Comparing insurance quotes for a commercial fleet sounds straightforward until you’re staring at five different documents with mismatched coverage limits, varying deductibles, and fine print that seems designed to confuse. Most fleet managers and small trucking business owners spend hours on this process, only to end up second-guessing their final choice or, worse, discovering a coverage gap after an incident. Choosing the wrong policy can mean paying thousands more than necessary or being underinsured when it matters most. This guide walks you through every step of the comparison process, from understanding what you’re actually looking at to making a confident, informed decision.

Table of Contents

- Know what you’re comparing: Key components of fleet insurance quotes

- Step-by-step: How to request and organize insurance quotes

- What really drives costs? Advanced factors and industry trends in 2026

- Evaluate and decide: How to pick the right insurance quote for your fleet

- A fleet manager’s perspective: Why quote comparison is changing in 2026

- Get personalized, competitive fleet insurance quotes today

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Key quote components | Focus on coverages, limits, exclusions, and endorsements to compare quotes accurately. |

| Cost drivers | Cargo type, route radius, authority status, and market trends profoundly impact your rates. |

| Organize comparisons | Use a structured process and table to review fleet insurance quotes side by side. |

| Leverage discounts | Tech tools and safety programs can reduce premiums by up to 25%. |

| Expert decision-making | Balance price with quality of coverage to protect your business from costly mistakes. |

Know what you’re comparing: Key components of fleet insurance quotes

Before you can compare quotes accurately, you need to understand what each quote actually contains. A commercial fleet insurance quote is not a single number. It is a structured document that outlines multiple coverage types, each with its own limits, deductibles, and exclusions. Treating quotes as simple price tags is one of the most common and costly mistakes fleet operators make.

The four core coverage types you will see in nearly every commercial fleet quote are liability, physical damage, motor truck cargo, and general liability. Liability coverage protects you when your driver causes an accident that injures someone or damages property. Physical damage coverage includes collision and comprehensive protection for your own vehicles. Motor truck cargo insurance covers the freight you haul. Each of these can be adjusted independently, which is why two quotes with similar total premiums can look completely different once you examine the details.

Several factors directly shape what you pay. Your operating radius, the states where you run, the type of cargo you haul, the age and condition of your vehicles, and whether you hold your own operating authority all influence pricing. Fleet insurance premium ranges typically fall between $9,000 and $17,000 per year per truck, though state-by-state variation is significant. A fleet operating in Texas or Florida will often see higher rates than one based in the Midwest, largely due to litigation environments and traffic density.

Key terms you need to know before reviewing any quote include the deductible (the amount you pay out of pocket before coverage kicks in), endorsements (add-ons that expand or modify your base policy), exclusions (situations or cargo types the policy will not cover), and limits (the maximum payout per incident or policy period). When reviewing a quote document, focus on the declarations page first. It summarizes your coverage limits and premiums in one place. Then review the exclusions section carefully. That is where policies tend to differ most.

For specialized vehicles, the comparison process has additional layers. If you operate box truck insurance quotes for local delivery fleets, for example, your cargo and liability needs will differ from a long-haul operation. Always ask agents to clarify any coverage that seems vague or unusually broad.

Pro Tip: Request a copy of the full policy language, not just the summary sheet, before committing. The declarations page tells you the limits; the full policy tells you the conditions.

“The cheapest quote is rarely the best quote. A policy with a lower premium but higher deductibles and narrower exclusions can cost you far more after a single claim.”

Step-by-step: How to request and organize insurance quotes

With a clear understanding of what you are comparing, the next step is building a repeatable process for collecting and organizing multiple quotes efficiently. This is where many fleet managers lose time, either by approaching too few sources or by collecting quotes that are not truly comparable.

Start by identifying your sourcing channels. You have three main options: independent brokers who work with multiple carriers, direct carriers who sell their own policies, and online comparison platforms that aggregate quotes from several insurers at once. Each has advantages. Brokers offer personalized guidance. Direct carriers can sometimes offer loyalty discounts. Online platforms give you speed and breadth. Using at least two channels gives you a stronger baseline for comparison.

Before you request a single quote, gather the information you will need. Carriers will ask for your complete vehicle list with VINs and vehicle weights, driver records and license information for all operators, your cargo types and typical routes, your operating authority number (MC or DOT number), your current or most recent insurance history, and details about any safety programs you run. Having this ready cuts quote turnaround time significantly.

Be alert to red flags during the quoting process. If an agent is unwilling to provide a full policy document, pushes you to decide within 24 hours, or cannot clearly explain an exclusion, treat that as a warning sign. New authorities face higher rates and fewer carrier options, which makes it even more important to work with agents who are transparent about why pricing is what it is.

Organize your quotes in a simple side-by-side table. Track the following for each quote: carrier name, total annual premium, liability limit, physical damage deductible, cargo coverage limit, key exclusions, and payment options. This structure makes it easy to spot where one policy is stronger and where another cuts corners.

| Coverage element | Quote A | Quote B | Quote C |

|---|---|---|---|

| Annual premium | $12,400 | $11,800 | $13,100 |

| Liability limit | $1M | $750K | $1M |

| Physical damage deductible | $2,500 | $5,000 | $2,500 |

| Cargo limit | $100K | $75K | $100K |

| Key exclusions | None noted | Reefer breakdown | None noted |

Pro Tip: Request all quotes with the same liability limit so you are comparing equivalent coverage. A lower premium with a lower limit is not a better deal.

For local box truck insurance needs, turnaround on quotes can be as fast as same-day through online platforms. For larger or more complex fleets, allow three to five business days and follow up proactively if you have not heard back.

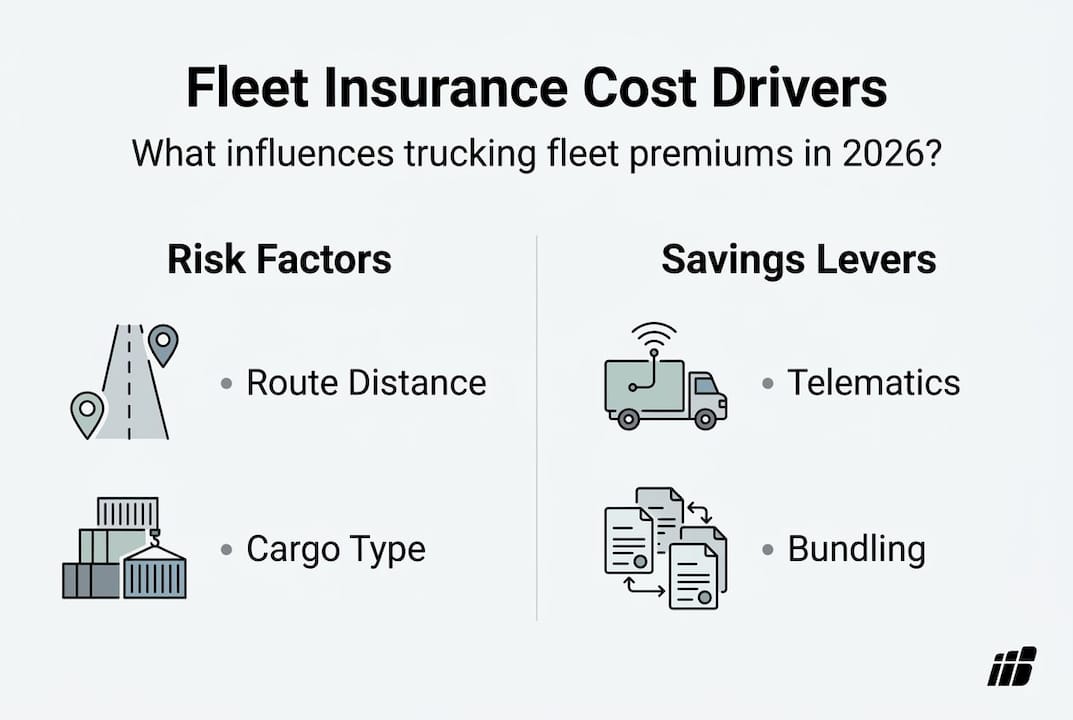

What really drives costs? Advanced factors and industry trends in 2026

Once your quotes are organized, the next question is why the numbers look the way they do. Understanding the deeper forces shaping fleet insurance costs in 2026 helps you negotiate more effectively and make smarter long-term decisions.

One of the most significant factors driving premiums higher across the industry is the rise of nuclear verdicts. A nuclear verdict is a jury award that far exceeds the actual damages in a case, often reaching tens of millions of dollars. These verdicts have become more common in trucking-related litigation, and carriers have responded by raising premiums across the board. Nuclear verdicts are driving up fleet insurance costs industry-wide, reshaping how carriers assess risk and price policies.

Edge cases also matter. If your fleet hauls HAZMAT (hazardous materials) or high-value loads, expect your premiums to be significantly higher than standard freight operations. HAZMAT loads can double your base premium in some markets due to the elevated liability exposure. Understanding this helps you evaluate whether a quote is priced appropriately for your specific cargo profile.

Technology is one of the most actionable levers you have. Fleets that install telematics systems and dashcams are consistently rewarded with lower rates. Telematics can earn discounts of 15 to 25 percent on premiums, and data shows that fleets using these tools report 18 percent fewer claims. Carriers view telematics as evidence of proactive risk management, which makes your fleet more attractive to underwriters.

Bundling policies is another effective strategy. Combining your commercial auto, cargo, and workers’ compensation coverage under one carrier often unlocks multi-policy discounts of 10 to 20 percent. Paying your annual premium upfront rather than monthly can also reduce your total cost. Safety programs, including driver training certifications and documented incident response procedures, are increasingly recognized by carriers as premium-reducing factors.

State-specific regulatory changes are also worth monitoring. Tort reform efforts in states like Florida and Georgia are shifting the litigation landscape, which may affect future pricing. Staying informed about workers’ compensation cost changes in your operating states helps you anticipate premium adjustments before renewal.

Evaluate and decide: How to pick the right insurance quote for your fleet

With your quotes organized and cost drivers understood, you are ready to make a final decision. This stage is about applying a structured framework so you choose confidently rather than reactively.

Start with a checklist of critical questions before committing to any policy. Does the liability limit meet federal and state minimums for your cargo type and routes? Are your highest-value vehicles covered under physical damage with a deductible you can realistically absorb? Are there any exclusions that could leave you exposed given your specific operations? Is the carrier rated A or better by AM Best, which is the industry standard for financial stability? Can you reach claims support 24 hours a day, seven days a week?

Balancing cost, coverage, and service is the central challenge. A policy that saves you $1,200 per year but comes with a $10,000 deductible may not serve you well if your fleet experiences even one minor incident. Conversely, paying for maximum limits on cargo types you rarely haul is unnecessary spending. The goal is alignment between your actual risk profile and your coverage structure.

Signs of a strong insurer for trucking fleets include a dedicated commercial lines team, experience with your specific cargo or vehicle type, transparent claims handling procedures, and a willingness to customize endorsements. Bundling policies and safety programs can improve your rates over time, so look for carriers who reward long-term relationships rather than just offering a low first-year rate.

When you are ready to push for better terms, ask specifically about safety credits, telematics discounts, and custom endorsements for your most common risk scenarios. Use your organized comparison table as leverage. Carriers want your business, and showing that you have done your research positions you as a serious, low-risk client.

Use an insurance cost calculator to pressure-test your final choice against industry benchmarks before signing. Once you confirm your selection, review the policy documents one final time, confirm your effective date, and store your certificate of insurance in an accessible location for compliance purposes.

Pro Tip: Set a calendar reminder 90 days before your renewal date. Starting the comparison process early gives you negotiating power and prevents rushed decisions.

A fleet manager’s perspective: Why quote comparison is changing in 2026

Here is something most guides will not tell you: comparing quotes purely on price is a strategy that made sense a decade ago but is increasingly risky today. The trucking insurance market in 2026 is being shaped by forces that have nothing to do with your driving record or claims history.

Nuclear verdicts with a median of $36 million and telematics data showing 18 percent fewer claims for tech-equipped fleets tell a clear story. The insurers pricing your fleet most competitively are the ones who see you as a low-risk, well-managed operation. That perception is built over time through documented safety practices, technology adoption, and consistent communication with your carrier.

The smartest fleet managers we see are not just shopping for the lowest quote. They are actively building a risk profile that makes them attractive to top-tier carriers. They invest in dashcams, maintain clean driver records, and ask the right questions during the quoting process. That approach consistently delivers better coverage at better rates, year after year. Price comparison is a starting point, not the finish line.

Get personalized, competitive fleet insurance quotes today

If this guide has shown you anything, it is that getting the right fleet insurance quote requires more than a quick search. It requires the right tools, the right information, and a platform that understands the trucking industry.

At Diamondback Insurance, we specialize in commercial vehicle and trucking coverage for fleet managers and small business owners just like you. Our platform aggregates online insurance quotes from multiple top-rated carriers instantly, so you can compare real options side by side without the back-and-forth. Whether you need coverage for a single box truck or a growing fleet, we make it fast, transparent, and straightforward. We also offer workers’ compensation solutions to help you protect your full operation. Get your personalized quote today and see how much you could save.

Frequently asked questions

What documents do I need to compare commercial fleet insurance quotes?

You typically need your vehicle list, driver information, operating authority, cargo details, recent insurance history, and documentation of any safety programs. Factors affecting costs and application requirements vary by carrier, so having everything organized upfront speeds up the process.

Can I get fleet insurance if I have a new operating authority?

Yes, but expect higher premiums and fewer carrier choices until you build a track record. New authorities face higher rates because carriers have limited data to assess your risk profile.

How do telematics and dashcams affect my fleet’s insurance rates?

Telematics and dashcams can lower your premiums by 15 to 25 percent and reduce claims by over 18 percent, making your fleet more attractive to carriers.

What causes insurance quotes to increase significantly year over year?

Major factors include nuclear verdicts, HAZMAT loads, and changes in state regulations or claim histories. Nuclear verdicts have raised premiums by 36 percent industry-wide, making proactive risk management more important than ever.

Recommended

- Q&A Blog Post: Box Truck Insurance Quotes

- Q&A Blog Post: Box Truck Insurance Near Me

- Simplifying Your Boat Insurance Estimate with DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- Navigating the Seas with Confidence: Marine Insurance for Your Cargo – Diamondback Insurance – Solutions with Instant Online Quotes