Most small business owners assume their personal auto insurance has them covered when they drive for work. That assumption is wrong, and it can cost you everything. A business auto policy (BAP) provides liability and physical damage coverage specifically for vehicles used in business operations, including owned, leased, hired, or non-owned employee vehicles. If your company relies on any vehicle to generate revenue, transport goods, or serve customers, understanding a BAP is not optional. This guide walks you through exactly what it covers, how it differs from personal insurance, and how to make sure your business is fully protected.

Table of Contents

- What is a business auto policy?

- Key components and coverage options

- Business auto vs. personal auto policies: What’s the difference?

- Common exclusions and endorsement pitfalls

- A fresh perspective: Why your BAP is just the starting point

- Protect your fleet with the right business auto policy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| BAP is essential | Personal auto insurance usually won’t cover claims for business use—BAP is designed to protect your business on the road. |

| Comprehensive coverages | A business auto policy offers liability, physical damage, and endorsements that can be tailored to your needs. |

| Mind the exclusions | Common exclusions include cargo, employee injuries, and some personal use—endorsements or extra policies are often needed. |

| Different from personal policies | BAPs offer higher limits and broader protections covering employees, contractors, and special vehicles compared to personal policies. |

| Regular policy review | Businesses should review fleet insurance annually to avoid coverage gaps and adapt to new risk exposures. |

What is a business auto policy?

A business auto policy is a specialized commercial insurance contract designed to protect your company when vehicles are used for work purposes. It is not simply a personal auto policy with a higher price tag. The BAP is a distinct product built for the exposures that come with operating vehicles in a business context, and it addresses risks that personal policies are never designed to handle.

According to standard insurance definitions, a BAP covers business vehicles ranging from private passenger cars driven by employees on sales calls, to delivery vans, to larger commercial trucks. The policy applies to vehicles your company owns outright, vehicles you lease, vehicles you hire for short-term use, and even personal vehicles your employees use for business errands. That last category is particularly important for small businesses that do not maintain a dedicated fleet.

Understanding trucking insurance basics reveals that the distinction between personal and commercial coverage matters the moment a claim is filed. Personal auto insurers routinely investigate whether a vehicle was being used for business at the time of an accident. If it was, they can deny the claim entirely. A BAP eliminates that risk by covering business use as its core purpose.

The practical scenarios requiring a BAP are broader than most owners expect. A landscaping crew driving a pickup to a job site needs one. A catering company using a cargo van needs one. A real estate agent regularly driving clients to property showings may need one. Even a freelance consultant who frequently drives a personal vehicle for client meetings may benefit from a BAP or a hired and non-owned auto endorsement. You can also explore commercial moving insurance options to understand how similar principles apply across transportation-related businesses.

Pro Tip: If any employee, including yourself, ever drives a vehicle for a work purpose and gets into an accident, your personal policy could deny that claim. The only reliable way to close that gap is through a properly structured business auto policy.

Key components and coverage options

Now that we know what a BAP is, let’s break down exactly what it includes and how each part protects your business.

The standard BAP form, such as the ISO CA 00 01, consists of five main sections: covered autos (defined by symbol codes), liability coverage, physical damage coverage, business auto conditions, and definitions. Each section has a specific function, and together they create the framework for your entire commercial vehicle protection.

Symbol codes are one of the most technical aspects of a BAP, and they are also one of the most consequential. These are numerical designations (ranging from 1 through 9, plus 19 and others) that appear on your declarations page and define exactly which vehicles your policy covers. Symbol 1, for example, means “any auto,” which is the broadest possible coverage. Symbol 7 limits coverage to specifically described vehicles only. Choosing the wrong symbol can leave vehicles unprotected without you ever realizing it. Always confirm with your insurer that the symbols assigned to your policy match the actual vehicles and usage patterns in your operation.

The core coverages within a BAP include liability for bodily injury and property damage caused to others, collision coverage for damage your vehicle sustains in an accident, comprehensive coverage for non-collision events like theft, fire, or weather damage, medical payments or personal injury protection (PIP) for occupants of your vehicle, uninsured and underinsured motorist coverage, and the hired and non-owned auto (HNOA) endorsement for vehicles your business uses but does not own.

Understanding liability coverage types is essential here because commercial liability limits are significantly higher than personal limits. A standard commercial liability limit often starts at $1 million combined single limit. For trucking operations or businesses transporting goods across state lines, federal minimums may require even higher limits depending on the cargo classification.

Endorsements allow you to customize your BAP beyond its standard form. Common add-ons include drive other car coverage (which extends protection to executives driving non-business vehicles), employees as insureds, and coverage for mobile equipment attached to vehicles. Reviewing insurance types for trucking businesses provides a helpful look at how these endorsements stack up for transportation-heavy operations. You might also want to review freight insurance options if your business involves transporting third-party goods regularly.

| Coverage type | What it protects | Typical limit range |

|---|---|---|

| Liability (BI/PD) | Injury or damage to others | $500K to $2M+ |

| Collision | Your vehicle in an accident | Actual cash value |

| Comprehensive | Theft, fire, weather damage | Actual cash value |

| Medical payments/PIP | Occupant medical costs | $5K to $50K |

| Uninsured motorist | Accidents with uninsured drivers | Matches liability limit |

| HNOA endorsement | Non-owned/hired vehicles | Varies by policy |

Pro Tip: Request a copy of your declarations page and verify the symbol codes listed for each vehicle. If your insurer assigned Symbol 7 but you occasionally rent trucks or let employees use personal vehicles for deliveries, you likely have a gap that needs an immediate endorsement update.

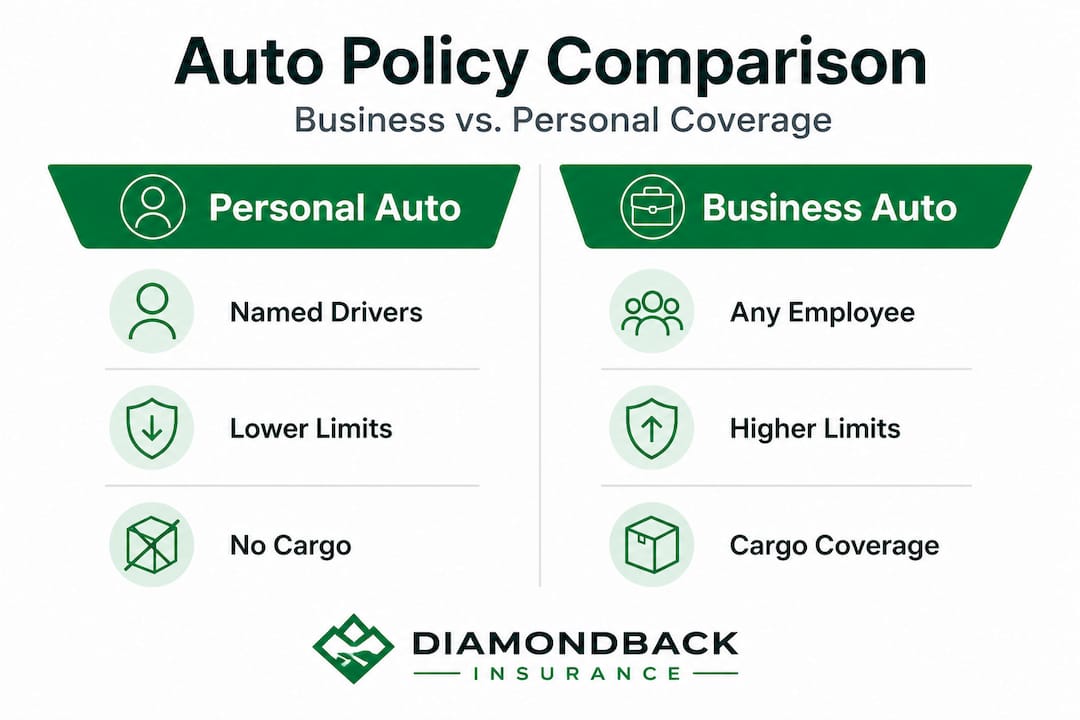

Business auto vs. personal auto policies: What’s the difference?

Understanding the specifics of BAP coverage, let’s see how it stacks up directly against a standard personal auto policy.

The differences are significant and the consequences of choosing wrong are serious. Personal auto insurance is designed for individual drivers using their vehicles for personal travel. It typically carries lower liability limits (often $100,000 to $300,000), covers a limited number of drivers listed on the policy, and explicitly excludes commercial use. A BAP carries higher limits (often $1 million or more), covers employees and permissive drivers, and addresses business exposures like cargo and tools.

Using a personal policy for commercial activity is not just a coverage gap. It is a financial risk that can result in total claim denial at the exact moment you need protection most.

The coverage gap becomes painfully real in specific loss scenarios. Imagine one of your employees rear-ends another vehicle while making a delivery. The injured party sues for $800,000. Your personal auto policy, with a $300,000 limit, would deny the claim anyway because business use was involved. Now you face that lawsuit with no insurance support and full personal liability. A BAP with a $1 million liability limit would respond to that claim and protect your business assets.

Businesses with larger fleets face compounded exposure. The more vehicles you operate, the greater the statistical likelihood of an accident occurring during business hours. A single fleet without proper BAP coverage could face simultaneous claims from multiple incidents with zero protection.

Another critical difference involves who is covered behind the wheel. Personal policies name specific individuals. A BAP can cover any employee or authorized driver operating a covered vehicle, which is essential when multiple staff members share company trucks or vans. Understanding your insurance options for truckers and commercial operators means recognizing that driver coverage flexibility is a core feature of commercial policies.

You should also consider how cargo coverage applies. Personal policies do not cover goods being transported for commercial purposes. If your employee is hauling $50,000 in equipment for a client and an accident destroys it, your personal policy offers nothing. Basic cargo insurance is a separate product, but the BAP with proper endorsements can address part of that exposure.

| Feature | Personal auto policy | Business auto policy |

|---|---|---|

| Liability limits | $100K to $300K typical | $500K to $2M+ typical |

| Business use coverage | Excluded | Core purpose |

| Driver eligibility | Named individuals | Employees, permissive drivers |

| Cargo protection | None | Available via endorsement |

| Number of vehicles | Typically 1 to 4 | Unlimited fleet support |

| Claims during work hours | Often denied | Covered |

Common exclusions and endorsement pitfalls

Even robust BAPs have limitations. Here is what you need to watch for and how to plug the most common coverage gaps.

Standard BAPs contain several important exclusions that surprise business owners when claims arise. Punitive damages are excluded in many states, meaning if a jury awards punitive damages against your driver for reckless behavior, your policy does not pay that portion. Intentional acts are never covered. Employee injuries sustained while operating your vehicles fall outside the BAP entirely and require a separate workers’ compensation policy.

Cargo is another major exclusion. A BAP protects the vehicle itself, but the goods inside it are not automatically covered. If your fleet transports freight, equipment, or client property, you need a separate inland marine policy to cover the cargo. This distinction catches many business owners completely off guard during their first major claim. You can review cargo insurance coverage options to understand what a proper cargo policy should include.

Vehicles over 10,000 pounds gross vehicle weight rating (GVWR) may require separate filings or specialized policies beyond a standard BAP. This threshold matters enormously for businesses using heavy-duty trucks, tow trucks, or large commercial vans. Failing to account for it means your heaviest, most valuable vehicles may operate without valid coverage.

Personal use of business vehicles creates another tricky gap. If an executive takes a company car home on weekends and gets into an accident on Saturday morning, the BAP may not respond because it was not being used for business. The Drive Other Car (DOC) endorsement solves this problem by extending protection to covered individuals driving non-owned vehicles for personal use. It is a relatively inexpensive endorsement that prevents significant exposure.

Reviewing your insurance needs for trucking or any commercial operation should happen at least annually. Your business changes, your fleet changes, your driver roster changes, and your exposures change with them. An endorsement that was sufficient two years ago may leave you unprotected today.

Pro Tip: Schedule a formal annual policy review with your insurance advisor before each renewal. Bring your current vehicle list, driver roster, and any changes to your operations. A 30-minute review can identify gaps that would otherwise cost you six figures in uninsured losses.

A fresh perspective: Why your BAP is just the starting point

With exclusions and complex risks in mind, let’s rethink what it really means to be protected on the road.

Most business owners treat their BAP like a checkbox. They get the policy, file it away, and assume they are protected until something goes wrong. That mindset is genuinely dangerous, and it is one we see reflected in claims situations every single year.

Here is the uncomfortable truth. A standard BAP, even a well-structured one, is a foundation. It is not a complete risk management strategy. Modern businesses operate with exposures that evolve constantly: new drivers, new vehicle types, new cargo categories, new operating territories, and new regulatory requirements. Your policy needs to evolve with your business, or it silently becomes inadequate.

The businesses that handle claims well are not the ones that bought the cheapest policy. They are the ones that understood their exposures, built their coverage intentionally, and revisited it regularly. They worked closely with their advisors, asked hard questions about exclusions, and made deliberate decisions about every endorsement. That is proactive risk management, and it is what separates businesses that survive a major accident from those that do not.

We also see a pattern among small fleet operators who underestimate the impact of truck insurance cost factors. Premiums that feel high on the front end represent a fraction of what a single uninsured liability claim can cost. The real cost of inadequate coverage is not the premium you saved. It is the lawsuit settlement, the cargo replacement, and the regulatory fine that follows when your coverage falls short.

Your BAP is the right starting point. But staying protected means treating it as a living document, one you actively manage rather than passively hold.

Protect your fleet with the right business auto policy

If you’re ready to take practical action and protect your fleet, here is how Diamondback Insurance can help.

Choosing the right business auto policy means more than picking the lowest premium. It means finding coverage that matches your actual operations, closes every gap, and grows with your business. Diamondback Insurance makes that process faster and more transparent than the traditional route.

Through our platform, you can save on fleet insurance costs by comparing quotes from multiple top-rated commercial insurers side by side in minutes. No back-and-forth with brokers, no paperwork delays, no guesswork on coverage terms. You enter your fleet details, your usage information, and your coverage needs, and we return real quotes you can actually compare. From there, you can get trucking insurance quotes and purchase the right policy directly online, with expert support available at every step. Your vehicles are on the road every day. Your protection should be that reliable too.

Frequently asked questions

Does a business auto policy cover all vehicle types used by my company?

A standard BAP covers a wide range of vehicles including owned, leased, hired, and non-owned employee vehicles, but heavy vehicles over 10,000 pounds GVWR or specialized equipment may require separate endorsements or dedicated policies.

What is not covered by a business auto policy?

A BAP excludes employee injuries, punitive damages in most states, intentional acts, cargo (unless specifically endorsed), and personal vehicle use; workers’ comp, inland marine, and endorsements like Drive Other Car can fill many of those gaps.

Can I use my personal auto policy for my business vehicle?

No. Personal auto insurance excludes business use and insurers can deny claims when vehicles are operated commercially, leaving your business fully exposed to liability without a dedicated commercial policy.

What are the most important coverages in a BAP?

The essential coverages are liability (bodily injury and property damage), collision and comprehensive, medical payments, uninsured and underinsured motorist protection, and the hired and non-owned auto (HNOA) endorsement for vehicles your business uses but does not own.

How do I get a quote or start a business auto policy?

Work with a commercial insurance specialist, provide details about your fleet, driver roster, and business operations, and request an instant online quote to get accurate pricing tailored to your specific coverage needs.