.

How to execute the endorsement process without gaps

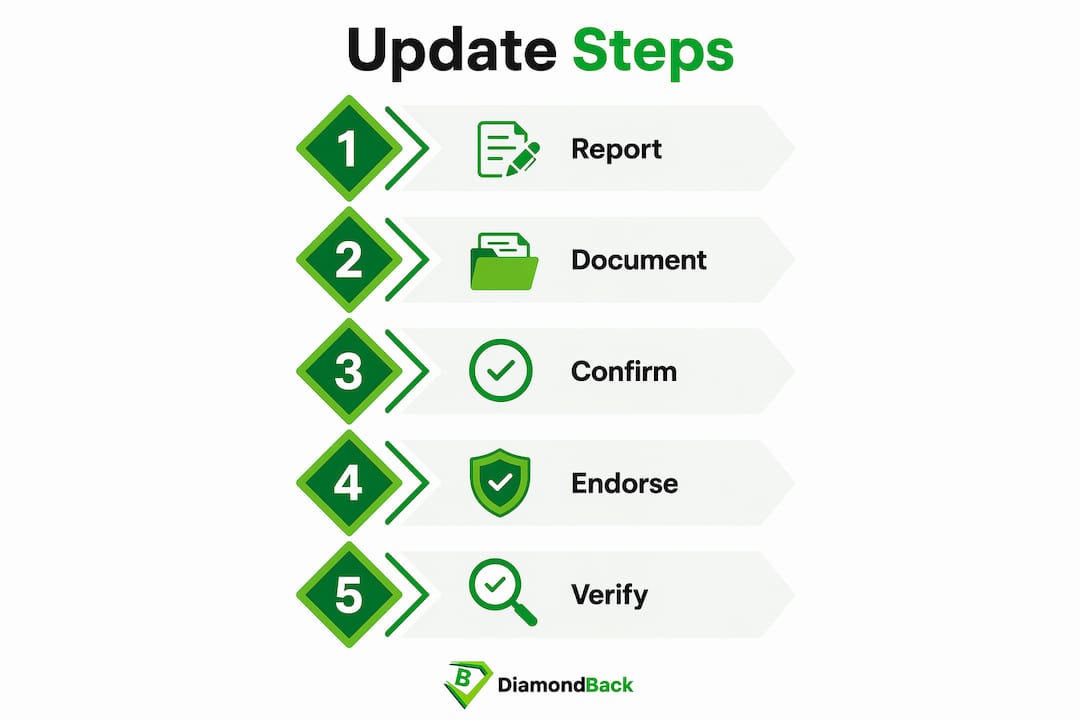

The fleet insurance update process follows a clear sequence, and skipping any step creates risk. Here is how to move through it correctly.

-

Contact your insurer or broker the same week the change occurs. Delays compound. An endorsement effective date is not backdated to the vehicle purchase date or driver hire date. Endorsement effective dates mark when coverage actually begins, so every day you wait is a day of potential uninsured exposure.

-

Submit complete and accurate vehicle and driver information. Use the data checklist from the previous section. Incomplete submissions are the single most common cause of endorsement delays. Some states also require you to sign uninsured motorist coverage election forms when adding vehicles, and missing those forms can delay the endorsement’s effective status entirely.

-

Confirm the updated declarations page. The declarations page is the document your lenders, lessors, and contract holders rely on as proof of coverage. An outdated declarations page that does not reflect added vehicles or drivers will fail compliance checks. Request the updated declarations page in writing once the endorsement is processed.

-

Request a new certificate of insurance (COI) immediately after the endorsement is confirmed. Certificates of insurance reflect coverage at the time of issuance and do not automatically update when your policy changes. Re-issuance is required after every endorsement or limit change. Depending on the complexity of the change, COI delivery can take hours or even days.

-

Distribute updated COIs to all relevant stakeholders. Freight brokers, shippers, lessors, and government agencies often require current COIs to authorize operations. Sending an updated certificate proactively keeps your contracts in good standing.

-

Evaluate telematics enrollment for new vehicles. Some carriers activate premium discounts immediately upon telematics device enrollment during the endorsement process. If your carrier offers this, enroll new vehicles at the same time you submit the endorsement request.

Pro Tip: Set a standing internal rule that no new vehicle operates on a public road until you have written confirmation of the endorsement effective date from your insurer. A verbal assurance is not coverage.

What are the most common pitfalls when modifying fleet insurance?

The most expensive mistakes in the fleet insurance update process come from timing errors and documentation gaps. Understanding these pitfalls before they happen is how you protect your operation.

Relying on grace periods without written confirmation is the most common error. Many fleet managers assume the 30-day newly acquired vehicles provision applies automatically. It does not apply universally, and even when it does, it is not a substitute for a confirmed endorsement. Operate on the assumption that the grace period may not exist until your insurer confirms otherwise in writing.

Failing to sequence COI delivery with endorsement completion creates hidden compliance failures. COIs do not self-update after policy modifications, and this gap often leads to contract violations that fleet managers discover only when a shipper or lessor flags the issue. Build COI re-issuance into your standard endorsement workflow, not as an afterthought.

Assuming coverage changes are retroactive is another costly misunderstanding. If a driver causes an accident before you report them to your policy, the claim may be denied. Coverage begins on the endorsement effective date, not the hire date. This applies equally to vehicles.

Starting your fleet insurance review 60 to 90 days before policy expiration gives you the best leverage with insurers and the most time to correct documentation errors before they become compliance problems. Source: rmcgp.com

When changing fleet insurance providers, the sequencing rule is absolute. Your new policy must be active before your old policy cancels. New policy activation before cancellation is the only way to avoid a coverage gap during the transition. Coordinate endorsements and COI deliveries so every contract holder receives valid, matching documentation without interruption.

Endorsements, re-quoting, or switching carriers: which approach fits your situation?

Not every fleet insurance change requires the same method. Choosing the right approach depends on the scale of the change and your current policy’s fit for your operation.

| Situation | Best Approach | Key Consideration |

|---|---|---|

| Adding or removing 1 to 3 vehicles or drivers | Midterm endorsement | Fastest method; updates declarations page without disrupting the policy term |

| Fleet grows by 25% or more, or operational use shifts significantly | Re-quote with current or new carrier | Endorsements for small changes, re-quoting for major growth or risk profile shifts |

| Premiums are uncompetitive or coverage no longer fits | Carrier switch at renewal | New policy must activate before old policy cancels to avoid gaps |

| Significant operational expansion into new states or cargo types | Re-quote or carrier switch | Existing endorsements may not accommodate new regulatory requirements |

Midterm endorsements handle the routine work of keeping your policy current. They are the right tool for incremental fleet changes. Re-quoting becomes necessary when your business has grown enough that your current policy structure no longer reflects your actual risk. A customized insurance program built around your current fleet size and operations will almost always outperform a heavily endorsed legacy policy.

Switching carriers is the most complex option and requires the most careful timing. The administrative burden of changing fleet insurance providers is real, but staying with a carrier whose pricing or coverage no longer serves your fleet is more expensive in the long run. Use the carrier switch as an opportunity to review your liability limits, physical damage coverage, and any gaps that have accumulated through years of incremental endorsements.

Pro Tip: Before closing out any fleet insurance update, verify three things in writing: the endorsement effective date, the updated declarations page, and the matching COI. Simply asking your broker to update the policy is not enough. Verification is what protects you.

Key takeaways

Updating fleet insurance correctly requires prompt reporting, confirmed endorsement effective dates, and proactive COI re-issuance after every policy change.

| Point | Details |

|---|---|

| Report changes immediately | Contact your insurer the same week any vehicle or driver change occurs to secure the correct endorsement effective date. |

| Verify, do not assume | Confirm endorsement completion, updated declarations pages, and new COIs in writing before considering the update complete. |

| COIs require re-issuance | Certificates of insurance do not update automatically; request a new COI after every endorsement or coverage change. |

| Sequence carrier switches carefully | Activate your new policy before canceling the old one to prevent any gap in coverage during the transition. |

| Start renewals 60 to 90 days early | Early preparation gives you negotiating leverage and time to correct documentation before compliance deadlines arrive. |

Why fleet insurance updates deserve the same discipline as vehicle maintenance

I have seen fleet managers who run tight, well-organized operations treat insurance updates as an afterthought. They track every oil change and tire rotation on a spreadsheet, but they add a new truck to the road and notify their broker two weeks later, if at all. That gap is not just a compliance risk. It is an uninsured operation.

The mindset shift that actually works is treating every vehicle acquisition and every driver hire as a two-part process. Part one is the operational step: purchase the truck, sign the employment agreement. Part two is the insurance step: submit the endorsement request before the vehicle or driver goes to work. When you wire those two steps together in your onboarding process, coverage gaps stop happening by default.

Documentation discipline matters just as much. Reviewing your fleet insurance coverage annually is good practice, but the real protection comes from maintaining a current declarations page and distributing updated COIs every time your policy changes. Freight brokers and shippers will not wait for you to sort out paperwork after a load is already on the truck.

The other thing worth saying plainly is that early renewal preparation is not just about avoiding surprises. It is about leverage. When you arrive at renewal with clean driver records, organized fleet data, and 60 to 90 days of lead time, you are negotiating from a position of strength. Carriers respond to prepared clients with better terms. Rushed renewals produce rushed pricing, and rushed pricing is almost never favorable.

— Vladimir

How Diamondbackins simplifies your fleet insurance updates

Managing a fleet means you cannot afford to spend hours chasing endorsements or waiting on certificates of insurance. Diamondbackins gives fleet managers and business owners direct access to instant quotes from multiple top-rated commercial carriers, so you can compare coverage options and secure the right policy without the delays of traditional brokers.

Whether you are adding vehicles mid-term, renewing trucking insurance before your expiration date, or switching to a carrier that better fits your current operation, Diamondbackins makes the process fast and transparent. The platform delivers instant policy documentation, including updated certificates of insurance, so your stakeholders always have what they need. Get your instant fleet insurance quote today and keep your fleet covered without the administrative friction.

FAQ

What does it mean to update fleet insurance?

Updating fleet insurance means formally modifying your commercial auto policy through a policy endorsement to reflect changes in vehicles, drivers, coverage limits, or operational details. The update produces a revised declarations page and requires a new certificate of insurance to be issued to relevant stakeholders.

How long does a fleet insurance endorsement take?

Endorsement processing time varies by carrier and the complexity of the change, but most routine additions or removals complete within one to three business days. COI delivery after an endorsement can take additional hours or days depending on the carrier.

Can I add a vehicle to my fleet policy before I buy it?

No. Endorsements require confirmed vehicle details, including the VIN, which is only available after purchase. You should submit the endorsement request on the same day you take ownership to minimize any gap between acquisition and confirmed coverage.

What happens if I forget to update my fleet insurance after adding a driver?

If a driver not listed on your policy is involved in an accident, your insurer may deny the claim. Coverage under a commercial fleet policy applies from the endorsement effective date, not the driver’s hire date, so prompt reporting is critical.

When should I re-quote instead of just updating my current policy?

Re-quoting makes sense when your fleet has grown by 25% or more, your operational use has shifted significantly, or your current premiums no longer reflect competitive market rates. Midterm endorsements handle incremental changes, but major growth or risk profile shifts warrant a full coverage review.