Insurance aggregation is defined as the consolidation of multiple insurance policies, claims, or agencies under a single organized platform or contractual framework that simplifies access, comparison, and negotiation of insurance products. Whether you are a fleet manager comparing commercial trucking coverage or an independent agent seeking better carrier appointments, understanding insurance aggregation explained in full gives you a measurable advantage. The concept operates on two distinct levels: consumer-facing digital platforms that gather quotes from multiple insurers in real time, and industry-facing agency alliances that pool premium volume to unlock better commission terms. Both models reduce friction, cost, and administrative burden in ways that traditional single-carrier shopping simply cannot match.

What is insurance aggregation and how does it work?

Insurance aggregation, known in the industry as either an online marketplace model or an agency alliance model, functions by centralizing the insurance buying or selling process. On the consumer side, digital platforms reduce search time by consolidating insurer quotes into a single interface where you enter your data once and receive multiple real-time offers. This matters because the traditional process of contacting five carriers separately, waiting for callbacks, and comparing mismatched quote formats wastes hours that most business owners do not have.

On the agency side, insurance aggregation works differently but follows the same core logic. Independent agents join aggregator organizations that pool premium volume to negotiate favorable carrier appointments, higher commission tiers, and profit-sharing arrangements that a solo agency could never secure alone. Think of it as collective bargaining for insurance professionals. A single independent agent writing $500,000 in annual premium has limited leverage with a national carrier. An aggregator representing 200 such agents writing $100 million in combined premium has significant leverage.

The operational mechanics for consumers involve carrier rating engines integrated directly into the aggregator platform. When you submit your vehicle details, business type, or coverage requirements, the platform queries multiple carrier APIs simultaneously and returns ranked quotes within seconds. For trucking and commercial fleet businesses, this means comparing liability limits, cargo coverage, and physical damage options across carriers like Progressive, Nationwide, or Travelers without filling out separate applications for each.

Pro Tip: When using a consumer-facing aggregator, always verify that the carriers listed are admitted in your state and that the coverage types match your specific operational needs, not just the premium price.

Agency-side aggregators also provide tools beyond market access. Many supply CRM software, agency management platforms, and compliance training resources that reduce the administrative overhead of running an independent book of business. This combination of market access and operational support is what separates a quality aggregator from a simple referral network.

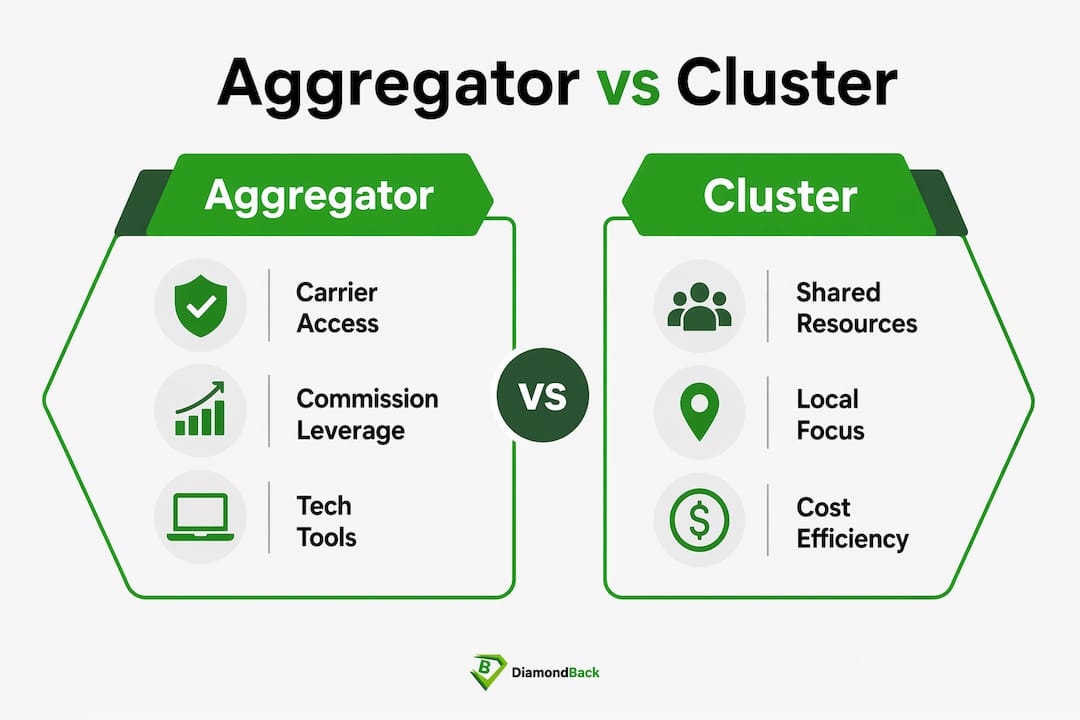

How do aggregators, clusters, and networks differ?

These three terms are frequently used interchangeably, but they describe meaningfully different structures. The primary distinction is intent: clusters share resources, aggregators negotiate market access and commissions, and networks prioritize collaboration and training.

| Model | Primary Focus | Scale | Key Benefit |

|---|---|---|---|

| Insurance cluster | Resource sharing among regional agencies | Local or regional | Reduced overhead costs |

| Insurance aggregator | Negotiating carrier appointments and commissions | National | Better market access and commission rates |

| Agency network | Agent collaboration, training, and compliance | Varies | Professional development and peer support |

A cluster is typically a group of geographically close agencies that share office space, staff, or technology costs. They may or may not negotiate collectively with carriers. An aggregator operates at a national scale and exists specifically to leverage collective premium volume for better carrier terms. An agency network, by contrast, may not negotiate carrier contracts at all. Its value lies in mentorship programs, compliance guidance, and shared marketing resources. Knowing which model you are evaluating matters before you sign any membership agreement, because the contractual obligations and financial structures differ substantially across all three.

What is insurance aggregation in policy claims?

Beyond platforms and agency alliances, insurance aggregation has a third meaning that directly affects how your claims are paid. An aggregation clause is a provision in an insurance policy that consolidates multiple related claims under a single unifying factor, treating them as one event for the purpose of applying deductibles and coverage limits.

Aggregation clauses are strategic mechanisms that determine whether a series of claims collapse into one or remain separate, depending entirely on the contractual language defining the unifying factor. Common unifying factors include “act or occurrence,” “originating cause,” and “series of related acts.” Each phrase produces a different legal outcome, and courts have ruled differently on each.

The practical implications for policyholders are significant:

The benefit of aggregation is that multiple related claims trigger only one deductible or retention rather than one per claim. For a trucking company facing several cargo damage claims from a single loading error, aggregation could mean paying one $10,000 deductible instead of five separate ones.

The risk is that a single aggregate limit can be exhausted faster when multiple claims are consolidated. If your policy carries a $1 million aggregate and five claims are treated as one event totaling $950,000, you have only $50,000 of remaining coverage for the rest of the policy period.

“Aggregation is never implied but must be evidenced. The precision of aggregation clause language directly affects whether claims consolidate or fragment under your policy.” — WTW Insurance Insights

Working with a knowledgeable broker before binding coverage is the most effective way to understand how your policy’s aggregation clause will behave in practice. Ask specifically which unifying factor the policy uses and request examples of how past claims were treated under that language.

What are the benefits of joining an insurance aggregator for independent agencies?

For independent agents, the decision to join an aggregator involves weighing concrete advantages against real contractual obligations. The benefits are substantial, but they require careful evaluation before committing.

The primary advantage is carrier access. Many national and specialty carriers will not appoint small independent agencies that lack sufficient premium volume. An aggregator solves this by granting member agencies access to carriers and product lines they could not reach independently. This directly expands the coverage options you can offer clients, which is a competitive differentiator in commercial lines like trucking, construction, and professional liability.

Commission improvement is the second major benefit. Aggregators leverage collective premium volume to negotiate commission tiers that individual agents cannot access. A carrier might pay a solo agent 10% on commercial auto. The same carrier might pay an aggregator’s members 13% based on the group’s combined volume. Over a full book of business, that difference compounds significantly.

Operational tools represent a third category of value. Many aggregators provide member agencies with agency management systems, marketing templates, E&O coverage options, and continuing education resources. These reduce the cost and complexity of running a compliant, professional operation.

The considerations are equally important to understand before signing:

-

Commission sharing is standard. Aggregators retain a portion of the commissions they negotiate on your behalf. The net commission you receive after the aggregator’s override may or may not exceed what you earned before joining.

-

Contract lock-in effects are a real risk. Some aggregator agreements include provisions that transfer carrier appointments to the aggregator’s name. If you leave the aggregator, you may lose those appointments entirely, forcing you to rebuild carrier relationships from scratch.

-

Member autonomy varies by organization. The best aggregators maintain member agency identity and allow you to operate independently while accessing group benefits. Others impose branding requirements or restrict which carriers you can use.

Pro Tip: Before joining any aggregator, request a complete copy of the membership agreement and have an attorney review the carrier appointment language and exit provisions. The cost of that review is far less than the cost of losing your book of business.

How does insurance aggregation simplify buying for businesses?

For individuals and businesses purchasing insurance, the consumer-facing aggregation model delivers practical benefits that directly reduce the time and cost of securing coverage. Online aggregators consolidate insurer quotes into a single interface, eliminating the need to contact multiple carriers separately and compare incompatible quote formats.

The simplification works across several dimensions that matter to fleet operators and small business owners:

Single data entry is the most immediate benefit. You provide your business details, vehicle information, and coverage requirements once. The platform distributes that data to multiple carriers and returns ranked quotes for direct comparison. For a trucking company comparing liability, cargo, and physical damage coverage across five carriers, this alone saves hours of administrative work.

Wider product selection follows naturally from the aggregation model. Because the platform queries multiple carriers simultaneously, you see coverage options and pricing tiers that you might never encounter through a single-carrier or single-agent relationship. This is particularly valuable for transportation and fleet businesses where coverage requirements vary significantly by cargo type, route, and vehicle class.

Cost transparency is a third benefit. Seeing multiple quotes side by side makes it easier to identify whether a premium difference reflects a genuine coverage difference or simply a carrier pricing strategy. This transparency supports better purchasing decisions.

One important limitation to understand: quotes from online aggregators are estimates. Actual premiums can change after underwriting verifies your driving records, vehicle inspections, or claims history. Treat the initial quote as a reliable starting point for comparison, not a guaranteed final price. For freight and logistics businesses, Diamondbackins provides instant freight coverage access that reflects this same aggregation principle applied specifically to commercial transportation needs.

Key takeaways

Insurance aggregation works because it centralizes the insurance process, whether for consumers comparing quotes or agencies negotiating carrier access, reducing cost and complexity at every stage.

| Point | Details |

|---|---|

| Two distinct models exist | Consumer platforms compare quotes; agency aggregators negotiate carrier access and commissions. |

| Aggregation clauses affect claims | Consolidating claims under one event reduces deductibles but risks exhausting aggregate limits faster. |

| Aggregators differ from clusters and networks | Each model has a distinct purpose: resource sharing, market access, or professional collaboration. |

| Agency contracts carry real risks | Commission sharing and carrier appointment lock-ins require careful review before joining. |

| Consumer quotes are estimates | Final premiums depend on underwriting verification of driving, asset, and claims data. |

Why I think most businesses underestimate aggregation’s full scope

Most conversations about insurance aggregation stop at the consumer platform level. Someone discovers they can compare five quotes in three minutes instead of making five phone calls, and they call that the whole story. After years of working in and around commercial insurance, I find that framing incomplete in ways that cost businesses real money.

The aggregation clause in your policy language is where the stakes get highest, and it is the dimension most business owners never read. I have seen trucking companies face claim scenarios where the difference between “originating cause” and “act or occurrence” language determined whether they paid one deductible or six. That is not a technicality. That is a five-figure financial difference that hinges on three words in a policy document most people sign without reading.

On the agency side, I think the industry is moving toward managed agency organizations and platform cooperatives that blend the best features of aggregators and networks. The agencies that will thrive are those that use aggregator relationships to access markets while retaining enough contractual independence to exit cleanly if the relationship stops serving them. Signing without reading the exit provisions is the single most common mistake I see independent agents make.

For consumers and fleet businesses, the practical advice is straightforward. Use aggregation platforms to generate your comparison set, then work with a broker who understands your specific operational risk to finalize coverage. The platform gives you market intelligence. The broker gives you coverage precision. You need both.

— Vladimir

See how Diamondbackins puts aggregation to work for your fleet

Diamondbackins applies the core principles of insurance aggregation directly to commercial trucking and fleet coverage. The platform queries multiple top-rated carriers simultaneously, returning real-time quotes you can compare and purchase in minutes without paperwork delays or broker callbacks. For fleet managers and owner-operators who need reliable coverage without the administrative burden of traditional insurance shopping, Diamondbackins delivers the speed and transparency that the aggregation model promises. Explore commercial trucking insurance in Georgia and see how quickly you can secure the right coverage for your operation. You can also review online platform cost savings to understand how aggregation-based purchasing compares to traditional methods for fleet businesses.

FAQ

What is insurance aggregation in simple terms?

Insurance aggregation is the process of consolidating multiple insurance quotes, policies, or agency resources under one platform or framework to simplify comparison, purchasing, or negotiation. It applies both to consumer-facing quote platforms and to agency alliances that pool premium volume for better carrier terms.

How does an insurance aggregator differ from a broker?

A broker represents you as the buyer and advises on coverage selection, while an aggregator is a platform or organization that consolidates quotes or carrier access from multiple insurers. Many consumers use both: an aggregator to generate comparison quotes and a broker to finalize coverage details.

Are quotes from insurance aggregators accurate?

Aggregator quotes are estimates based on the information you provide at the time of entry. Final premiums are confirmed after underwriting reviews your driving history, vehicle details, and claims record, which can result in adjustments to the initial figure.

What should agencies check before joining an aggregator?

Agencies should review commission sharing structures, carrier appointment ownership language, and exit provisions before signing any aggregator agreement. Contract lock-in effects can result in losing carrier appointments if you leave, so legal review of the membership agreement is strongly recommended.

What is an aggregation clause in an insurance policy?

An aggregation clause is a policy provision that consolidates multiple related claims into a single event for the purpose of applying deductibles and coverage limits. The unifying factor defined in the clause, such as “originating cause” or “act or occurrence,” determines whether claims are treated as one or separately.