Managing insurance for a trucking fleet is rarely straightforward. Between FMCSA compliance, cargo liability, driver requirements, and contract-specific coverage demands, the complexity can feel overwhelming. Many fleet managers discover too late that buying insurance without expert guidance leads to coverage gaps, missed filings, or premiums that don’t reflect their actual risk profile. Insurance brokers solve this problem by acting as your dedicated advisor, shopping multiple carriers, structuring policies to your exact operational needs, and standing beside you when claims arise. This guide breaks down exactly how brokers work, when they deliver the most value, and how to use that relationship to protect your business and control costs.

Table of Contents

- What insurance brokers do for trucking fleets

- How brokers manage risk and influence insurance costs

- Brokers vs agents vs buying direct: What’s the difference?

- When does a broker add the most value?

- Why the smartest fleet managers treat brokers as strategic partners

- Explore commercial coverage solutions with DiamondBack Insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Brokers expand market access | Insurance brokers can connect you with more carriers—including for hard-to-place trucking risks—than buying direct. |

| Data drives better coverage | A broker uses your fleet’s safety and compliance records to negotiate lower premiums and better terms. |

| Advocacy from quote to claim | Brokers support you through quoting, policy structuring, regulatory filings, and claims—adding lasting value. |

| Partnership mindset pays off | Businesses that treat brokers as strategic partners gain year-round guidance and improved insurance outcomes. |

What insurance brokers do for trucking fleets

A trucking insurance broker is not simply a salesperson who connects you to a policy. They are advisors who design, compare, and negotiate coverage on your behalf, working across multiple insurance carriers to find the right fit for your operation. As intermediaries shopping markets, brokers structure coverage, meet compliance requirements, and advocate for you through claims. That’s a fundamentally different role than what most fleet managers expect.

The core tasks a broker handles go well beyond finding a quote. They align your policies with the specific requirements of your freight contracts, lender agreements, and regulatory bodies such as the FMCSA (Federal Motor Carrier Safety Administration), DOT (Department of Transportation), and UIIA (Uniform Intermodal Interchange and Facilities Agreement). They manage COIs (Certificates of Insurance), which are documents that prove your coverage to shippers and contractors, and handle the filings required by regulators. If you operate box trucks with specific coverage needs, a broker ensures those vehicles are correctly classified and covered.

Brokers also stay with you after the policy is placed. When an accident or cargo dispute occurs, they act as your advocate with the insurer, helping you navigate the claims process and pushing for a fair resolution. This ongoing support is something a direct purchase or a single-carrier agent rarely provides at the same level.

Consider a practical example. A regional carrier wins a new contract with a national retailer. The retailer requires higher liability limits, specific cargo coverage, and a named additional insured on the policy. A broker reviews the contract language, adjusts the coverage structure accordingly, secures the required COI, and confirms all filings are current before the first load moves. Without that broker, the carrier risks losing the contract or operating with inadequate coverage.

“A broker’s value isn’t just in finding a policy. It’s in making sure that policy actually works when you need it most.”

Pro Tip: Ask your broker to review every new freight contract before you sign it. Contract insurance requirements vary widely, and catching a mismatch early is far easier than fixing it after the fact.

How brokers manage risk and influence insurance costs

Having covered the broker’s advisory role, let’s look at how brokers actively affect the coverage and premiums you pay. The price of your fleet insurance is not fixed. Underwriters at insurance companies assess your risk profile and set premiums based on what they find. A skilled broker shapes how that profile looks.

Brokers leverage your fleet’s FMCSA safety data, loss runs (your claims history), maintenance records, and telematics data to present your business as a well-managed, lower-risk operation. Safety records and telematics help brokers build strong risk profiles for underwriters, directly influencing premium offers and insurability decisions. In practical terms, a clean safety record paired with documented maintenance logs can be the difference between a standard rate and a surcharge.

The table below shows how key data points influence underwriting decisions:

| Data point | What underwriters assess | Impact on premium |

|---|---|---|

| FMCSA safety rating | Compliance and inspection history | High |

| Loss runs (3-5 years) | Claims frequency and severity | High |

| Driver MVR records | Individual driver risk | High |

| Telematics data | Speed, braking, and hours of service | Moderate |

| Maintenance logs | Vehicle condition and upkeep | Moderate |

Brokers also help you implement safety programs that reduce claims frequency over time. Fewer claims improve your loss runs, which strengthens your position at renewal. This is a compounding benefit: better safety today means better rates next year.

When your documentation is current and organized, brokers can move faster and negotiate more effectively. Gaps in records, on the other hand, give underwriters reason to apply conservative pricing.

Pro Tip: Keep at least three years of loss runs, current MVR (Motor Vehicle Record) reports for all drivers, and up-to-date maintenance logs. This documentation is your strongest negotiating tool when your broker goes to market on your behalf.

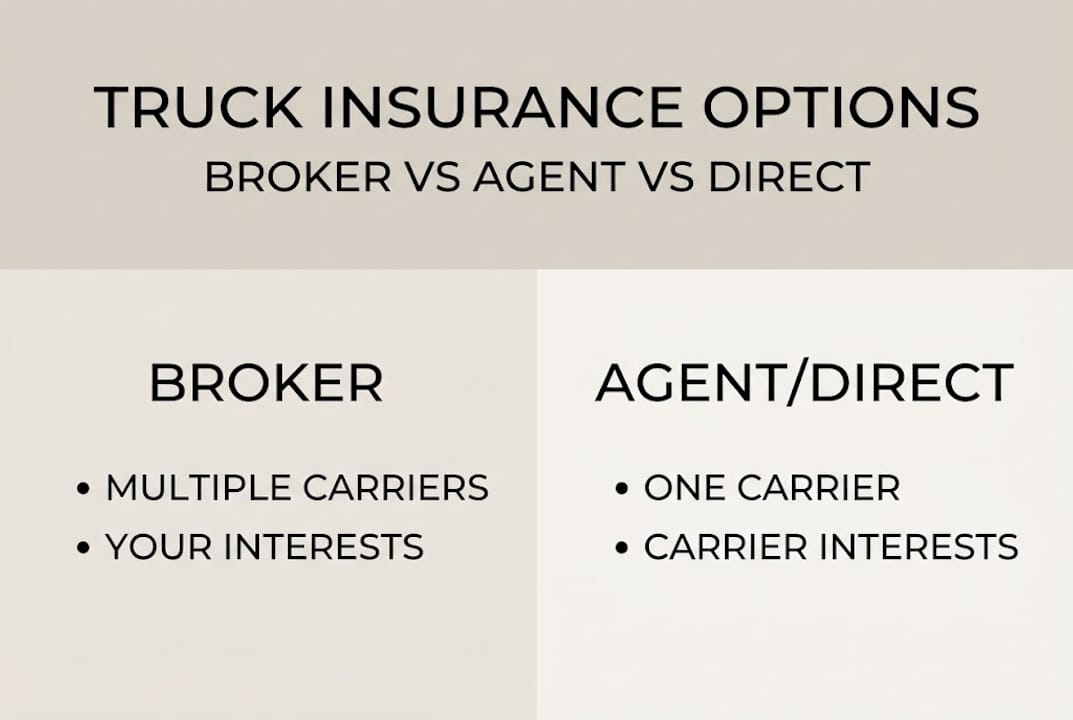

Brokers vs agents vs buying direct: What’s the difference?

To put the broker’s role in context, let’s compare it with how agents and direct insurance purchase work for fleets. The distinction matters because each option carries different levels of market access, flexibility, and ongoing support.

A broker represents your interests. They work with multiple insurance carriers, including wholesale markets for risks that standard carriers won’t touch. Brokers expand market access and can leverage wholesalers, while buyers going direct are limited to a single carrier and receive less advocacy. That broader reach is especially important for trucking operations, where risk profiles can be complex.

An agent, by contrast, typically represents one or a small number of insurers. A captive agent works exclusively for one company, which limits the options they can offer you. An independent agent has more flexibility but still operates within a narrower market than a broker. For straightforward fleets with clean records, an agent may be sufficient. But when your operation has unusual equipment, specialty cargo, or a complicated driver mix, an agent’s market reach may fall short.

Buying direct from an insurer cuts out the intermediary entirely. This can feel efficient, and for simple, low-risk operations it sometimes works. The tradeoff is that you lose the advocacy layer. If your needs change, if a claim becomes contentious, or if you need to meet a new contract’s requirements quickly, you’re managing that alone. Understanding the insurance quote process helps you see where brokers add steps that actually protect you rather than slow you down.

“Brokers matter most when the risk is complex or hard-to-place.”

Here is a quick comparison to clarify the differences:

| Feature | Broker | Agent | Direct purchase |

|---|---|---|---|

| Market access | Multiple carriers and wholesalers | One or a few carriers | Single carrier |

| Represents | Your interests | Insurer’s interests | N/A |

| Claims advocacy | Yes | Limited | No |

| Best for | Complex or growing fleets | Standard, stable risks | Simple, low-risk operations |

When does a broker add the most value?

Now that you’ve seen the big-picture differences, let’s get practical with when hiring a broker gives your business the biggest edge. Not every fleet situation is equal, and brokers deliver outsized value in specific circumstances.

Brokers are indispensable for complex or rapidly changing risks, such as specialized cargo, new DOT authorities, or unusual equipment. If you’re starting a new trucking operation, expanding into new states or regions, or taking on a shipper that requires non-standard coverage terms, a broker’s market access and expertise become critical. Standard carriers may decline your application outright, while a broker with wholesale market connections can often find coverage for new ventures that others cannot.

Here are four scenarios where brokers provide the clearest advantage:

- New fleet start-ups seeking their first DOT authority, where underwriters are cautious about placing coverage without an established safety record.

- Fleets expanding operations into new regions or adding new vehicle types, where existing policies may not extend coverage automatically.

- Specialty cargo haulers transporting hazardous materials, oversized loads, or high-value freight that falls outside standard market appetite.

- Fleets meeting new contract requirements from shippers or brokers who demand specific liability limits, endorsements, or additional insured status.

In each of these scenarios, a broker does more than find a price. They structure the coverage correctly, confirm it meets all requirements, and ensure the policy will actually respond when a claim occurs.

Pro Tip: Disclose every detail of your operation to your broker, including equipment types, cargo categories, driver experience levels, and any prior coverage cancellations. Hidden risks can jeopardize claims or make future coverage harder to secure.

Why the smartest fleet managers treat brokers as strategic partners

Here is a perspective that most articles won’t tell you: treating your broker as a one-time deal finder is one of the most expensive habits in fleet management. The companies that consistently pay less and get better coverage are the ones that keep their broker informed year-round, not just at renewal.

A broker who knows your business deeply can advise you on how a new contract will affect your premiums before you sign it. They can flag when a telematics upgrade might improve your risk profile, or when a carrier’s appetite for your type of freight is shifting. That kind of proactive guidance doesn’t happen in a transactional relationship.

Strategic insurance collaboration means sharing operational changes, safety program updates, and growth plans with your broker on a regular basis. Think of them as part of your risk management team. The broker who understands your five-year growth plan can position your coverage to scale with you, avoiding the scramble that happens when fleets outgrow their policies unexpectedly.

The uncomfortable truth is that most fleet managers only call their broker when something goes wrong or when renewal is due. By then, the leverage to negotiate better terms has already narrowed. The businesses that treat this relationship as ongoing and collaborative consistently come out ahead, both in coverage quality and in cost.

Explore commercial coverage solutions with DiamondBack Insurance

You now understand the real value brokers provide. The next step is putting that expertise to work for your operation.

DiamondBack Insurance specializes in trucking and transportation coverage, giving fleet managers and small business owners access to tailored, cost-effective insurance solutions. Whether you need custom solutions for box trucks or coverage for a mixed commercial fleet, the platform connects you with multiple top insurers in one place. You can get instant quotes online in minutes or work with a broker for custom advice on complex operations. DiamondBack combines the speed and transparency of a modern online platform with the market access and expertise your fleet deserves. Start your quote today and see what the right coverage actually looks like for your business.

Frequently asked questions

How do trucking insurance brokers get paid?

Most brokers earn a commission from the insurer based on the premium placed, not a fee paid directly by you, so using a broker typically does not add to your out-of-pocket cost.

Can a broker help lower my truck fleet insurance premium?

Yes. Brokers use your safety records and data to build a stronger risk profile and access a wider range of carriers, which often results in more competitive premium offers than buying direct.

Do brokers handle COIs and insurance filings for regulatory bodies?

Yes. Brokers structure coverage for compliance and manage Certificates of Insurance along with required filings for DOT, FMCSA, UIIA, and other regulatory bodies as part of their standard service.

When should I not use a broker for truck fleet insurance?

For a standard, simple fleet with a clean record and straightforward coverage needs, buying direct can be faster, though it offers less flexibility and less support if your operation grows or your needs change.

Recommended

- Q&A Blog Post: Box Truck Insurance Near Me

- Q&A Blog Post: Box Truck Insurance Quotes

- Smooth Sailing Ahead: Understanding Boat Insurance with Towing author: DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- Navigating Your Coverage: The Boat Insurance Calculator by DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes