If you run a business that involves vehicles on the road, you have almost certainly encountered the term primary liability insurance, and you may have wondered what it actually covers. Many business owners assume their general liability policy handles everything, only to discover a significant gap after an accident. Understanding what is primary liability insurance, how it functions within the broader insurance hierarchy, and why it matters for your financial protection is not optional knowledge. It is the foundation of any sound risk management plan, especially in commercial trucking and transportation.

Table of Contents

- Key Takeaways

- What primary liability insurance is and what it covers

- Primary liability vs. general liability insurance

- How primary liability insurance works in practice

- Risks of being underinsured and the real benefits of coverage

- Key factors for selecting the right primary liability insurance

- My take on primary liability insurance after years in this space

- How Diamondbackins can protect your business today

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Primary pays first | Primary liability insurance responds to a claim before any excess or umbrella policy activates. |

| On-road coverage only | It covers bodily injury and property damage caused by vehicle operation, not off-road business risks. |

| Noncontributory clauses matter | These endorsements require your insurer to pay claims without pulling in other policies, speeding up settlement. |

| Limits can become inadequate | Rising medical and legal costs mean yesterday’s coverage amounts may leave you exposed today. |

| Both coverages are often required | Many contracts demand both primary and general liability insurance to close coverage gaps completely. |

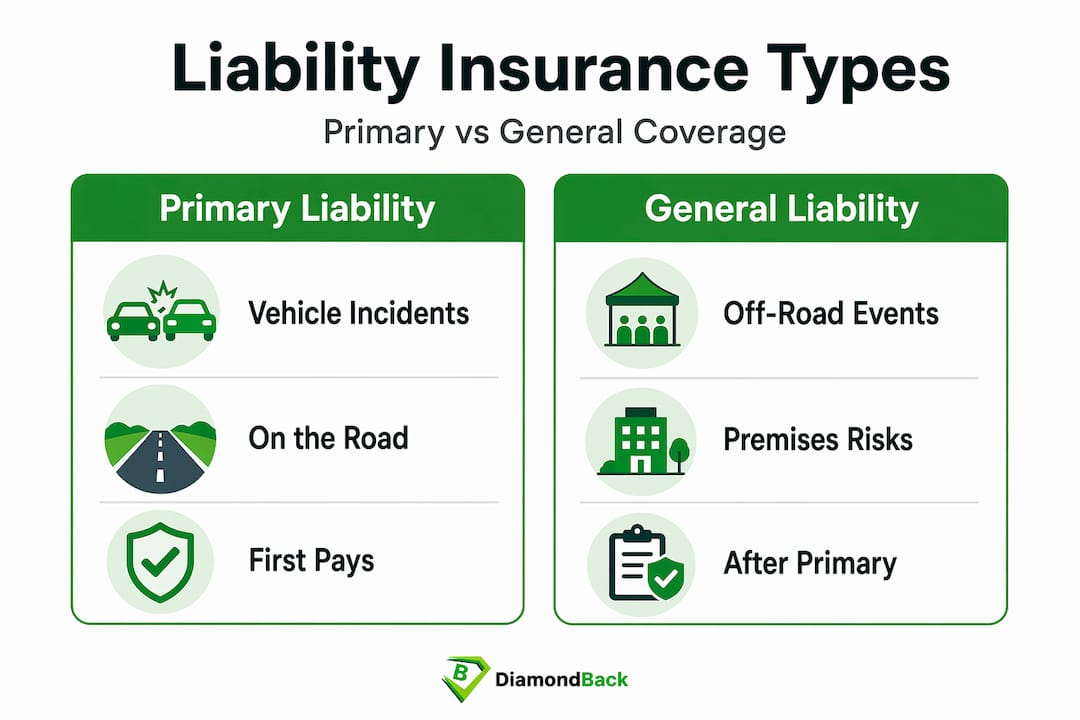

What primary liability insurance is and what it covers

The definition of primary liability insurance is straightforward: it is the first policy to respond when a third-party claim is filed against you. As the first layer of defense, it absorbs the initial financial impact of a loss, paying out up to your policy limits before any secondary, excess, or umbrella coverage is triggered. Think of it as the front line of your financial protection.

In commercial contexts, primary liability insurance is specifically designed to cover bodily injury and property damage that occur while your vehicle is in operation on the road. If a driver operating one of your commercial trucks causes an accident that injures another motorist or damages their vehicle, your primary liability policy is what responds to that claim. Federal regulations require commercial vehicles to carry this type of coverage, which underscores how foundational it is to legal operation.

It is also worth clarifying what primary liability insurance does not cover. It does not address incidents that happen off the road, such as a visitor slipping and falling at your warehouse, or a client being injured on your business premises. Those risks fall under general liability insurance, which is a separate policy entirely. Mixing up these two coverages is one of the most common and costly mistakes business owners make.

Pro Tip: Review your primary liability declaration page carefully to confirm your coverage limits and verify that the policy clearly states “primary” as the coverage position. Some policies issued as excess coverage may look similar but will not respond first to a claim.

Primary liability vs. general liability insurance

Understanding the difference between primary liability and general liability insurance is where many business owners gain real clarity on their risk exposure. Both policies cover third-party claims, but they apply to entirely different situations, and neither one substitutes for the other.

Primary liability insurance covers vehicle-related incidents that occur while your truck, van, or commercial vehicle is being driven. If your delivery driver rear-ends another car on the highway, that claim goes to your primary liability policy. General liability insurance, on the other hand, covers off-road risks such as a customer who slips on a wet floor at your loading dock, property damage caused by an employee working inside a client’s office, or advertising-related injury claims.

The table below illustrates how these two coverages differ across critical dimensions.

| Category | Primary liability insurance | General liability insurance |

|---|---|---|

| Trigger | Vehicle in operation on the road | Business operations off the road |

| Typical claims | Truck accidents, on-road property damage | Slip-and-fall, premises liability, advertising injury |

| Regulatory requirement | Federally mandated for commercial vehicles | Required by many contracts, not always by law |

| Responds to | Third-party bodily injury and property damage from vehicle use | Third-party bodily injury and property damage from business operations |

| Common policyholders | Trucking companies, fleet operators, contractors | All businesses with physical premises or operations |

The confusion arises because both policies share similar language around “bodily injury” and “property damage.” The critical distinction is the trigger. One activates when your vehicle is moving, and the other activates when your business operations are the source of the harm. Shippers and brokers often require carriers to maintain both coverages precisely because some incidents can transition between on-road and off-road triggers, and a gap between the two policies can leave a claim uncovered.

Pro Tip: If you operate commercial vehicles and also manage a physical location where clients or vendors visit, you almost certainly need both coverages. Consult your insurance advisor to map out where each policy’s trigger begins and ends for your specific operations.

How primary liability insurance works in practice

Understanding the claims hierarchy helps you appreciate why the word “primary” carries so much weight. When an accident occurs, the primary insurer manages the claim directly from start to settlement, up to the policy’s limits. Only after those limits are exhausted does an excess or umbrella policy step in. This sequential structure is why getting your primary limits right matters so much from the very beginning.

Here is how the process typically unfolds in a real-world commercial trucking scenario.

- One of your drivers is involved in a collision that injures another driver and damages two other vehicles. The injured party files a claim against your business.

- Your primary liability insurer receives the claim and takes over the investigation, legal defense, and settlement negotiations.

- The insurer pays out the settlement and legal costs up to your policy limit, say $1 million.

- If the total damages exceed $1 million, your excess or umbrella policy activates and covers the difference up to its own limits.

A critical component of how primary liability insurance works is the noncontributory endorsement. Noncontributory coverage means your insurer is required to pay the claim without seeking any contribution from other applicable policies. This matters because without this endorsement, your insurer could attempt to split the claim with another carrier, creating delays, disputes, and added complexity for everyone involved.

Many commercial contracts, particularly those with large shippers, brokers, and general contractors, now mandate that carriers and vendors carry primary, noncontributory liability insurance. This contractual requirement is not bureaucratic boilerplate. It protects the other party by making sure that if something goes wrong, your insurer steps up immediately without pointing fingers at another policy. You can explore trucking insurance requirements in more detail to understand what these contracts typically demand.

Pro Tip: Before signing any shipping or brokerage agreement, read the insurance requirements clause carefully. If the contract specifies “primary and noncontributory,” confirm with your carrier that your policy includes that specific endorsement. Not all standard commercial auto policies include it automatically.

Risks of being underinsured and the real benefits of coverage

One of the most uncomfortable truths in commercial insurance is that many businesses believe they are adequately protected simply because they have a policy in place. The reality is quite different. Standard coverage limits have not kept pace with rising medical expenses, attorney fees, and jury award inflation, which means a policy that felt sufficient five years ago may leave a significant gap today.

Consider a catastrophic accident involving a fully loaded commercial truck. Medical costs for serious injuries can reach seven figures. Add legal fees, lost wages for the injured party, and potential punitive damages, and a $1 million primary policy can be exhausted before the case is even settled. Many businesses are operating on legacy insurance contracts that have not been stress-tested against current economic conditions, creating a false sense of security.

The benefits of having adequate primary liability insurance coverage go beyond simply satisfying a legal or contractual requirement.

Your policy covers the cost of legal defense, which alone can run into six figures for complex commercial liability cases. It protects your business assets from seizure if a court judgment exceeds your personal financial capacity. It preserves your business reputation by allowing you to respond to claims quickly and professionally. And it gives clients and partners the confidence to work with you, knowing you are a responsible operator. Understanding how coverage gaps expose fleets can help you recognize the real financial stakes of underinsurance.

“Liability exposure is dynamic and influenced by inflation and the complexity of legal environments. Standard coverage limits have effectively shrunk, causing underinsurance concerns that businesses often do not recognize until a major claim occurs.”

The layered insurance strategy, where primary liability sits beneath an excess or umbrella policy, is the most effective way to address the risk of catastrophic claims. Your primary policy handles the everyday exposure, while the umbrella policy provides a financial ceiling for worst-case scenarios.

Key factors for selecting the right primary liability insurance

Choosing primary liability insurance is not a decision you should make based on price alone. Several factors deserve careful review before you commit to a policy.

Your policy limits are the first and most critical consideration. Look at the nature of your operations, the value of assets your vehicles could potentially damage, and the bodily injury exposure your fleet carries. A trucking company’s insurance needs differ significantly from those of a landscaping contractor with a single van, and your limits should reflect your actual exposure.

Carrier reputation and claims handling efficiency matter just as much as price. Primary claims handling directly affects how quickly disputes are resolved and how effectively your legal defense is managed. An insurer that is slow to respond or reluctant to settle can cost you more in the long run than a slightly higher premium would have.

Review any contractual obligations before purchasing. If your clients or brokers require primary, noncontributory coverage, verify that the policy you are buying specifically includes that endorsement. Also review your deductible structure carefully, since a high deductible may reduce your premium but increase your out-of-pocket exposure when a claim occurs.

Finally, build in a regular review schedule. Your business changes, your fleet grows, and the legal environment shifts. A policy that fit your operation two years ago may no longer provide the coverage you actually need.

Pro Tip: Treat your annual renewal as an opportunity to reassess your limits against current claim trends, not just a routine administrative task. A brief conversation with your broker about recent jury awards in your region can reveal whether your current limits remain realistic.

My take on primary liability insurance after years in this space

I’ve worked with enough trucking and transportation businesses to know that underestimating primary liability risk is remarkably common. What I’ve consistently observed is that business owners treat primary liability insurance as a compliance checkbox rather than a strategic financial tool. That mindset is where the real danger lives.

In my experience, the businesses that get into serious financial trouble after accidents are rarely the ones without any insurance. They are the ones whose limits were set years ago and never revisited. I’ve seen $1 million limits that felt generous a decade ago prove completely inadequate against modern medical and legal costs, leaving business owners personally exposed in ways they never anticipated.

What I’ve learned is that the claims hierarchy, and specifically the noncontributory endorsement, deserves far more attention than it typically gets. Most small business owners have never heard the term “primary noncontributory” until a shipper’s contract puts it in front of them. At that point, it’s often a scramble to get the right endorsement in place. Getting ahead of that requirement, rather than reacting to it, separates prepared businesses from vulnerable ones.

My honest advice is this: review your current primary liability limits against recent large verdict data in your state, confirm your noncontributory endorsement status, and map your primary coverage against your umbrella policy to make sure there are no gaps between them. Do it now, before a claim forces the conversation.

— Vladimir

How Diamondbackins can protect your business today

When you understand what is primary liability insurance and why it matters, the next logical step is securing coverage that actually matches your exposure. Diamondbackins specializes in commercial trucking and transportation insurance, giving you instant access to quotes from multiple top-rated carriers so you can compare options and choose the coverage that fits your operation, not just the one that fits a generic profile.

Whether you need primary liability coverage for a single commercial vehicle or a full fleet, Diamondbackins makes the process direct and transparent. You can review fleet protection options and get competitive quotes online in minutes, without waiting for a callback or sitting through a sales presentation. If you are a trucking professional in Georgia or anywhere across the country managing commercial vehicle risk, Diamondbackins is built specifically for operations like yours. You can also explore a broader overview of what trucking insurance covers to make sure your policy addresses every exposure your business carries.

FAQ

What is primary liability insurance in simple terms?

Primary liability insurance is the first policy to pay when a third-party claim is filed against you. It covers bodily injury and property damage caused by your vehicle while it is in operation, up to your policy limits, before any excess coverage responds.

Is primary liability insurance required for commercial trucks?

Yes. Federal regulations mandate that commercial motor vehicles carry primary auto liability insurance covering bodily injury and property damage caused during on-road operations. Most shipping and brokerage contracts also require it independently.

What does primary and noncontributory mean on a certificate of insurance?

Primary and noncontributory means your insurer must respond to a claim first and cannot seek contribution from any other insurance policy the additional insured may carry. This simplifies claims and speeds up settlement for all parties involved.

How does primary liability differ from general liability insurance?

Primary liability covers incidents triggered by vehicle operation on the road, while general liability covers off-road business risks such as customer injuries on your premises. Both policies address third-party claims but in entirely different scenarios, and many businesses need both.

How much primary liability coverage does a trucking business need?

Coverage needs vary by fleet size, cargo type, and operating territory, but given rising medical and legal costs, many experts now consider $1 million limits a starting point rather than a ceiling. Review current verdict trends in your state and consider pairing primary coverage with an umbrella policy for complete protection.

Recommended

- Understanding General Liability Insurance vs. Professional Liability Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- Types of liability coverage: protect your fleet and business

- Limited liability coverage explained: safeguard your business and trucks

- The Essential Guide to General Liability Insurance for Small Businesses – Diamondback Insurance – Solutions with Instant Online Quotes