Buying commercial truck insurance through a traditional broker can feel like navigating a maze with no map. You make calls, wait days for callbacks, shuffle through stacks of paperwork, and still end up uncertain about whether you got the best rate. Fleet managers and small business owners in the trucking industry deserve a better process, and today, a modern online approach delivers exactly that. This guide walks you through every stage of purchasing commercial truck insurance online, from preparation through compliance verification, so you can protect your fleet faster, smarter, and at a lower cost.

Table of Contents

- What you need before you start: Requirements and prep checklist

- A step-by-step process to buying commercial truck insurance online

- Understanding costs and how to save on premiums

- Common mistakes in online insurance buying (and how to avoid them)

- A smarter path to fleet insurance: Lessons from the trenches

- Protect your fleet with streamlined online coverage

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Preparation is critical | Having all required documents before you begin speeds up the insurance buying process. |

| Follow step-by-step | A structured seven-step process ensures you get accurate quotes and maintain compliance. |

| Compare for savings | Obtaining multiple quotes helps lower costs and find the coverage best suited to your fleet. |

| Know your costs | Understanding pricing factors enables you to leverage discounts and avoid overpaying. |

| Avoid common errors | Double-check information to prevent delays, compliance issues, and missed savings. |

What you need before you start: Requirements and prep checklist

To get started, let’s cover what you need at your fingertips for a seamless insurance application.

Preparation is the single biggest factor in how smoothly your online insurance purchase goes. Walking into a quote platform without the right documents is like trying to register a vehicle without a title. You can waste hours going back and forth, and in some cases, gaps in your submission can actually delay FMCSA compliance filings, which means your trucks could be sidelined while you scramble to fix the paperwork.

What specific documents do you need?

The commercial auto application process requires you to gather your business information, vehicle VINs, driver’s licenses and motor vehicle records (MVRs), DOT and MC numbers, and recent loss runs before you begin. Loss runs are your claims history reports, and insurers use them to assess your risk profile. If you have not requested loss runs from your previous carrier recently, do it now. Most carriers can provide them within 24 to 48 hours, and having them on hand prevents the most common application delay.

Beyond those essentials, you should also prepare your business structure documentation, such as your LLC operating agreement or articles of incorporation, along with a complete list of driver information including years of experience, endorsements held, and any violations on record. Each driver’s CSA (Compliance, Safety, Accountability) score can significantly affect your premium, so knowing your drivers’ records before the insurer does helps you anticipate the pricing you will receive.

| Document type | What to include | Why it matters |

|---|---|---|

| Vehicle information | VIN, make, model, year, GVWR | Determines coverage category and rates |

| Driver records | License, MVR, endorsements | Key pricing and risk factor |

| Business details | DOT/MC numbers, entity type | Required for FMCSA compliance filings |

| Loss runs | 3 to 5 years of claims history | Establishes your insurability and premiums |

| Cargo description | Type, weight, hazmat designation | Affects liability limits and cargo coverage |

You can also review trucking business insurance basics to make sure you understand how coverage types relate to your specific operation before you submit a single quote request.

Pro Tip: Request your loss runs from your current or previous insurer at least one week before you plan to apply. Some carriers require a written request and may take a few business days. Starting early keeps you in control of the timeline.

The goal of this preparation stage is accuracy. Inaccurate or incomplete information does not just slow things down; it can result in a policy that does not match your actual risk exposure, which creates serious problems at claim time.

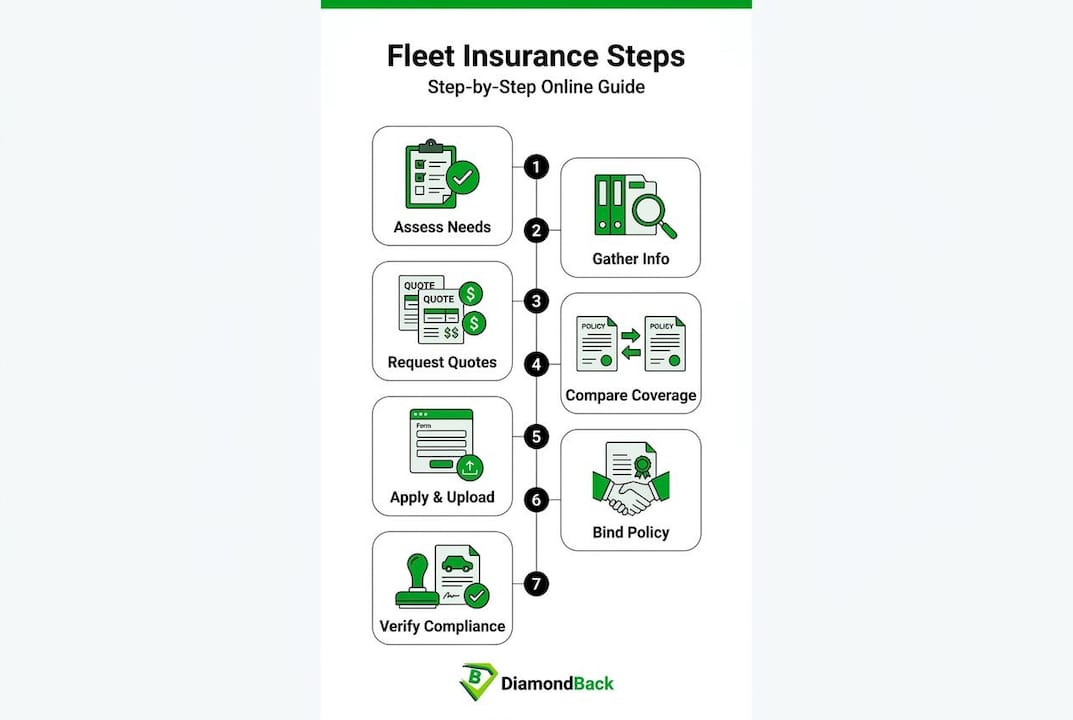

A step-by-step process to buying commercial truck insurance online

Once everything’s gathered, follow this sequence to secure your fleet’s protection efficiently.

The online process for purchasing commercial truck insurance is straightforward when you break it into distinct, manageable steps. Each stage builds on the previous one, and skipping steps is where most fleet managers run into trouble.

Step 1: Assess your coverage needs. Before you request a single quote, you need to clearly define what you are insuring and what level of coverage your operation requires. This means identifying the number and type of vehicles, the types of cargo you haul, the states you operate in, and the minimum liability limits required by the FMCSA. For most for-hire trucking operations, FMCSA minimum coverage requirements start at $750,000 in liability for general freight, rising to $5,000,000 for hazardous materials. Knowing your threshold before you shop ensures you do not accidentally purchase a policy that falls short.

Step 2: Gather your documents. As outlined above, this is the prep stage. Do not skip it or rush through it.

Step 3: Request quotes online. Using a platform that aggregates quotes from multiple carriers saves you significant time and gives you a realistic view of what the market offers. When you compare trucking fleet quotes from several providers simultaneously, you gain immediate leverage on pricing without spending days on the phone.

Step 4: Compare your quotes carefully. Price is not the only factor. Review the coverage limits, deductibles, exclusions, and the financial stability rating of each carrier. A lower premium with a high deductible or poor claims service can cost you far more in the long run. Look closely at what each policy covers for physical damage, bobtail liability, cargo loss, and general liability.

Step 5: Apply online and submit your documents. Most modern platforms allow you to upload all required documents directly through the portal. Fill in each field accurately and double-check every entry before submission. Errors at this stage can lead to delays or incorrect coverage.

Step 6: Purchase, bind your policy, and confirm FMCSA filings. Once you accept a quote, you will be asked to bind the policy, which means making it active. Critically, your insurer must file a BMC-91 form with the FMCSA to prove financial responsibility. Confirm this filing is submitted and accepted before your trucks operate under the new policy. Operating without that filing in place is a compliance violation, regardless of whether you have paid your premium.

Step 7: Verify and document your compliance. Store your policy documents, proof of filing, and certificates of insurance in an accessible location. Many fleet managers keep digital copies in a shared drive accessible to dispatchers and drivers.

For a detailed look at what affects your pricing at each stage, review the truck insurance cost breakdown to understand exactly what you are paying for.

Pro Tip: When comparing quotes, ask each carrier or platform whether their system automatically submits the BMC-91 filing on your behalf. Some platforms handle this for you as part of the purchase process, which eliminates one of the most commonly missed compliance steps.

Understanding costs and how to save on premiums

After understanding the process, it’s crucial to anticipate costs and know how to cut expenses.

Insurance costs in the trucking industry can feel unpredictable, but they follow a clear logic once you understand the pricing drivers. Knowing what factors move your premium up or down puts you in a much stronger negotiating position.

According to industry cost benchmarks, owner-operators running a single truck typically pay between $8,000 and $15,000 per year for commercial truck insurance. Small fleets with two to five trucks generally see annual premiums in the $15,000 to $40,000 range, with discounts available through safety programs, telematics devices, policy bundling, and fleet size. These figures vary widely based on your specific risk profile, cargo type, and operating territory.

| Fleet size | Typical annual premium range | Primary pricing drivers |

|---|---|---|

| 1 truck (owner-operator) | $8,000 to $15,000 | Driver record, cargo type, radius |

| 2 to 5 trucks | $15,000 to $40,000 | Fleet safety record, CSA scores |

| 6 to 10 trucks | $35,000 to $90,000+ | Claims history, driver pool quality |

What drives your rate up or down?

Your CSA score is one of the most influential factors. Carriers use it to evaluate how your operation manages safety, and a poor score translates directly into higher premiums or difficulty finding coverage at all. The type of cargo you haul is another major variable. Hauling refrigerated food carries different risk than hauling building materials or chemicals, and your premium reflects that difference. Driver experience matters significantly. A fleet with drivers averaging ten or more years on the road will consistently outperform a newer fleet in pricing.

Telematics technology has become one of the most effective tools for reducing premiums. Insurers reward fleets that use GPS tracking and driver behavior monitoring because it demonstrates accountability and reduces accident frequency. Bundling your commercial auto, general liability, and cargo insurance with a single carrier often unlocks meaningful multi-policy discounts as well.

You can explore how truck insurance rate factors interact with your specific operation to identify where you have the most room to reduce costs. Understanding which premium impact factors apply to your fleet helps you prioritize the improvements that will have the greatest financial return.

The fleets that consistently pay the lowest premiums are not just the safest operators. They are the ones who actively manage their insurance relationship, review coverage annually, and leverage every available discount.

Pro Tip: Install telematics before your next renewal and request a re-quote. Many carriers will apply a discount retroactively or at the next policy period if you can demonstrate monitored safe driving over 60 to 90 days.

Common mistakes in online insurance buying (and how to avoid them)

Even with a clear process, certain mistakes can set you back, and here is how to avoid them.

The online process is faster than traditional methods, but speed can lead to careless errors. The most expensive mistakes in commercial truck insurance purchases are almost always preventable with a simple review step before submission.

What is the most common error fleet managers make?

Submitting incomplete or inaccurate information is the leading cause of application delays and compliance problems. As the 2026 commercial auto process guidelines confirm, incomplete or inaccurate information can slow down application approval and delay FMCSA compliance. This includes errors as straightforward as a mistyped VIN, a missing driver record, or an outdated loss run. Each one creates a follow-up request from the underwriter, and follow-up requests add days to your timeline.

Underestimating your coverage needs is another serious and costly mistake. Some fleet owners try to minimize their premiums by selecting the bare minimum liability limits. If a major accident occurs and your limits fall short of the damages, you are personally exposed to the difference. Always purchase at least the FMCSA minimums, and evaluate whether your cargo value or operating risk warrants higher limits.

Skipping the comparison stage is surprisingly common. Some fleet managers accept the first quote they receive because the process feels overwhelming. Online platforms make comparison straightforward, and the price difference between the lowest and highest quote for the same coverage can easily reach $2,000 to $5,000 annually for a small fleet.

Forgetting to confirm FMCSA compliance filings is perhaps the most operationally dangerous mistake. You can have a valid policy and still face fines or shutdowns if the BMC-91 has not been filed with the FMCSA. Always verify that your carrier or platform has completed this step before dispatch.

State-specific requirements add another layer of complexity. Operating across state lines means you may have varying minimum coverage requirements depending on where your trucks travel. Reviewing state-specific insurance rates and requirements helps ensure your policy is valid everywhere you operate.

Pro Tip: Before you hit submit on any application, run through a three-point check: verify every VIN matches your vehicle list, confirm every driver’s MVR is included, and make sure your loss runs cover at least three full policy years.

A smarter path to fleet insurance: Lessons from the trenches

Here is an uncomfortable truth about traditional insurance buying that most people in this industry will not say out loud: the old way was never designed for efficiency. It was designed for intermediaries. Brokers calling brokers, manual forms routed through multiple desks, coverage comparisons that happened over the phone with no written record. That process benefited everyone except the fleet manager sitting at the end of it.

The online-first approach changes the dynamic fundamentally. When you streamline your insurance buying process through a digital platform, you gain something brokers rarely offer: transparency. You see every quote side by side, every coverage limit spelled out, every exclusion visible before you commit. There is no ambiguity, no waiting for someone to get back to you on Monday.

What we have consistently observed among fleet managers who adopt an online-first approach is that they stop treating insurance as an annual chore and start treating it as an operational decision. That shift in mindset matters more than any single discount. When you approach your fleet’s insurance with the same structured thinking you apply to route planning or vehicle maintenance, you make better decisions, catch compliance gaps early, and reduce your total cost of risk over time. The fleet managers who struggle are the ones who rush the process at renewal time, skip the comparison step, and assume last year’s policy still fits this year’s operation. It rarely does.

Protect your fleet with streamlined online coverage

You have the process, the checklist, the cost knowledge, and the pitfalls clearly mapped out. The next step is turning that knowledge into actual protection for your trucks and your business.

Diamondback Insurance makes that step fast, transparent, and cost-effective. Our platform lets you get instant fleet insurance quotes from multiple top-rated carriers in minutes, compare options side by side, and bind your policy without ever picking up a phone. Whether you are covering a single owner-operator rig or a growing regional fleet, we have options built for your operation. If you are based in the Southeast, explore Georgia commercial trucking coverage designed specifically for your state’s requirements. Start with online instant quotes today and see how much your fleet can save.

Frequently asked questions

What documents are required to purchase commercial truck insurance online?

You need your business information, vehicle VINs, driver’s licenses and MVRs, DOT and MC numbers, and recent loss runs covering at least three years of claims history. Having these ready before you start the application prevents delays and accelerates compliance processing.

How much does commercial truck insurance cost for one truck or a small fleet?

Owner-operators typically pay between $8,000 and $15,000 per year, while small fleets of two to five trucks generally fall in the $15,000 to $40,000 range annually, depending on cargo type, driver records, and operating territory.

How do I speed up the insurance buying process?

Prepare all required documents before you log into any quote platform, and compare quotes from multiple providers simultaneously using an aggregator. This single habit cuts most application timelines from days down to hours.

How do I ensure my coverage meets FMCSA requirements?

Confirm that your policy includes the required minimum liability limits for your cargo type and that your insurer files the BMC-91 proof of financial responsibility with the FMCSA as part of the binding process. Always verify that filing before your trucks go back on the road.

What discounts are available for truck insurance?

Most carriers offer premium reductions for safety programs, telematics usage, policy bundling, and larger fleet size. Installing telematics and maintaining a strong safety record are the two most consistent and significant ways to reduce what you pay year over year.