A fleet insurance workflow is the integrated process of managing all insurance-related activities for a commercial vehicle fleet, including policy administration, claims handling, safety documentation, and telematics data sharing. When this process runs on disconnected spreadsheets and phone calls, your premiums reflect it. When it runs on integrated digital systems, your insurer sees a safer, more predictable fleet, and your rates follow. Platforms like Draivn, Oxmaint, and FleetRabbit have demonstrated that data-driven fleet workflows can reduce commercial auto coverage premiums by 15 to 35% within three to six months of sustained data sharing. This guide walks you through every layer of that process.

What are the core components of a fleet insurance workflow?

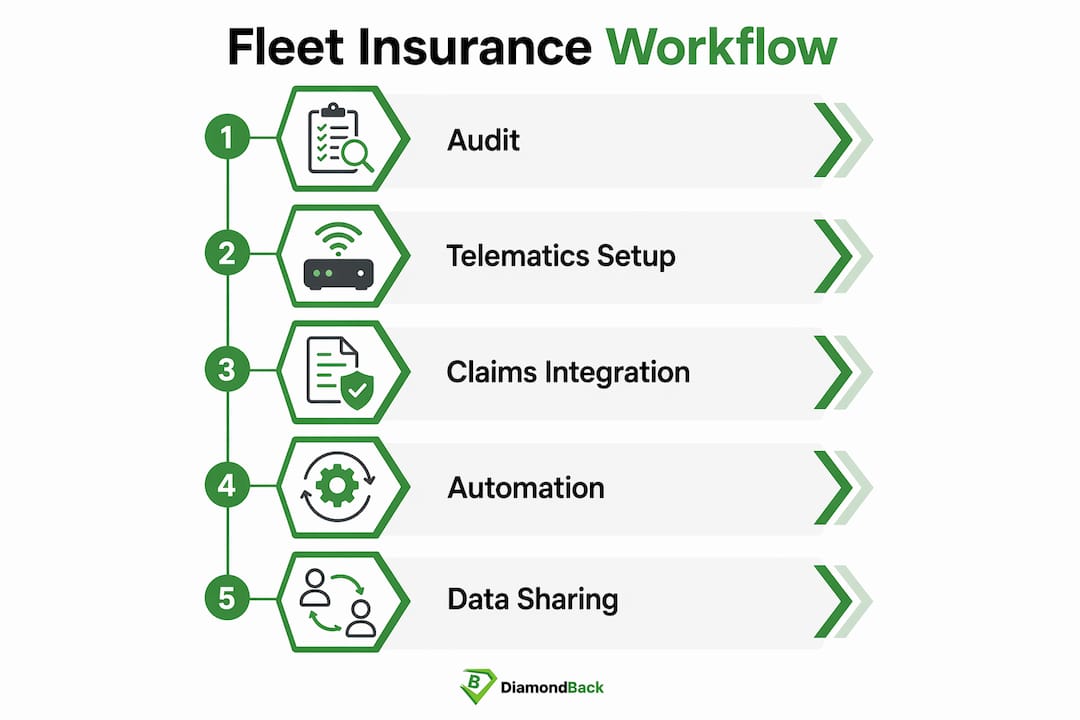

A modern fleet insurance workflow is built on five interconnected layers. Each one feeds the next, and a gap in any layer creates friction that costs you money and time.

Telematics hardware and data capture form the foundation. GPS units, accelerometers, ADAS event sensors, and dash cams generate the raw safety evidence that insurers need to move your fleet from standard risk to preferred risk. Telematics data reveals that fleets often outperform industry loss history averages, enabling 12 to 25% premium reductions when that data is shared in a structured format. That is not a marginal improvement. It is the difference between a profitable quarter and a costly one.

Fleet safety and maintenance management platforms translate raw data into documented compliance. Oxmaint, for example, centralizes inspection records, maintenance logs, and driver training documentation in timestamped archives. Insurers use these archives to verify that your safety culture is real, not just claimed. Proactive digital safety archives shift fleets from standard to preferred risk categories, which unlocks meaningful cost benefits at renewal.

Claims handling integration software connects your drivers, fleet managers, repair shops, and insurers in a single workflow. FleetResponse is one platform built specifically for this purpose, linking incident reports directly to insurer notifications and repair scheduling. Without this connection, claims travel through phone calls and email chains, creating delays and errors that extend downtime.

Insurance communication platforms handle the data exchange between your fleet systems and your insurer or broker. Draivn, which integrates directly with Linxup telematics via API, is a clear example of how data transparency between fleets and insurers closes the traditional information gap that inflates premiums unfairly.

Documentation management systems complete the picture by organizing driver training records, vehicle inspection reports, and incident documentation in formats that underwriters can actually use during risk assessment.

Pro Tip: Request your insurer’s preferred data format before you configure your telematics export. Formatting your safety data to match their intake requirements cuts review time and accelerates any mid-term premium adjustments.

How to implement a fleet insurance workflow step by step

Building this workflow from scratch feels large, but the process is sequential and manageable. Start with what you have, then add layers.

Step 1: Audit your current process. Map every insurance-related task your team performs today, from loss run requests to accident report submissions. Identify where data lives in silos and where tasks require manual re-entry. Most small fleets discover that 60 to 70% of their insurance premium formula is directly controllable through documented safety practices and automation. That audit tells you exactly where to focus first.

Step 2: Install and configure telematics. Choose a telematics provider that supports API-based data sharing with insurance platforms. Linxup’s integration with Draivn is a practical model. Once installed, configure your system to capture ADAS events, hard braking, speeding incidents, and GPS trip data continuously, not just during incidents.

Step 3: Connect your claims workflow. Integrate your fleet management software with a claims handling platform. When a driver reports an incident, the system should automatically generate a First Notice of Loss package, notify your insurer, and initiate repair scheduling. Automated claims reporting with G-force and GPS event capture produces First Notice of Loss packages within minutes, which measurably improves claims cycle times.

Step 4: Automate high-friction manual tasks. Loss run extraction, fleet schedule validation, and accident report submission are the three tasks most commonly handled manually and most easily automated. Configure your platforms to handle these on a schedule, not on demand.

Step 5: Establish ongoing data sharing protocols. Do not wait until renewal to share safety data. Set a monthly cadence for transmitting verified telematics reports and safety documentation to your broker or insurer. Timely sharing of well-packaged safety evidence is critical because waiting until renewal often misses mid-term adjustment opportunities.

Here is a direct comparison of what changes when you move from a manual to an automated workflow:

| Task | Manual workflow | Automated workflow |

|---|---|---|

| Incident reporting | Phone call, then email, then form | Auto-generated FNOL within minutes |

| Loss run extraction | Request submitted, wait 5 to 10 days | Pulled on demand from integrated system |

| Safety data sharing | Annual PDF at renewal | Monthly structured data feed to insurer |

| Driver training records | Paper files or scattered folders | Timestamped digital archive, audit-ready |

| Claims status tracking | Follow-up calls to adjuster | Real-time dashboard visibility |

Pro Tip: Continuous driver safety coaching generates measurable improvements within 90 days. Build a coaching review into your monthly workflow so that telematics data drives behavior change, not just reporting.

What are common mistakes in managing vehicle insurance processes?

Most fleet managers do not fail at insurance because they lack coverage. They fail because their processes are reactive and fragmented.

The most costly mistake is collecting telematics data without sharing it in insurer-accepted formats. Raw GPS logs mean nothing to an underwriter. Your data needs to be packaged into structured reports that match what your insurer’s risk team can actually evaluate. Fleet insurance losses are best contained when telematics data is formatted into insurer-required structures before renewal periods, but many fleets never get there because no one owns that formatting task.

The second major mistake is treating insurance as a renewal event rather than a daily operational activity. Fleet insurance workflows are daily operational activities, not just renewal checklists. Automating incident reporting triggers claim creation and insurer notifications instantly, which is only possible when your systems are connected year-round.

Disjointed communication between fleet managers, drivers, and repair shops is the third common failure point. Siloed communication across fleet, claims, and repair teams causes delays, higher costs, and operational disruptions. A single missed notification can delay a repair approval by days, keeping a vehicle off the road and inflating your loss ratio.

Insufficient documentation of driver training and inspections is equally damaging. Without timestamped records, you cannot prove your safety culture to an underwriter, and you lose your negotiating position at renewal.

Pro Tip: Assign one person in your organization as the insurance workflow owner. This role does not need to be full-time, but it needs to be consistent. Accountability is what separates fleets that capture premium savings from those that do not.

How does integrating fleet operations reduce costs and improve claims outcomes?

The financial case for an integrated fleet insurance workflow is direct. Integrated, data-driven workflows can reduce premiums by 15 to 35% within three to six months of sustained data sharing. That range is wide because it depends on your starting risk profile and how consistently you share verified safety evidence.

Insurance underwriting is shifting from historical loss data to validated real-time telematics data, which means safer fleets can now negotiate better premium rates based on actual performance rather than industry averages. This is a structural change in how commercial auto coverage is priced, and it favors fleets that have their data in order.

On the claims side, automated incident reporting reduces administrative load and fleet downtime significantly. Connecting insurance claims workflows directly with fleet management systems accelerates incident reporting and repair scheduling, which keeps vehicles moving and loss ratios manageable. Unified platforms also eliminate duplicated data entry, which is a quiet but real source of errors in manual workflows.

“Top fleet managers treat insurance workflows as mission-critical operational layers and integrate them deeply into telematics and maintenance platforms.” — FleetResponse, 2026

Fleet insurance premiums are rising due to nuclear verdicts and increased accident frequency across the transportation sector. Fleets with verified safety records see compounded premium reductions of 12 to 25% or more across renewal cycles. That compounding effect is the real long-term value. Each renewal builds on the safety record you documented during the prior term.

You can also review how insurers shape transportation risk to understand which data points carry the most weight in underwriting decisions, so you prioritize collecting and sharing the right metrics.

What coverage options should your fleet insurance workflow track?

A well-built workflow does not just manage processes. It tracks the coverage types your fleet actually needs and flags gaps before they become claims problems.

The core coverage types for most commercial fleets include primary liability, physical damage (collision and comprehensive), motor truck cargo, uninsured and underinsured motorist coverage, and general liability. Each coverage type has different triggers, limits, and documentation requirements. Your workflow should map each vehicle and cargo type to the appropriate coverage and flag any mismatches during policy reviews.

Liability coverage is the non-negotiable foundation. Federal Motor Carrier Safety Administration minimums apply to most commercial fleets, but those minimums rarely reflect your actual exposure. Physical damage coverage protects your asset base, and its value depends on accurate vehicle valuations that your workflow should update at each renewal. Cargo coverage requirements vary by commodity type, so your documentation system needs to track what each vehicle carries and match it to the correct policy endorsement.

Workflows also support timely policy reviews and coverage adjustments. When you add a vehicle, change a route, or hire a new driver, your insurance policy needs to reflect that change immediately. An integrated fleet policy administration system sends those updates automatically rather than waiting for a quarterly review. You can explore the full range of fleet insurance coverage options to confirm your current policy addresses every exposure your operation carries.

Data-driven risk profiles also help you select appropriate coverage limits rather than defaulting to the cheapest option. When your telematics data shows consistent safe driving behavior, you have the evidence to justify higher deductibles in exchange for lower premiums, a trade-off that only makes sense when you can document your actual risk level.

Key takeaways

An integrated fleet insurance workflow, built on telematics data, automated claims handling, and continuous safety documentation, is the most direct path to lower premiums and faster claims resolution for commercial fleets.

| Point | Details |

|---|---|

| Telematics data drives savings | Sharing verified safety data with insurers can reduce premiums by 15 to 35% within six months. |

| Automation cuts claims cycle time | Automated FNOL generation and repair scheduling reduce downtime and administrative errors. |

| Documentation builds negotiating power | Timestamped training and inspection records shift your fleet from standard to preferred risk status. |

| Daily workflow beats annual renewal | Continuous data sharing captures mid-term adjustments that waiting until renewal will miss. |

| Coverage tracking prevents gaps | Mapping each vehicle and cargo type to the correct policy endorsement protects against uncovered claims. |

Why I think most fleets are leaving serious money on the table

After working closely with transportation businesses and their insurance challenges, I have come to one clear conclusion: most small and mid-sized fleets treat insurance as an administrative obligation rather than an operational asset. That mindset is expensive.

The fleets that negotiate the best rates are not necessarily the safest. They are the ones that can prove they are safe, in formats that underwriters can process quickly. I have seen operations with genuinely strong safety cultures pay standard market rates simply because their documentation was scattered across paper files and email threads. Meanwhile, a competitor with a structured telematics export and a clean digital safety archive walks into renewal with leverage.

The organizational change piece is harder than the technology piece. Getting drivers to understand why their telematics data matters, and getting dispatchers to log incidents immediately rather than at end of shift, requires consistent internal communication. The fleets that succeed treat their insurance workflow owner the same way they treat their safety officer: as someone with real authority and a clear mandate.

My honest advice is to start with the audit. You cannot fix what you cannot see. Once you map your current process, the gaps become obvious, and the ROI of fixing them becomes easy to calculate. The tools exist. The savings are real. The only variable is whether you build the habit of treating your insurance workflow as a daily operational priority.

— Vladimir

How Diamondbackins supports your fleet insurance workflow

Managing a fleet insurance workflow is complex enough without spending hours on the phone chasing quotes from individual carriers. Diamondbackins is built to remove that friction. As an online platform that aggregates quotes from multiple top-rated insurers, Diamondbackins gives fleet managers and small business owners instant access to commercial truck insurance quotes tailored to their specific coverage needs, vehicle types, and operating regions.

Whether you operate in Georgia, Virginia, or across state lines, Diamondbackins connects you to coverage options that align with your fleet’s risk profile and workflow requirements. The platform is designed for speed and transparency, so you can compare options, select the right coverage, and secure your policy in minutes rather than days. If you are ready to put your fleet’s safety record to work, get your instant fleet quote through Diamondbackins today and see what your documented safety performance is actually worth.

FAQ

What is a fleet insurance workflow?

A fleet insurance workflow is the integrated system of processes that manages policy administration, claims handling, telematics data sharing, and safety documentation for a commercial vehicle fleet. It replaces manual, siloed tasks with connected digital processes that reduce costs and improve claims outcomes.

How much can an optimized workflow reduce fleet insurance premiums?

Integrated, data-driven fleet insurance workflows can reduce premiums by 15 to 35% within three to six months of sustained safety data sharing with insurers. Fleets with verified telematics records also see compounded reductions of 12 to 25% or more across multiple renewal cycles.

What telematics data do insurers actually use for underwriting?

Insurers use GPS trip data, hard braking events, ADAS sensor alerts, speeding incidents, and dash cam footage to assess actual fleet risk. Sharing this data in structured, insurer-accepted formats is what converts raw telematics into premium reductions.

How does automated claims reporting improve fleet operations?

Automated claims reporting generates First Notice of Loss packages within minutes of an incident using G-force and GPS event data. This accelerates insurer notification, speeds repair approvals, and reduces the administrative burden on fleet managers and drivers.

When should fleets share safety data with their insurer?

Fleets should share safety data on a monthly basis rather than waiting for annual renewal. Continuous data sharing allows insurers to make mid-term premium adjustments and keeps your fleet in preferred risk status throughout the policy term.