A single missed premium payment. A renewal notice that slipped through the cracks. A job change that left your health coverage in limbo for three weeks. These are the moments that create insurance coverage gaps, and the financial consequences can be severe before you even realize what happened. Understanding why avoid insurance gaps matters is the first step toward protecting everything you’ve worked to build. Whether you own a home, run a small business, or manage a fleet of trucks, a lapse in coverage can expose you to costs that dwarf what you would have paid in premiums.

Table of Contents

- Key takeaways

- Why avoid insurance gaps: understanding what they are

- Financial risks of coverage lapses

- How federal flood insurance lapses create broader problems

- How to avoid insurance gaps before they happen

- My perspective on coverage continuity

- Protect your coverage with Diamondbackins

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Coverage stops instantly | A lapse removes all financial protection the moment it occurs, with no retroactive coverage for claims. |

| Lenders act fast | Mortgage lenders impose costly force-placed insurance within 30 to 45 days of a lapse, covering only their interest. |

| Flood program lapses are systemic | NFIP reauthorization gaps can stall thousands of home sales daily when new and renewal policies cannot be issued. |

| Higher premiums follow gaps | Even short lapses lead to stricter underwriting and elevated premiums when you try to reinstate or replace coverage. |

| Prevention is straightforward | Automatic payments, proactive renewal reviews, and knowing your enrollment windows can eliminate most gaps entirely. |

Why avoid insurance gaps: understanding what they are

An insurance gap, or what the industry formally calls a coverage lapse, is any period of time during which your policy is not in force. The effect is immediate and absolute. Coverage stops instantly with no grace period for claims that occur during the gap, no matter how brief that window is.

Gaps happen for many reasons, and most of them are not dramatic. Missed premium payments are the most common cause. Renewal delays occur when you switch providers but the new policy start date does not perfectly align with the old policy’s end date. Life transitions like changing jobs, relocating to a new state, or aging out of a parent’s plan frequently create coverage disconnects. Administrative errors, such as an insurer using an outdated bank account or an incorrect mailing address, can quietly cancel a policy without your knowledge.

The types of coverage affected vary widely. A homeowners insurance lapse leaves your property exposed to fire, theft, and storm damage with zero protection. A flood insurance gap means a single weather event could cost you hundreds of thousands of dollars with no recourse. A business liability gap exposes your small business to lawsuits without any financial backstop. Health insurance gaps leave you paying full price for medical care that could otherwise be covered.

What makes coverage lapses particularly dangerous is that they often start as minor oversights. You assume the autopay is running. You think the renewal was automatic. You expect your new employer’s health plan to start on day one. That assumption is where the financial risk begins.

Financial risks of coverage lapses

The consequences of insurance coverage gaps are not theoretical. They show up in your bank account, your mortgage statement, and your business cash flow.

For homeowners with a mortgage, the impact arrives quickly. Lenders impose force-placed insurance within 30 to 45 days after detecting a lapse. This force-placed policy typically costs two to three times more than standard homeowners insurance. More importantly, it protects only the lender’s financial interest in the property. Your personal belongings, your liability exposure, and any improvements you’ve made to the home are completely unprotected.

The cost of that force-placed policy does not disappear. Escrow shortfalls from lapses cause lenders to raise your monthly mortgage payment by $100 to $300 or more until the shortfall is resolved. That can last months, putting real pressure on your monthly budget at exactly the wrong time.

A coverage lapse does not just mean you lose protection. It means you pay more for less coverage, and the financial strain compounds the longer the gap continues.

For small business owners, the risks of insurance gaps extend to operational continuity. A liability claim that occurs during a gap, even a slip-and-fall on your property, becomes your personal financial responsibility. If you operate commercial vehicles or a trucking fleet, any accident during a lapse period can expose you to costs that threaten the business entirely. Reviewing common trucking insurance mistakes is a practical way to see how quickly these situations escalate.

Pro Tip: Reinstating a lapsed homeowners policy within 30 days is significantly cheaper than waiting. The longer the gap, the more likely you’ll face stricter underwriting requirements and higher premiums on any new policy you try to secure.

The long-term effects matter too. Insurers view a coverage history with gaps as a sign of higher risk. When you apply for a new policy or attempt reinstatement, gaps lead to higher premiums and stricter qualification standards. The financial hit from a single lapse can follow you for years.

How federal flood insurance lapses create broader problems

Flood insurance operates differently from most other coverage types, and the systemic risks it creates deserve special attention. The National Flood Insurance Program, known as the NFIP, is the primary source of flood coverage for most American homeowners in designated flood zones. It operates under periodic congressional reauthorizations, and those reauthorizations do not always happen on time.

| NFIP lapse impact | What it means for you |

|---|---|

| New policies cannot be issued | Homebuyers in flood zones cannot obtain required flood insurance to close a purchase. |

| Renewals are frozen | Existing policyholders whose policies expire during a lapse cannot renew on schedule. |

| Home sales stall | Mortgage lenders require proof of flood coverage, and a lapse creates a compliance gap. |

| Closing delays accumulate | Real estate transactions dependent on flood insurance proof face postponements. |

The NFIP has experienced 33 lapses since 2017, and each one creates the same chain reaction. If NFIP funding lapses in 2026, an estimated 1,400 home sales could be disrupted daily due to flood insurance coverage uncertainty. That is not a hypothetical. It has happened before, and it will happen again without structural reform.

It is worth noting that NFIP lapses do not cancel policies already in force. Existing flood policies remain active during a federal program lapse. The problem is that new policies and renewals cannot be issued, which creates a bottleneck for anyone whose policy expires or who is purchasing a property during the gap period.

Private flood insurance has emerged as a meaningful alternative. Private carriers can issue and renew policies regardless of NFIP authorization status, which means you can maintain insurance policy continuity even when the federal program is stalled. If your property is in a flood zone, exploring private flood coverage now rather than waiting for the next NFIP reauthorization deadline is a sound strategy.

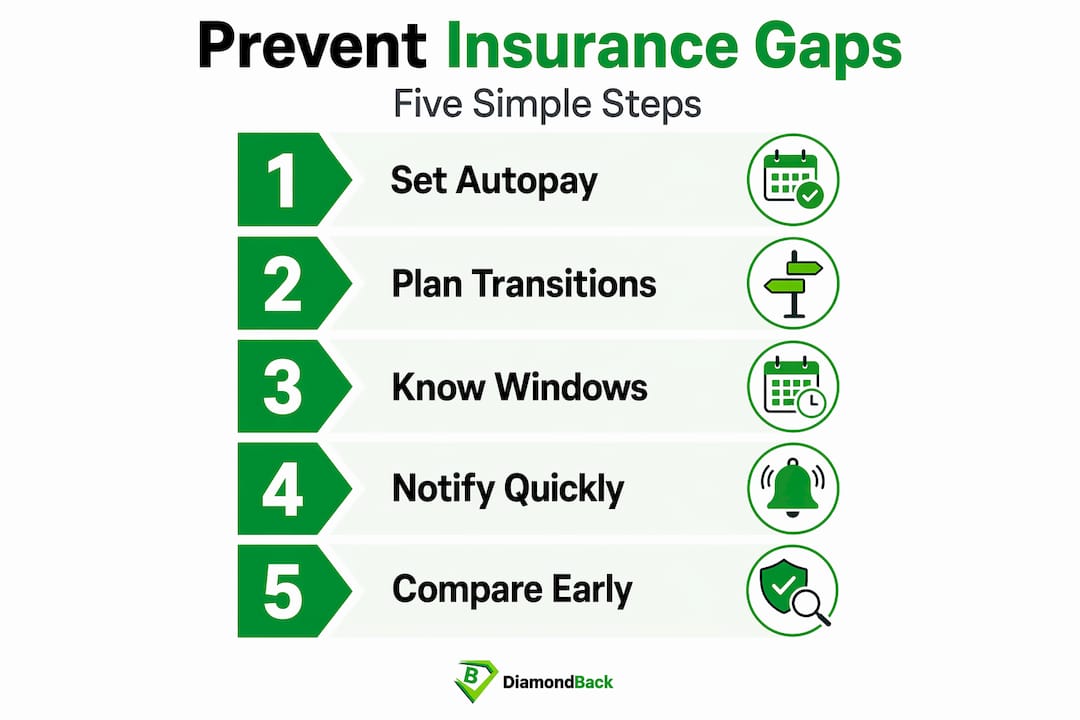

How to avoid insurance gaps before they happen

Prevention is far simpler than recovery. The strategies below are practical, specific, and proven to work for both homeowners and small business owners.

First, set up automatic premium payments wherever possible. Manual payments are where most lapses begin. Autopay removes the human error factor entirely. Pair that with calendar reminders set 60 days before each policy’s renewal date so you have time to review, compare, and renew without rushing.

Second, plan deliberately around life transitions. Coverage gaps frequently arise from life transitions such as job changes, moves, or shifts in eligibility, not simple carelessness. When you change jobs, confirm your new employer’s health coverage start date before your current coverage ends. If there is a gap, a COBRA election or marketplace plan can bridge it. When you move, contact your homeowners insurer immediately to transfer or replace coverage before your closing date.

Third, understand your enrollment windows. Health insurance special enrollment periods are time-limited, and missing them can leave you without options for months. 61.7% of uninsured adults cite affordability as their reason for lacking coverage, but many do not realize that marketplace subsidies or Medicaid may reduce that cost significantly. Knowing what you qualify for keeps coverage within reach.

Fourth, communicate with your insurer and your lender at the first sign of trouble. If you know a payment will be late or a policy is about to lapse, call ahead. Many insurers will work with you on a short extension or reinstatement rather than forcing you through a full new application. Your mortgage lender also needs to know, since early communication gives you time to resolve the issue before force-placed insurance is triggered.

Fifth, compare new quotes before your current policy lapses. Shopping early gives you leverage and time. You can often find better rates without any gap in coverage. Platforms that deliver instant quotes from multiple carriers make this process faster than it used to be. Small business owners managing fleet coverage can also review how much insurance their operation requires to avoid both gaps and unnecessary over-coverage.

Pro Tip: Keep copies of all your current policy documents, premium payment receipts, and insurer contact information in one accessible location. If you ever need to expedite a reinstatement or switch providers quickly, having that documentation ready can cut the process time in half.

The importance of comprehensive insurance is not just about meeting lender requirements or legal minimums. It is about maintaining the financial foundation that protects your home, your business, and your long-term stability.

My perspective on coverage continuity

I’ve seen what happens when people treat insurance as something to deal with later. A homeowner who let their policy lapse for 47 days during a renovation got hit with a water damage claim on day 32. Total out-of-pocket cost: over $28,000. No coverage. No recourse. Just a bill.

What strikes me is how often the logic behind a gap sounds reasonable in the moment. “The renovation is short-term.” “I’m switching jobs anyway.” “The renewal is automatic, right?” These are not careless people. They are busy people who underestimated the mechanics of how coverage works.

The grace period assumption is the most dangerous. Most homeowners policies have no grace period for claims. You can have a grace period for payment, but if a loss occurs during that window before the payment clears, you may still be unprotected. That distinction matters enormously.

What I’ve learned from watching how force-placed insurance plays out is that it is one of the most expensive traps in personal finance. You pay more, get less, and still owe your lender while rebuilding from an uncovered loss. Insurance policy continuity is not a checkbox. It is a core discipline of financial risk management, no different from maintaining your cash reserves or keeping your business liability limits current.

The businesses and homeowners I’ve seen navigate difficult years without catastrophic loss almost always share one trait: they treat insurance renewals with the same attention they give their tax deadlines. Proactive, scheduled, and non-negotiable.

— Vladimir

Protect your coverage with Diamondbackins

If you are a small business owner or fleet operator, maintaining continuous coverage across your vehicles and operations is one of the most direct ways to protect your bottom line. Diamondbackins makes it straightforward to compare quotes from multiple top carriers in minutes, so you can secure or renew coverage before a gap ever forms. Whether you need commercial trucking insurance in Georgia or want to understand your options as a fleet owner, Diamondbackins gives you instant access to tailored quotes without the back-and-forth of traditional brokers. You can also explore the full range of trucking insurance options to find the right fit for your operation. Staying covered should not be complicated. With Diamondbackins, it is not.

FAQ

What happens the moment a homeowners insurance policy lapses?

Coverage ends immediately with no retroactive protection. Any claim for fire, theft, storm damage, or liability that occurs during the lapse period is your full financial responsibility.

How quickly will my mortgage lender respond to a coverage lapse?

Most lenders impose force-placed insurance within 30 to 45 days. This policy protects only the lender’s interest and typically costs two to three times more than standard homeowners coverage.

Can NFIP flood insurance lapses affect my home sale?

Yes. During federal NFIP authorization lapses, new and renewal flood policies cannot be issued. This can stall closings and mortgage approvals that require proof of active flood coverage.

Why do insurance gaps lead to higher premiums later?

Insurers treat a coverage history with gaps as a higher risk profile. When you reinstate or apply for a new policy after a lapse, expect stricter underwriting criteria and elevated rates.

What is the fastest way to prevent an insurance coverage gap?

Set up automatic premium payments and review each policy 60 days before its renewal date. For life transitions like job changes or moves, confirm new coverage start dates align exactly with the end of your existing policy.

Recommended

- Optimize your fleet: why reviewing insurance coverage saves money

- Truck Gap Insurance: Protecting Your Fleet from Financial Gaps

- Protect your trucks: gap insurance explained for fleet owners

- Securing Your Future Workers’ Compensation Insurance for the Self-Employed with DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes