Adequate cargo coverage is defined as insurance that protects the full commercial value of your shipment against loss, damage, theft, and transit disruptions beyond what your carrier’s liability provides. For freight operators and businesses moving goods across state lines or international borders, relying on carrier liability alone is a calculated risk that rarely pays off. The FMCSA minimum for general freight sits at just $5,000, a figure that covers a fraction of most real shipment values. Understanding why secure adequate cargo coverage matters is the difference between a recoverable loss and a business-threatening financial gap.

Why carrier liability limits leave you financially exposed

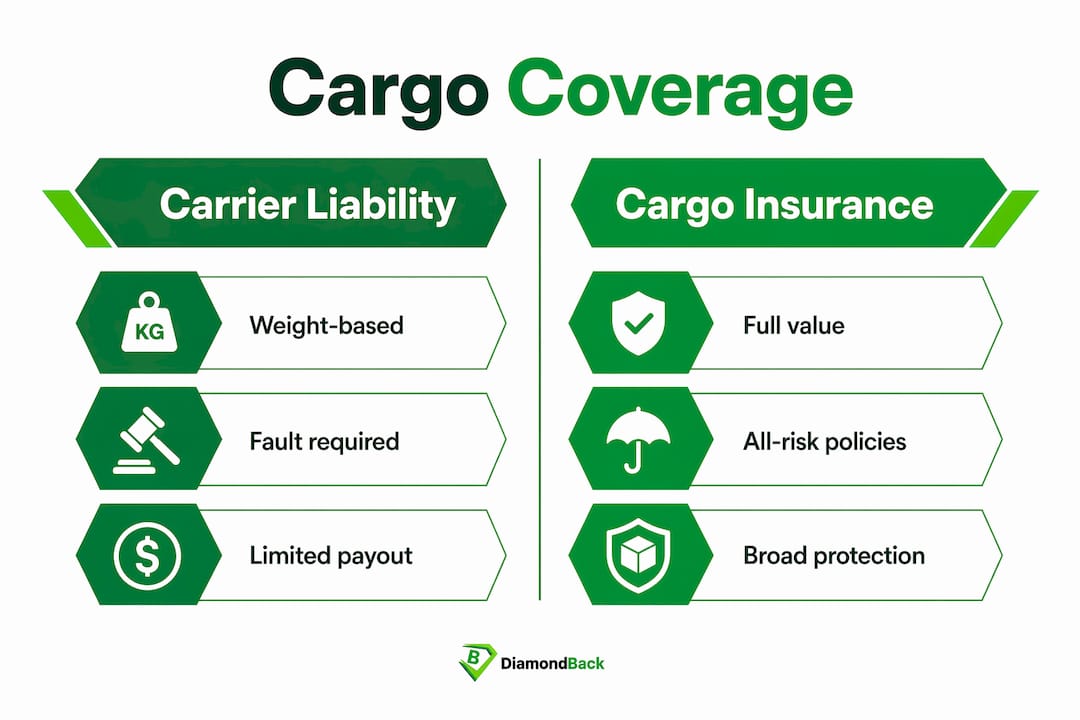

Carrier liability is not cargo insurance. This distinction costs businesses millions of dollars every year, yet it remains one of the most misunderstood points in freight logistics.

Under international conventions like the Hague-Visby Rules and the Montreal Convention, carrier liability caps are weight-based, not value-based. A shipment of precision electronics weighing 500 kilograms might be worth $80,000, but the carrier’s maximum payout could be calculated at roughly $9 per kilogram, leaving you with $4,500 on an $80,000 loss. That gap is your problem, not the carrier’s.

The numbers at the domestic level are equally stark. 73% of truckers are underinsured, operating under the FMCSA’s $5,000 minimum that was never designed to reflect current freight values. This means the carrier hauling your load may have coverage that pays out less than the cost of a single pallet of consumer goods. The risk lands squarely on the shipper.

Beyond the payout gap, the claims process itself creates financial strain. Standard carrier liability claims can take up to 180 days to settle, and that timeline assumes no dispute. When a carrier contests fault, you may need to prove negligence in court before seeing a dollar. For businesses managing cash flow across multiple shipments, a six-month wait for partial reimbursement is not a minor inconvenience. It is a liquidity crisis.

| Risk Factor | Carrier Liability | Cargo Insurance |

|---|---|---|

| Payout basis | Weight-based (cents per kg) | Full declared commercial value |

| Fault requirement | Must prove carrier negligence | Pays regardless of fault |

| Settlement timeline | Up to 180 days | As fast as 30 days with bespoke policy |

| Theft coverage | Limited or excluded | Covered under All-Risk policies |

| General Average exposure | Not covered | Covered with proper endorsement |

Pro Tip: Review every carrier contract before signing. Most contain liability limitation clauses that reduce payout well below even the standard weight-based cap. Your cargo insurance policy should explicitly cover the gap between carrier liability and full cargo value.

What does adequate cargo insurance actually cover?

Cargo insurance, specifically Motor Truck Cargo (MTC) insurance and All-Risk marine policies, covers the commercial value of freight during transit rather than the equipment carrying it. MTC insurance is the coverage most brokers require carriers to hold before accepting a load, with typical broker-mandated limits ranging from $100,000 to $500,000 depending on freight type and value.

All-Risk policies provide the broadest protection available. They cover theft, fire, collision damage, water damage, and loading or unloading accidents. They also address General Average, a maritime law principle that requires all cargo owners aboard a vessel to share salvage costs when the captain must sacrifice cargo to save the ship. Without cargo insurance, your goods can be held by the carrier until you post a substantial cash bond, regardless of whether your specific cargo was jettisoned.

Every policy carries exclusions you need to understand before a loss occurs. Standard exclusions include inherent vice (goods that deteriorate by their own nature), inadequate packaging, losses from delay, and mysterious disappearance without evidence of theft. Cargo coverage does not apply before pickup or after delivery, so warehouse storage gaps require separate inland marine coverage.

One critical distinction that many businesses miss: marine policies do not automatically cover inland transit risks. Multi-modal policy extensions must be explicitly added to close the gap between port and final destination. A shipment that moves by sea and then by truck is only fully protected if both legs are covered under the same policy or coordinated endorsements.

The speed of claims settlement is a concrete financial benefit that often goes unquantified. Bespoke cargo policies enable reimbursement within 30 days compared to 180 days for standard carrier claims. For a business with $500,000 in freight moving monthly, that difference in settlement speed directly affects your ability to pay suppliers, fund the next shipment, and maintain operations without emergency credit.

How to choose the right cargo coverage for your business

Choosing the right coverage starts with knowing the actual commercial value of your typical and highest-value loads. Many operators set coverage limits based on average shipments and then find themselves underinsured when a high-value load is damaged. Your policy limit should reflect your maximum single-shipment exposure, not your average.

Commodity type and route risk both shape your coverage needs significantly. Refrigerated freight requires a reefer breakdown endorsement, since standard MTC policies exclude temperature-related losses caused by mechanical failure. Electronics, pharmaceuticals, and luxury goods attract higher theft rates and may require specialized cargo protection with lower deductibles and broader theft definitions. Routes through high-crime corridors or regions with limited emergency response increase your exposure and should be reflected in your policy terms.

Broker and shipper contracts set hard minimums you cannot ignore. Most freight brokers require carriers to carry MTC coverage of at least $100,000, and many large shippers require $250,000 to $500,000 before awarding lanes. Inadequate coverage risks breach of contract and immediate disqualification from loads. Reviewing your broker agreements annually and matching your coverage limits to contract requirements protects both your revenue and your legal standing.

Policy sub-limits and deductibles deserve as much attention as the headline coverage amount. A policy with a $250,000 limit but a $50,000 sub-limit on electronics leaves you exposed on the loads that matter most. Review every sub-limit, check deductible levels against your cash reserves, and confirm that your policy covers the specific commodities you haul. If you are unsure how much coverage your operation actually needs, the Diamondbackins guide on evaluating coverage limits provides a practical framework for freight operators.

Pro Tip: Request a certificate of insurance from every carrier you hire and verify their MTC coverage limits match your shipment value before releasing the load. A carrier with a $100,000 policy hauling a $300,000 shipment leaves a $200,000 gap that falls on you.

Best practices to reduce cargo loss beyond your policy

Insurance pays for losses. Good operational practice prevents them. The two work together, and neither is sufficient alone.

Documentation is your first line of defense when a claim occurs. Photograph every load at pickup, confirm the condition of goods against the bill of lading, and note any pre-existing damage before signing. Missing or late documentation is one of the most common reasons insurers deny claims, even when the loss itself is clearly covered. Timely notification to your insurer after a loss is equally critical. Most policies require notice within 24 to 72 hours of discovering damage or theft.

GPS tracking on trailers and high-security locks on cargo doors reduce theft exposure on high-value loads. Cargo theft is a growing problem across major transit corridors, and carriers who can demonstrate active security measures often qualify for lower premiums. Avoiding known high-theft areas, particularly overnight stops near major distribution hubs, reduces your risk profile without adding cost.

Selecting carriers with strong safety records and verified cargo insurance limits is a risk management decision, not just a procurement one. Reviewing carrier safety scores through the FMCSA’s Safety Measurement System before awarding loads gives you data to make informed decisions. Guidance on managing logistics risk across different freight types reinforces that specialized handling and proper insurance work as a system, not in isolation.

For businesses shipping internationally, preparing for General Average exposure before a voyage begins is practical risk management. Confirm your policy covers General Average contributions and that your insurer can post bonds quickly. A vessel incident that holds your goods for weeks while you arrange a cash bond is a disruption your policy should prevent entirely.

Key takeaways

Adequate cargo coverage protects the full commercial value of your freight where carrier liability ends, paying regardless of fault and settling claims in weeks rather than months.

| Point | Details |

|---|---|

| Carrier liability is insufficient | Weight-based caps and fault requirements leave most shippers with significant unrecovered losses. |

| MTC and All-Risk policies fill the gap | These policies cover theft, fire, collision, and General Average at declared commercial value. |

| Coverage limits must match load values | Set limits based on your highest-value shipment, not your average, and review broker contract minimums. |

| Documentation prevents claim denial | Photos at pickup and timely insurer notification are required for successful claims. |

| Multi-modal gaps need explicit coverage | Marine policies do not automatically cover inland transit; request extensions for every leg of the journey. |

What I’ve learned about cargo coverage after years in freight insurance

I have reviewed hundreds of cargo claims over the years, and the pattern is consistent. The businesses that suffer the most are not the ones hit by catastrophic events. They are the ones that assumed their carrier’s insurance was enough and never verified the actual limits until a loss occurred.

The most common mistake I see is treating cargo insurance as a compliance checkbox rather than a financial tool. Operators secure the minimum MTC coverage to satisfy a broker contract and then move on. When a $200,000 load of electronics is stolen from a truck stop in Atlanta, they discover their $100,000 policy covers half the loss and their carrier’s liability covers almost nothing. That gap does not come from bad luck. It comes from not reviewing coverage against actual exposure.

Current logistics conditions make this more urgent, not less. Supply chain volatility, rising cargo theft rates, and tighter freight margins mean that a single uninsured loss can erase months of profit. I have seen well-run operations absorb a major cargo loss and recover because they had the right policy in place. I have also seen operators with years of clean records face serious financial strain from a single underinsured incident. The difference between those two outcomes is almost always a policy review that took less than an hour.

My recommendation is direct: review your cargo coverage limits against your actual shipment values every six months. Check your broker contracts for minimum requirements. Confirm your policy covers every transit mode you use. And treat the common trucking insurance pitfalls as a checklist, not a cautionary tale for someone else.

— Vladimir

Get the right cargo coverage through Diamondbackins

Diamondbackins specializes in commercial trucking and cargo insurance, giving freight operators and fleet managers instant access to quotes from multiple top-rated insurers in one place. You can compare coverage options, review policy limits, and purchase a policy that matches your actual freight values and broker contract requirements, all without the back-and-forth of a traditional broker. Whether you need Motor Truck Cargo coverage, All-Risk protection, or multi-modal endorsements, Diamondbackins makes it straightforward to find and secure the right policy. Review your cargo coverage options today and get an instant quote tailored to your fleet and the loads you haul.

FAQ

What is adequate cargo coverage?

Adequate cargo coverage is insurance that protects the full declared commercial value of your freight during transit, covering losses from theft, damage, and accidents beyond what carrier liability provides. It pays regardless of fault, unlike carrier liability which requires proving carrier negligence.

Why is carrier liability not enough to protect my shipment?

Carrier liability is calculated by weight under international conventions like the Hague-Visby Rules, not by cargo value, meaning payouts can be as low as a few dollars per kilogram on high-value goods. Settlement can also take up to 180 days, creating serious cash flow problems for freight operators.

What does Motor Truck Cargo insurance cover?

Motor Truck Cargo insurance covers the value of freight in a carrier’s custody from pickup to delivery, including losses from theft, fire, collision, and loading accidents. Most freight brokers require MTC limits between $100,000 and $500,000 before assigning loads to a carrier.

How do I know if my cargo coverage limits are high enough?

Your coverage limit should match the maximum commercial value of any single shipment you move, not your average load value. Review your broker contracts for minimum requirements and check policy sub-limits for specific commodity types like electronics or refrigerated goods.

What happens if I have no cargo insurance during a General Average event?

Without cargo insurance, you are required to post a cash bond to release your goods from the carrier’s custody after a General Average declaration, which can run into tens of thousands of dollars. A policy with General Average coverage pays the bond and covers your share of salvage costs automatically.