Letting your trucking insurance lapse—even for a single day—can bring your entire operation to a standstill. Coverage lapses trigger FMCSA suspension of your operating authority (your MC number), which means no interstate hauls, no revenue, and no business until coverage is fully reinstated. Most fleet managers think of renewal as routine paperwork, but the reality is that it touches every corner of your operation: regulatory standing, financial health, driver safety programs, and your ability to compete. This article walks you through why timely renewal matters, what it costs you to delay, and how to approach it strategically.

Table of Contents

- Compliance and operational risks of letting insurance lapse

- Financial costs and savings: What renewal means for your bottom line

- Fleet insurance renewals vs. individual policies: Administrative and cash flow strategies

- Expert tips to get ahead on renewals and keep your rates low

- Renewal isn’t just compliance—It’s your hidden profit lever

- Get support for your next insurance renewal

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Avoid costly lapses | Letting trucking insurance expire can halt your operations and raise future premiums. |

| Renewal saves money | Staying continuously insured preserves discounts and reduces long-term costs. |

| Fleet policies simplify renewal | Renewing one fleet policy is more efficient and can save money versus managing multiple individual plans. |

| Prepare for rising rates | Market trends and nuclear verdicts may drive premium hikes, so proactive renewal preparation is crucial. |

Compliance and operational risks of letting insurance lapse

With the importance established, let’s look closer at the real-world compliance hurdles and what happens when insurance renewal is skipped.

What does the FMCSA actually require?

The Federal Motor Carrier Safety Administration (FMCSA) mandates that all carriers operating in interstate commerce maintain continuous, uninterrupted insurance coverage. This is not a grace period situation. The moment your insurer files a cancellation notice with the FMCSA, the agency begins the process of revoking your operating authority. A coverage lapse triggers FMCSA suspension of your MC number, and that suspension is immediate and public. Brokers, shippers, and freight platforms can see it. That visibility alone can cost you contracts before you even realize what happened.

State requirements add another layer. Many states require proof of continuous coverage for state operating licenses, intrastate authority, and vehicle registration. A lapse at the federal level often creates a cascade of state-level compliance problems that take weeks to untangle.

What happens the moment your policy lapses?

The business impact is swift. Authority revocation takes weeks or months to reinstate, and during that window you cannot legally haul freight. Every day off the road is lost revenue. For a small fleet running five trucks, even a week of downtime can mean tens of thousands of dollars in missed loads. For larger operations, the damage compounds quickly.

Reinstatement is not simply a matter of paying a late fee and moving on. You must secure new coverage, file the appropriate forms (typically a Form BMC-91 or BMC-91X for liability), wait for FMCSA processing, and then verify that your authority has been restored. That process is rarely fast. Meanwhile, drivers sit idle, fixed costs keep running, and customers look elsewhere.

There is also a longer-term reputational cost. Shippers and brokers track carrier safety scores and compliance records. A suspension on your record signals instability, and rebuilding that trust takes far longer than reinstating a policy. Understanding insurance rate increases after a lapse is equally important, because the financial pain does not stop when coverage resumes.

| Consequence | Timeline | Business Impact |

|---|---|---|

| FMCSA authority suspended | Immediate upon lapse | No interstate operations |

| State authority issues | Days to weeks | Intrastate operations at risk |

| Reinstatement of authority | Weeks to months | Lost revenue, idle drivers |

| Shipper/broker trust damage | Long-term | Reduced freight opportunities |

| Premium increases at renewal | Next policy term | Higher ongoing operating costs |

The bottom line is clear: the perceived short-term savings of skipping or delaying renewal are dwarfed by the operational and financial consequences that follow.

Financial costs and savings: What renewal means for your bottom line

Beyond compliance, financial motivations drive why insurance renewal is a must for every fleet. Here’s how the numbers break down.

How much is insurance actually costing your fleet?

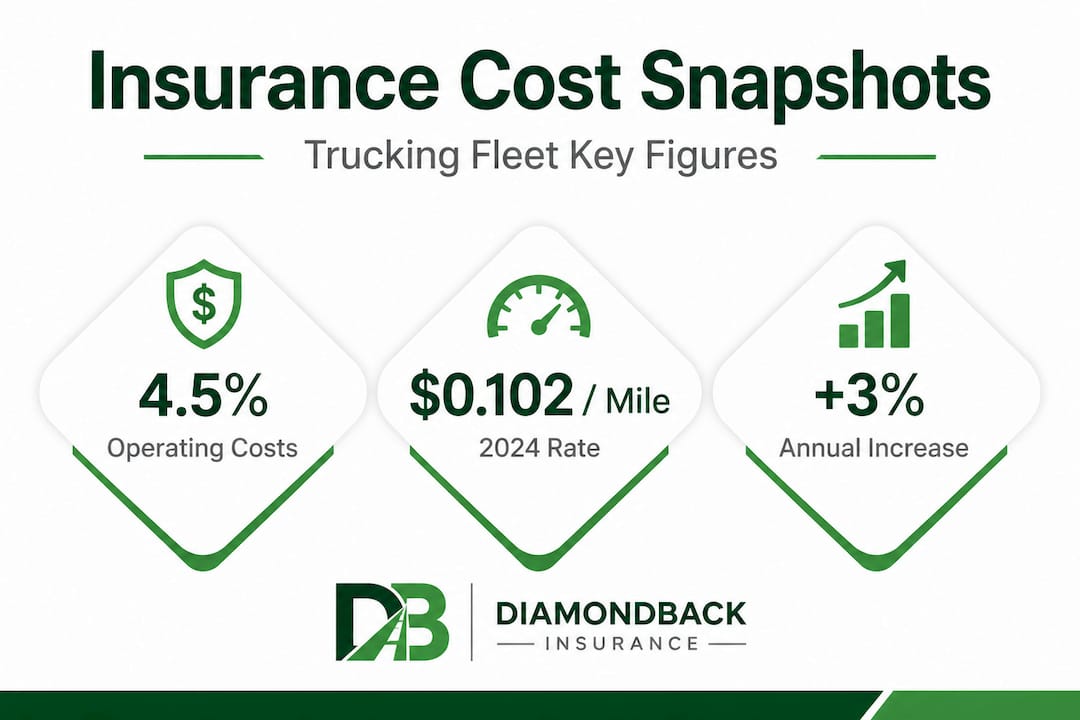

Trucking insurance reached $0.102 per mile in 2024, according to ATRI data, up 3% from 2023 and representing roughly 4.5% to 10% of total operating costs depending on fleet size and haul type. That figure is expected to climb further through 2025 and 2026, driven by claims inflation and what the industry calls “nuclear verdicts,” which are jury awards with a median value of $51 million in trucking-related cases. These verdicts push insurers to price risk higher across the board, even for carriers with clean records.

That means your renewal is not happening in a vacuum. Market forces are working against you, and the only real leverage you have is the quality of your own risk profile.

How lapses and poor records raise your rates for years

A coverage lapse immediately marks your company as a higher risk in the eyes of underwriters. Lapses increase future premiums and can keep your rates elevated for several policy cycles. New carriers already pay 40% to 100% more than established ones with clean records. A lapse essentially resets some of that hard-earned credibility.

On the flip side, carriers who invest in safety technology and maintain strong records can earn meaningful discounts. Telematics systems and forward-facing cameras yield 5% to 15% premium discounts with many insurers. Those savings compound over time and directly offset the rising per-mile cost of coverage.

Understanding what affects insurance premiums gives you a clearer picture of where to focus your energy before renewal season. Reviewing factors affecting rates specific to your fleet type helps you enter negotiations with real data rather than guesswork.

Smart steps to reduce your renewal costs

First, review your loss run reports, which are detailed records of your claims history, at least 90 days before renewal. Insurers scrutinize these closely, and knowing what they will see gives you time to prepare explanations or demonstrate corrective actions.

Second, document all safety investments. If you have installed dashcams, added electronic logging devices (ELDs), or enrolled drivers in ongoing training programs, make sure your insurer knows. These are tangible risk-reduction measures that underwriters reward.

Third, review driver motor vehicle records (MVRs) proactively. A driver with recent violations can spike your renewal quote significantly. Addressing those issues before submission puts you in a stronger position.

Pro Tip: Request quotes from multiple insurers at least 60 days before your renewal date. The market can shift quickly, and comparing options gives you negotiating power even if you ultimately stay with your current carrier.

| Action | Potential Premium Impact |

|---|---|

| Installing telematics/dashcams | 5-15% discount |

| Clean CSA score (no violations) | Lower base rate |

| Coverage lapse on record | 20-40% rate increase |

| New carrier (under 2 years) | 40-100% higher than established rate |

| Loss ratio under 60% | Stronger negotiating position |

Fleet insurance renewals vs. individual policies: Administrative and cash flow strategies

With the costs and risks in mind, fleet managers should also consider how the structure and timing of policy renewal impacts day-to-day operations.

Why fleet policies simplify your life

Managing individual policies for each truck in your fleet creates a documentation nightmare. Different renewal dates, separate premium payments, and varying coverage terms make it easy for gaps to appear. Fleet insurance simplifies admin and renewals compared to individual policies, and it typically comes with bulk discounts that reduce your per-unit cost. One renewal date, one set of documents, one relationship with your insurer. That simplicity has real operational value.

Fleet policies also make it easier to add or remove vehicles as your operation changes. If you acquire a new truck mid-term, adding it to an existing fleet policy is straightforward. Managing that same change across multiple individual policies is far more complicated and creates more opportunities for error.

Reviewing fleet insurance coverages before your renewal helps you identify whether your current structure still fits your operation or whether consolidating to a fleet policy would serve you better.

Managing cash flow around renewal season

One of the most overlooked challenges in trucking insurance renewal is the cash flow impact. Annual or semi-annual premiums represent a significant outlay, and if your working capital is stretched, that payment can create real strain. Cash flow gaps during renewal are a genuine risk for smaller fleets, and they sometimes push operators to delay renewal or seek lower coverage limits just to manage the immediate cost.

The better approach is to plan for renewal payments the same way you plan for major maintenance or equipment purchases. Set aside a portion of monthly revenue specifically for the upcoming premium. If your insurer offers monthly payment plans, evaluate whether the added cost of installment fees is worth the cash flow relief. For many smaller operators, it is.

Pro Tip: If cash flow is consistently tight around renewal, consider shifting your policy start date to align with your strongest revenue months. Many insurers will accommodate a mid-term date change with advance notice.

What fleet managers often overlook at renewal time

Coverage limits are frequently set and then forgotten. Your liability limits, cargo coverage amounts, and physical damage deductibles should be reviewed every renewal cycle. Your operation may have grown, your cargo values may have changed, or your risk exposure may have shifted. Renewing with the same limits year after year without review can leave you dangerously underinsured.

Also review any endorsements or riders attached to your policy. Specialized coverage for refrigerated cargo, hazardous materials, or owner-operators under your authority needs to be confirmed and updated at each renewal.

Expert tips to get ahead on renewals and keep your rates low

Now that the core reasons and financial tactics are clear, let’s close out with the top strategies to make insurance renewal work for your business.

Start the process earlier than you think necessary

Most carriers wait until 30 days before renewal to start gathering documents. The carriers who consistently secure the best rates start 90 days out. That extra time allows you to compile loss runs, address any open claims, and have meaningful conversations with multiple insurers rather than scrambling to accept whatever quote arrives first.

Poor CSA scores directly raise premiums on a rolling 24-month basis, which means violations from nearly two years ago are still affecting your rate today. Knowing your score well before renewal gives you time to contest inaccurate data or demonstrate improvement trends to underwriters.

Understand the nuclear verdict effect on your renewal

Even if your fleet has had zero claims in the past three years, your renewal rate may still increase. Nuclear verdicts drive market-wide rate hikes regardless of individual carrier performance. Insurers price the risk of what could happen based on industry-wide loss data, not just your own. Understanding this dynamic helps you set realistic expectations and avoid frustration when rates rise despite a clean record.

The best counter to this market pressure is a loss ratio below 60%, meaning your claims paid out represent less than 60% of the premiums you have paid. Carriers who can demonstrate this ratio consistently have real leverage in renewal negotiations.

Avoid the most common renewal mistakes

Rushing the process, failing to update driver lists, and neglecting to report new equipment are among the most common renewal mistakes that create coverage gaps or premium surprises. Each of these issues is preventable with a structured renewal checklist and a clear internal timeline.

Document every safety improvement your fleet has made during the policy year. New training programs, upgraded equipment, improved hiring standards—these all tell a story of a well-managed operation. Underwriters respond to that story when it is presented clearly and with supporting data.

“The carriers who treat renewal as a strategic event rather than an administrative task consistently come out ahead, both in rate and in coverage quality.”

Renewal isn’t just compliance—It’s your hidden profit lever

Most fleets approach renewal with one goal: get it done without the rate going up too much. That mindset leaves money on the table. The carriers who consistently outperform their peers on insurance costs treat renewal as an active business strategy, not a reactive compliance task.

Think about what renewal season actually gives you. It is a scheduled, structured moment when you have your insurer’s full attention. You have documentation of your safety performance, your claims history, and your operational investments in front of you. That is a negotiating position, not just a paperwork exercise. Trucking insurance experts who work with top-performing carriers consistently note that the operators who come to renewal prepared, with clean data and a clear narrative about their risk management practices, secure meaningfully better terms than those who simply respond to whatever quote arrives.

There is also a competitive angle that most fleet managers miss entirely. When a competitor lets their coverage lapse, loses authority, or gets hit with a rate spike that squeezes their margins, that is an opportunity for you. Freight brokers and shippers notice which carriers are consistently reliable and financially stable. Your clean renewal record is part of that signal. It is not just about avoiding problems. It is about building a reputation that attracts better freight at better rates.

Forward-thinking operators also use renewal season to reassess their entire coverage structure. Are your liability limits still appropriate given how nuclear verdicts have shifted the risk landscape? Is your cargo coverage keeping pace with the value of what you haul? These are questions that generate real financial protection when answered proactively, and they are questions that only get asked when you treat renewal as a strategic event.

Get support for your next insurance renewal

If you’re ready to make renewal a competitive advantage, here’s how DiamondBack can help.

Renewal season does not have to be stressful or uncertain. DiamondBack Insurance gives you instant access to tailored quotes from multiple top-rated insurers, so you can compare options and secure the right coverage without the back-and-forth of traditional brokers. Whether you need trucking insurance explained from the ground up or you are a seasoned fleet manager looking to optimize your renewal terms, the platform is built to move at your pace.

From single-unit operators to regional fleets, DiamondBack covers a wide range of operations across the country, including commercial trucking insurance in Georgia and beyond. The process is fully online, transparent, and designed to put you in control of your coverage decisions. Get your fleet insurance quotes today and enter your next renewal season with confidence.

Frequently asked questions

What happens if trucking insurance lapses for even a day?

A lapse, even for one day, triggers FMCSA suspension of your operating authority, halting all interstate operations until coverage is fully restored and documented with the agency.

Does missing a renewal impact future insurance premiums?

Yes, a lapse marks your company as higher risk, and future premiums increase for several years as insurers price in the added uncertainty around your coverage continuity.

How can I prepare for my trucking insurance renewal to avoid problems?

Keep safety records strong, gather all claims and loss data at least 90 days in advance, and prepare a loss ratio below 60% to give yourself real negotiating leverage with underwriters.

Is fleet insurance renewal better than separate policies for each truck?

Fleet renewals simplify admin and often deliver bulk discounts, reducing the risk of coverage gaps that come with managing multiple individual policy timelines.

Will industry-wide claim trends impact my renewal rate?

Yes, nuclear verdicts raise rates across the market, meaning even fleets with zero claims can see premium increases driven entirely by industry-wide loss trends.