You assume your general liability policy has your cargo covered. Most fleet owners do. That assumption can cost you six figures in a single bad week. Motor truck cargo insurance is a separate, specialized policy that protects the freight in your care from the moment you accept it until the moment it’s delivered. Federal law already holds you liable for cargo loss or damage, so the real question is not whether you need this coverage but whether the coverage you carry is strong enough to protect your operation.

Table of Contents

- Defining motor truck cargo insurance

- How coverage works: Triggers, limits, and exclusions

- Optimizing your policy: Customizing coverage for your fleet

- Cost factors and premium management in 2026

- What most fleet managers get wrong about motor truck cargo insurance

- Get the right motor truck cargo insurance for your fleet

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Strict liability applies | Federal regulations hold carriers strictly liable for cargo loss or damage unless they prove otherwise. |

| Coverage gaps are common | Relying on minimum required limits or misunderstanding exclusions can leave fleets exposed. |

| Quarterly policy reviews matter | Regular updates help align insurance with changing cargo values and risks. |

| Technology lowers costs | Using telematics and other safety technology can reduce premiums noticeably for fleets. |

| Choose coverage wisely | Selecting all-risk policies with proper endorsements provides broader protection than named-peril plans. |

Defining motor truck cargo insurance

Motor truck cargo insurance is a commercial policy that covers freight or cargo while it is being transported by a for-hire motor carrier. It responds when cargo in your truck is damaged, lost, stolen, or destroyed during transit. This is different from physical damage coverage, which protects your truck, and different from general liability, which responds to third-party bodily injury or property damage. Understanding insurance options for trucking companies starts with knowing that cargo coverage stands alone as its own line of protection.

Who carries the legal liability for freight? The answer is you, almost always. Coverage is triggered under the Carmack Amendment (49 U.S.C. §14706), which holds motor carriers strictly liable for cargo loss or damage unless proven otherwise. That means the burden of proof falls on you, not the shipper, to demonstrate why a claim should not be paid. Very few defenses are available: acts of God, acts of public enemies, shipper error, inherent defect in the cargo, or public authority. Outside of those narrow exceptions, you owe the shipper full value.

For household goods carriers, federal law sets minimum cargo limits at $5,000 per vehicle and $10,000 per occurrence. For other freight types, there is no universal federal minimum, but that does not mean you are free from risk. If you are wondering how much truck insurance you need, the honest answer is almost always more than the legal minimums suggest.

The phrase “care, custody, and control” defines when your cargo liability begins and ends. Liability attaches the moment you accept a shipment and continues until proper delivery is complete. If freight is damaged while sitting on your dock waiting for a driver, you may already be on the hook.

What does motor truck cargo insurance actually cover?

| Covered events | Typically excluded |

|---|---|

| Collision or vehicle upset | Poor or inadequate packaging by shipper |

| Fire, lightning, or explosion | Employee theft (needs separate rider) |

| Theft of entire vehicle load | Inherent vice or natural deterioration |

| Flood or windstorm damage | Unscheduled high-value commodities |

| Refrigeration breakdown (with endorsement) | War, terrorism, or nuclear events |

| Loading and unloading accidents | Contraband or illegal goods |

Knowing what is excluded is just as important as knowing what is covered. Many claims are denied not because the policy is wrong but because the fleet manager never reviewed the exclusions before a loss happened. Connecting with specialized insurance for truckers means working with carriers who understand the freight you haul and can write a policy that fits it precisely.

How coverage works: Triggers, limits, and exclusions

Now that you know what this policy does, it is important to see the mechanics of how coverage is triggered and where gaps often occur.

The “care, custody, and control” standard sounds simple, but claims often fail on packaging disputes or unreported high-value changes. If a shipper uses inadequate packaging and freight arrives broken, the insurer may deny the claim by arguing the damage existed before you took possession. If you accept a load of electronics worth $400,000 but your policy only lists a per-load limit of $100,000, the gap comes out of your pocket. These disputes are common and expensive.

Common claim triggers include vehicle accidents that cause freight to shift or be destroyed, theft of the entire trailer load, refrigeration unit failure during a reefer haul, water intrusion during a rainstorm, and loading or unloading accidents where cargo is dropped or mishandled. Each of these events has specific documentation requirements and deadlines for filing notice to the shipper and insurer.

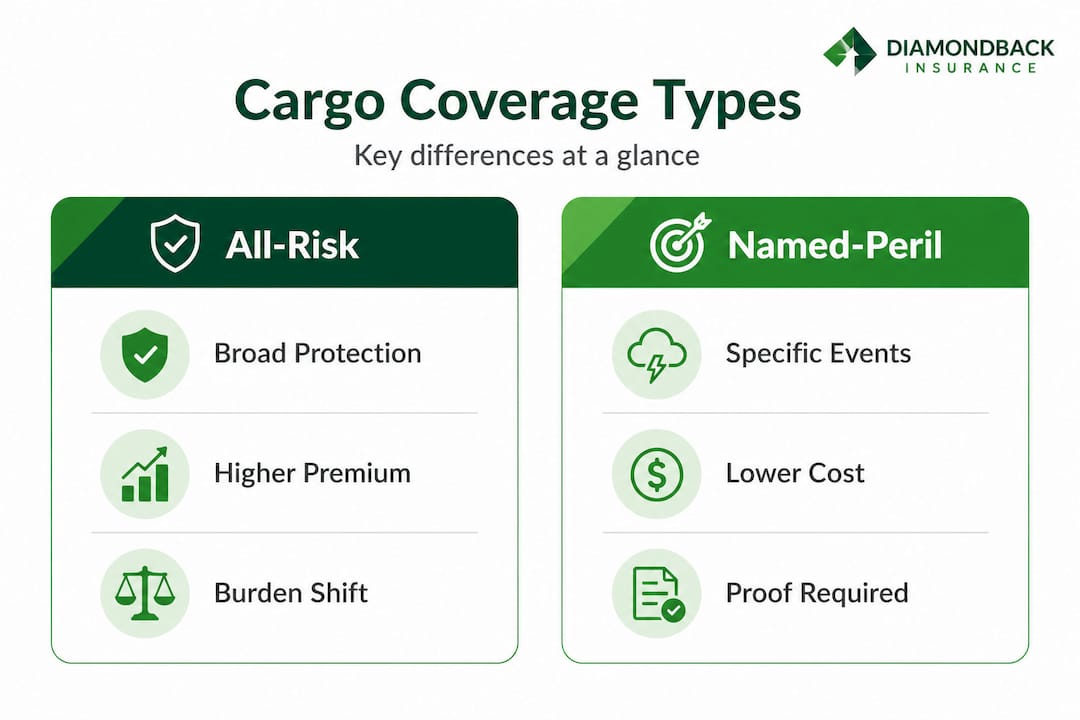

Named-peril vs. all-risk coverage: What’s the difference?

| Coverage type | How it works | Best for |

|---|---|---|

| Named-peril | Only covers events specifically listed | Dry freight, predictable routes |

| All-risk | Covers all events unless excluded | High-value or diverse cargo types |

| Endorsements | Add-on riders for specialized risks | Reefer, electronics, bulk goods |

All-risk coverage costs more, but it shifts the burden of proof in your favor. Under a named-peril policy, you must prove the loss was caused by a listed event. Under an all-risk policy, the insurer must prove the loss falls into an exclusion. That is a significant legal difference when a $250,000 claim is on the table.

Pro Tip: Filing Form BMC-34 with the FMCSA is the standard method for establishing proof of motor truck cargo insurance. Some brokers and shippers require this document before they will assign loads. Keep it current and accessible at all times.

Common exclusions that lead to denied claims deserve your full attention. Policies routinely exclude employee theft without a specific endorsement, loss caused by improper packaging that was not your responsibility to inspect, cargo that is not listed as a scheduled commodity on your policy, and deterioration or spoilage not caused by a covered peril. Reviewing factors affecting insurance rates will also show you how your claims history and the types of freight you haul directly shape what coverage is available and at what price.

Optimizing your policy: Customizing coverage for your fleet

Knowing what can go wrong with claims, the next priority is making your coverage an asset, not a vulnerability.

Your policy limits should reflect the highest single-load value you are realistically likely to carry, not the average load. If you regularly haul freight valued at $150,000 but carry only $100,000 in per-load coverage, you are self-insuring that $50,000 gap every single time. Match limits to max load value, review commodities and exclusions quarterly, and add endorsements for reefer or high-value goods. Brokers reject inadequate certificates of insurance, which means underinsured fleets lose load opportunities.

Quarterly reviews matter more than most fleet managers realize. Your freight mix changes over seasons. A fleet that hauls produce in summer and industrial equipment in winter faces two very different risk profiles. A policy written in January may not accurately reflect the commodities your trucks carry in October. Reviewing your scheduled commodities and your per-load limits every 90 days keeps your coverage aligned with your actual exposure.

Five steps to optimize your motor truck cargo policy:

First, audit your current per-load and per-occurrence limits against the highest-value shipments you have accepted in the past 12 months. Second, review your scheduled commodities list and add any freight types your trucks carry that are not currently listed. Third, identify endorsements that apply to your freight, such as refrigeration breakdown coverage, debris removal, or earned freight coverage. Fourth, check your policy exclusions side by side with your most recent claims or near-misses to spot coverage gaps before they become losses. Fifth, request a certificate of insurance review from your broker to confirm it meets all shipper and broker requirements.

Technology adoption is one of the most underused tools for lowering premiums in trucking. Insurers are actively rewarding fleets that deploy telematics, dashcams, electronic braking systems, and predictive maintenance programs. These tools reduce loss frequency, and lower loss frequency translates directly to lower premiums. Understanding policy differences for fleet managers will show you how technology investment appears differently on large fleet policies versus owner-operator coverage.

Avoiding common coverage pitfalls is equally important. Many fleet managers make the mistake of assuming their broker has updated their policy when cargo volumes or freight types change. Reviewing trucking insurance mistakes will reveal that passive policy management is one of the top reasons fleets face denied claims or coverage shortfalls. Explore top coverages for fleets to understand how cargo coverage integrates with the rest of your insurance tower.

Pro Tip: Always ask your broker to confirm that your certificate of insurance lists the correct commodities and limits before accepting a new shipper relationship. A mismatch between your COI and a broker’s load tender requirements can cost you the load and damage your credibility.

Cost factors and premium management in 2026

With your policy optimized, it is essential to master cost control, especially as insurance rates trend upward in 2026.

Motor truck cargo insurance premiums are driven by several well-defined variables. The value of the cargo you typically carry is the most direct cost driver. Higher cargo values mean higher per-load limits, which means higher premiums. Your claims history is the second major factor. A fleet with two cargo claims in three years will pay significantly more than a fleet with a clean loss record. The type of freight you haul matters greatly: electronics, pharmaceuticals, and alcohol attract higher rates because they are frequent theft targets. Your truck type and age also factor in, as newer equipment with advanced safety features often qualifies for better rates.

| Cost factor | Estimated premium impact |

|---|---|

| High-value cargo (electronics, pharma) | 15 to 25% above base rate |

| Prior cargo claims (2+ in 3 years) | 20 to 40% surcharge |

| Telematics and dashcam adoption | 5 to 15% discount |

| Reefer or temperature-controlled loads | 10 to 20% above base rate |

| Clean DOT safety rating | 5 to 10% discount |

| Fleet size above 20 units | Volume pricing, varies by insurer |

Insurance costs in trucking can reach 10.2 cents per mile for insured fleets when all coverage lines are factored together. That figure puts cargo insurance in direct competition with fuel and maintenance as a major operational cost. Taking it seriously is not optional.

Four strategies to minimize cost increases in 2026: Review your policy limits annually and remove coverage for commodity types you no longer haul. Invest in telematics and safety technology before your next renewal, not after, so you have documented data to show underwriters. Work with a platform that lets you compare truck insurance quotes across multiple carriers, because rate differences for identical risk profiles can vary by 25% or more across insurers. Finally, implement a formal cargo claims prevention program, including driver training on load securing, pre-trip inspections, and delivery documentation, to build a verifiable record of risk management.

Market fluctuations are real. When large cargo claims spike industry-wide, all fleets pay more at renewal time regardless of their individual loss records. Staying ahead of those cycles means reviewing your policy annually, not just at renewal, and understanding where rates are moving before your quote arrives.

What most fleet managers get wrong about motor truck cargo insurance

Here is the uncomfortable reality we see repeatedly: most fleets treat motor truck cargo insurance as a compliance checkbox rather than a risk management tool. They accept whatever limits were written two years ago, renew without reviewing, and assume the policy will perform when it is needed. It often does not perform the way they expect, and the gap between expectation and reality shows up in the worst possible moment.

Minimum legal limits are a trap. The federally mandated minimums for household goods carriers, $5,000 per vehicle and $10,000 per occurrence, were not designed to reflect the actual value of modern freight. A single pallet of consumer electronics can exceed those limits. Running at minimums does not make you compliant in the eyes of the brokers and shippers you want to work with. It makes you a liability they will not assign loads to.

Ignoring quarterly reviews is the second major mistake. Freight mix changes constantly. A fleet that adds a refrigerated trailer in spring needs to revisit its exclusions immediately. A fleet that starts hauling pharmaceutical goods needs to check whether those commodities are even scheduled on the current policy. Missing that review is how a $300,000 claim becomes a $300,000 loss because the freight type was not listed.

Technology is the premium game-changer most fleets are still resisting. Insurers have robust data showing that telematics-equipped fleets generate fewer claims and smaller losses. Adopting this technology early, before your competition does, gives you a pricing advantage at renewal. Understanding why fleet policies differ will show you precisely how technology investment shifts underwriting decisions in your favor. The fleets that are winning on insurance costs right now are the ones that made the technology investment two or three years ago and have the claims data to prove it.

Get the right motor truck cargo insurance for your fleet

Your cargo represents the lifeblood of your business. Every load you haul is a financial commitment to a shipper, and the right insurance coverage ensures that commitment does not become a personal loss. Understanding your policy, reviewing it regularly, and matching limits to real exposure is the foundation of a sound risk management strategy.

Diamondback Insurance makes it straightforward to take the next step. You can find the best trucking insurance by comparing quotes from multiple top-rated carriers on one platform, without spending hours on the phone or waiting days for responses. If you are ready to review your cargo coverage right now, you can get an instant quote in minutes and see your real options side by side. For fleet managers managing cash flow, explore flexible monthly truck insurance options that make premium payments work with your operational budget. Protecting your fleet does not have to be complicated.

Frequently asked questions

Is motor truck cargo insurance mandatory for all fleets?

It is not federally mandated for all fleets, but household goods carriers must meet minimum limits, and most brokers and shippers require coverage above those minimums before assigning loads. The Carmack Amendment creates strict carrier liability regardless of whether cargo insurance is technically required.

What types of losses are usually excluded from motor truck cargo insurance?

Typical exclusions include losses caused by poor packaging, unscheduled high-value cargo, employee theft without a rider, and certain restricted commodities. Claims frequently fail on packaging disputes or high-value cargo that was not reported to the insurer before the haul.

How often should insurance policy limits be reviewed?

Fleet managers should review limits and commodity schedules at least once per quarter. Brokers reject inadequate COIs, so keeping limits current protects both your coverage and your load opportunities.

What’s the difference between all-risk and named-peril cargo coverage?

All-risk policies cover most loss events unless a specific exclusion applies, while named-peril policies only cover events explicitly listed in the policy. All-risk coverage is generally the stronger option for fleets hauling diverse or high-value freight because it shifts the burden of proof to the insurer.

How can fleets lower motor truck cargo insurance premiums?

Adopting telematics, dashcams, and safety technology is one of the most effective ways to reduce premiums, as insurers reward documented loss prevention. Insurance costs reaching 10.2 cents per mile make proactive cost management essential for fleet profitability.