An insurance binder is defined as a temporary insurance contract that legally confirms your coverage is active before the full policy is issued. If you have ever closed on a home, financed a commercial truck, or started a new business operation, you have almost certainly needed one. The binder solves a real timing problem: you need proof of coverage today, but the formal policy paperwork takes days or weeks to finalize. Understanding the insurance binder meaning, what it covers, and how it differs from other documents protects you from gaps that can cost you significantly.

What is an insurance binder and how does it work?

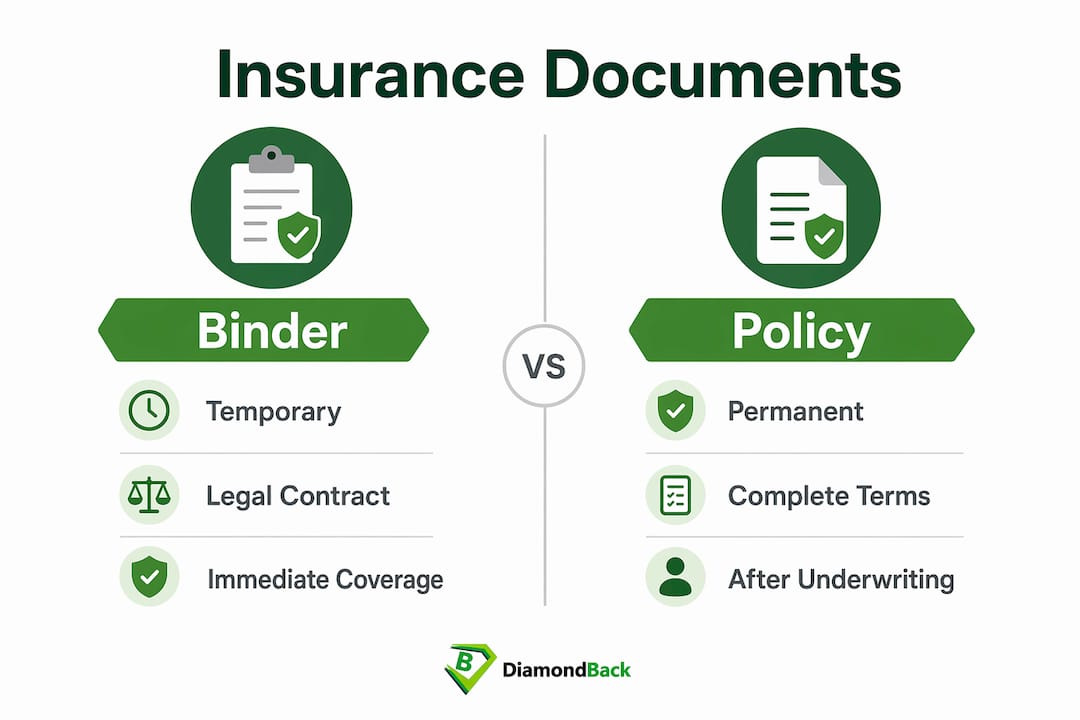

An insurance binder is a legally binding temporary contract issued by a licensed insurance agent or broker to confirm that coverage is in force immediately. It is not a quote, a summary, or a placeholder. It is an enforceable agreement that commits the insurer to the coverage described from the moment it is issued.

The binder closes the timing gap between needing coverage immediately and receiving the full policy later. A mortgage lender will not release funds without proof that the property is insured. A freight broker will not dispatch a load without confirmation that the carrier holds active liability coverage. The binder satisfies both requirements on the spot, allowing transactions to move forward without delay.

Only licensed agents or brokers authorized by the insurer can legally issue a binder. This matters because a binder issued by someone without binding authority is not valid coverage, regardless of what the document says. When you receive a binder, confirming the issuing agent’s authority is the first step you should take.

What does an insurance binder typically cover?

The definition of insurance binder includes specific components that make it function as valid proof of coverage. A properly issued binder contains the named insured, a description of the covered property or operations, the effective start date and time, key coverage limits, applicable deductibles, and any major conditions or endorsements temporarily applied. These details allow lenders, brokers, and other third parties to rely on the document with confidence.

The coverage limits stated in the binder carry full legal weight during the binder period. If a covered loss occurs before the formal policy is issued, the claim is handled under the binder’s terms. This means the limits, deductibles, and exclusions listed in the binder are the ones that apply, not the terms you may have discussed verbally or expected to appear in the final policy.

Pro Tip: Review your binder the same day you receive it. Errors in the named insured, coverage limits, or effective date are far easier to correct before a claim occurs than after one is filed.

Conditions and endorsements in a binder may differ slightly from the final policy. Insurers sometimes apply standard conditions temporarily while underwriting is completed. You should compare the binder terms against your final policy when it arrives and flag any discrepancies to your agent immediately. Careful review of binder details prevents disputes that can surface during claim handling.

Insurance binder vs policy vs certificate of insurance

These three documents serve different purposes, and confusing them creates real problems. The table below clarifies the key distinctions.

| Document | Purpose | Creates coverage? | Duration |

|---|---|---|---|

| Insurance binder | Temporary proof of active coverage | Yes | 30 to 90 days |

| Full insurance policy | Permanent, comprehensive contract | Yes | Policy term (typically 1 year) |

| Certificate of insurance | Summary of existing coverage for third parties | No | Reflects underlying policy |

A certificate of insurance summarizes existing coverage but does not create coverage itself. If the underlying policy is canceled, the certificate becomes worthless, even if it shows a future expiration date. A binder, by contrast, is the coverage. It is the contract, not a summary of one.

The full insurance policy is the permanent, legally comprehensive document that replaces the binder once underwriting is complete. It contains the complete terms, exclusions, endorsements, and conditions that govern your coverage for the entire policy period. The binder is intentionally streamlined because speed is the priority at issuance. The policy fills in every detail the binder leaves general.

For trucking and transportation professionals, understanding this distinction matters when a freight broker or shipper requests proof of insurance. A certificate of insurance is typically what they want to keep on file. A binder is what you need when coverage is brand new and the certificate has not yet been generated. Knowing which document applies to which situation keeps your operations moving without unnecessary delays. You can review essential insurance documents for truckers to understand how each document fits into your compliance requirements.

How long does an insurance binder last?

A binder is typically valid for about 30 days but can extend up to 90 days depending on the insurer and state regulations. This window gives the insurer time to complete underwriting, prepare the formal policy documents, and deliver them to the insured without leaving a coverage gap.

State law plays a significant role in binder duration. Florida, for example, limits binders to 60 days unless the insurer issues an extension. Other states follow different rules, and some allow oral binders in addition to written ones, though written binders are always preferable for documentation purposes. Knowing your state’s rules prevents you from assuming coverage is still active when the binder has legally expired.

A binder ends when the full policy is issued, when the binder period expires, or when coverage is canceled under applicable contract terms. If the insurer decides not to issue a policy after reviewing the full application, the binder coverage ends and you are left without protection. This scenario is uncommon but real, particularly in high-risk commercial lines where underwriting scrutiny is higher.

The risks of a coverage gap after binder expiration are significant. A trucking company operating without active coverage faces regulatory penalties, potential loss of operating authority, and full personal liability for any accidents during the uninsured period. If your binder is approaching expiration and you have not received your formal policy, contact your agent immediately to request an extension or confirm the policy issuance timeline.

Practical uses of insurance binders for homeowners and businesses

Insurance binders appear in several high-stakes situations where coverage must be confirmed before a transaction can close or an operation can begin.

1. Mortgage closings for homeowners. Homeowners insurance binders provide temporary proof of coverage required by lenders before releasing mortgage funds. The lender needs confirmation that the property is insured from the moment ownership transfers. The binder satisfies this requirement while the full homeowners policy is being finalized, often issued the same day the first premium is paid.

2. New commercial vehicle or fleet coverage. When a trucking company adds a new vehicle to its fleet or launches operations, it needs proof of insurance before the truck can legally operate. The binder confirms active coverage immediately, allowing the driver to get on the road while the policy is being processed. Platforms like Diamondbackins are built specifically for this scenario, providing instant binding for commercial trucking operations.

3. Business transactions and contract requirements. Businesses entering contracts, leasing commercial space, or bidding on projects often need to show active coverage before the deal closes. A binder provides that proof on the same day coverage is agreed upon, preventing delays that could cost the business the contract.

4. Underwriting and downstream scheduling. Binders trigger downstream underwriting and closing activities. Once a binder is issued, lenders schedule appraisals, attorneys prepare closing documents, and freight brokers confirm dispatch. Any errors in the binder ripple through all of these processes. Corrections made promptly after binder issuance prevent compounding problems later.

5. Freight and logistics operations. Carriers operating in freight and logistics need active coverage confirmed before each load. Understanding how freight insurance coverage works alongside binders helps carriers stay compliant and avoid costly gaps.

Pro Tip: When you receive a binder for a business transaction, share it immediately with all parties who need it. Lenders, brokers, and attorneys often have their own review timelines, and delays in sharing the document can push back closing dates.

Key takeaways

An insurance binder is a legally enforceable temporary contract that provides active coverage from the moment it is issued, making it the most time-sensitive document in the insurance process.

| Point | Details |

|---|---|

| Binder is a legal contract | A binder creates real coverage immediately, not a summary or placeholder document. |

| Coverage limits apply during binder period | Claims during the binder period are settled under the binder’s stated terms, not the final policy. |

| Duration is 30 to 90 days | Binders expire by state law or policy issuance; gaps after expiration carry serious legal and financial risk. |

| Binder differs from a certificate | A certificate of insurance summarizes existing coverage but does not create it; a binder does both. |

| Review binder details immediately | Errors in coverage terms or named insured must be corrected before a claim occurs, not after. |

Why I treat every binder like a policy in miniature

After years of working with trucking and transportation insurance, the single most consistent mistake I see is treating a binder as a formality. Operators receive it, file it, and assume the real coverage details will sort themselves out when the full policy arrives. That assumption has cost businesses real money.

A binder is an enforceable contract the moment it is issued. The limits it states are the limits that apply if a loss occurs on day two of coverage. I have seen cases where a coverage limit was entered incorrectly in the binder, the insured never reviewed it, a claim occurred during the binder period, and the settlement was based on the wrong limit. The insured had no recourse because the binder was the operative contract at the time of loss.

The issuing authority question is equally important and equally overlooked. Not every person who hands you a binder has the legal authority to bind coverage on behalf of the insurer. Binders must come from persons with clear risk-binding rights. If you are working with a new agent or a broker you have not used before, ask directly whether they have binding authority for the insurer named on the document. It is a straightforward question that protects you completely.

My practical advice is to treat the binder review as a non-negotiable step in your coverage process. Verify the named insured matches exactly. Confirm the effective date and time are correct. Check that the coverage limits match what you agreed to. If anything is off, call your agent the same day. Discrepancies between binder and final policy are far easier to resolve before a claim than during one.

— Vladimir

Get instant coverage binding with Diamondbackins

When your trucking operation needs proof of coverage today, waiting days for a policy to process is not an option. Diamondbackins provides instant online quotes from multiple top insurers, allowing you to compare options and bind coverage in minutes.

Whether you are adding a new truck to your fleet, launching a new operation in Georgia, or responding to a freight broker’s coverage requirement, Diamondbackins delivers the speed and transparency you need. The platform is built for trucking and transportation professionals who cannot afford coverage delays. Secure your commercial trucking insurance in Georgia and get your binder issued the same day.

FAQ

What is an insurance binder in simple terms?

An insurance binder is a temporary legal contract that confirms your insurance coverage is active before the full policy is issued. It provides immediate proof of coverage for lenders, brokers, and other parties who require it.

How long is an insurance binder valid?

A binder is typically valid for 30 days but can extend up to 90 days depending on the insurer and state law. Florida, for example, limits binders to 60 days unless an extension is issued.

Does an insurance binder replace the full policy?

No. A binder provides temporary coverage while the full policy is being finalized. Once the insurer issues the complete policy document, the binder is replaced and the policy’s full terms govern your coverage.

What is the difference between a binder and a certificate of insurance?

A binder creates active coverage and is a legal contract. A certificate of insurance only summarizes existing coverage for third parties and does not create coverage on its own.

Who can issue an insurance binder?

Only licensed insurance agents or brokers with explicit authority from the insurer can legally issue a binder. A binder from someone without binding authority does not constitute valid coverage.

Recommended

- The Essential Guide to General Liability Insurance for Small Businesses – Diamondback Insurance – Solutions with Instant Online Quotes

- Navigating Your Coverage: The Boat Insurance Calculator by DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- What Does Workers’ Compensation Insurance Cover A Comprehensive Guide by DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- Unveiling the Coverage Spectrum of General Liability Insurance with DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes