An insurance deductible is the fixed dollar amount you pay out of pocket before your insurer covers the remaining cost of a covered claim. Understanding the role of insurance deductibles is one of the most practical financial decisions you can make as a homeowner or policyholder, because this single number shapes both your monthly premium and your exposure when something goes wrong. In 2026, ACA individual out-of-pocket maximums are capped at $9,200 annually, and homeowners deductibles commonly range from $500 to $5,000 flat. Getting this choice right protects your budget on both ends.

How do insurance deductibles impact your premiums and claims?

The relationship between deductibles and premiums is direct and mathematical. Deductibles filter out trivial claims, reduce insurer administrative costs, and allow carriers to price policies at lower monthly rates. When you absorb more of the initial risk, the insurer’s exposure shrinks, and that savings gets passed to you as a reduced premium.

The insurance deductible impact on claims is equally significant. A higher deductible means you pay more out of pocket before your insurer steps in, which discourages filing small claims that barely exceed the threshold. Filing a $600 claim on a $500 deductible homeowners policy, for example, nets you only $100 from your insurer while potentially triggering a premium increase at renewal. That math rarely works in your favor.

From a budget planning perspective, your deductible choice sets the floor of your financial exposure in any covered event. A $2,500 deductible on a homeowners policy might save you $300 to $500 per year in premiums, but it also means you need $2,500 accessible if a storm damages your roof. The strategic risk management required here is not complicated, but it demands honesty about your actual cash reserves.

Pro Tip: Calculate how many years of premium savings it takes to offset one deductible payment. If a higher deductible saves you $400 per year but costs you $2,000 more per claim, you need five claim-free years just to break even. Run that number before you commit.

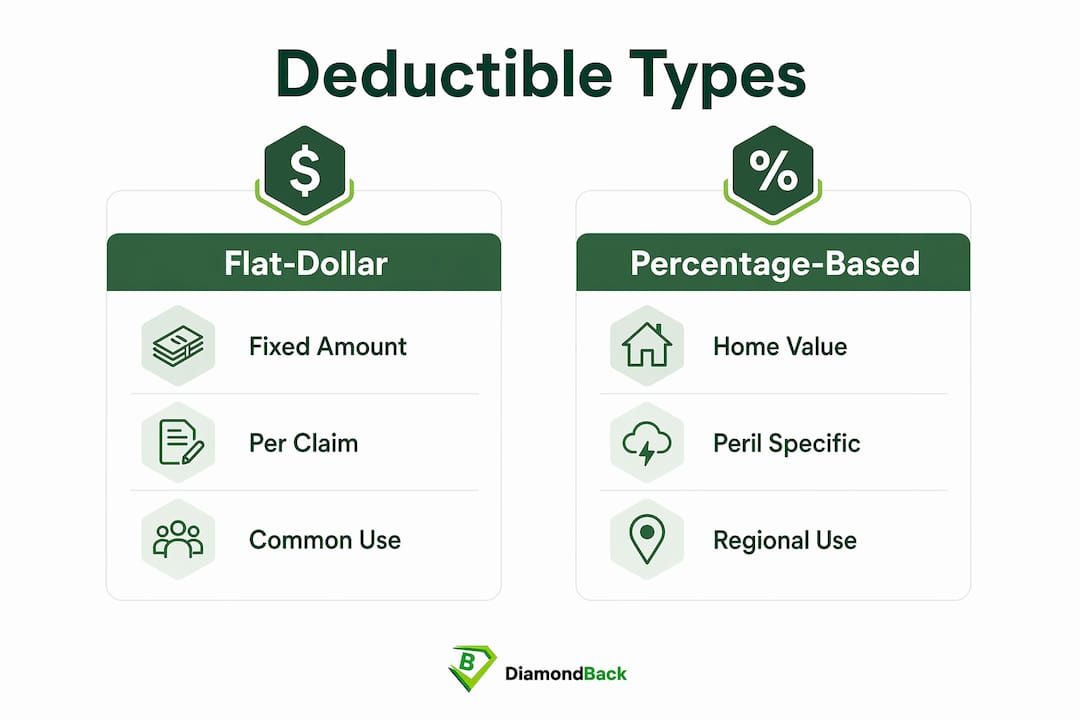

What are the different types of deductibles and how do they work?

Not all deductibles operate the same way, and the type embedded in your policy determines exactly how much you pay when a loss occurs.

Flat-dollar deductibles are the most common structure. You pay a fixed amount, say $1,000, regardless of the total claim size. A $15,000 roof replacement with a $1,000 deductible means your insurer pays $14,000. Homeowners insurance deductibles typically range from $500 to $5,000 flat, giving policyholders a predictable out-of-pocket figure.

Percentage-based deductibles are calculated as a percentage of your home’s insured value, not the claim amount. If your home is insured for $400,000 and your deductible is 2%, you owe $8,000 before coverage applies. This structure is standard in coastal states for hurricane and wind damage, and it can produce unexpectedly large out-of-pocket costs during major weather events.

Per-occurrence vs. annual deductibles represent the other key structural difference. Auto and homeowners policies use per-occurrence deductibles, meaning you pay the deductible each time you file a separate claim. Health insurance uses an annual aggregate deductible. Individual high-deductible health plans carry a minimum threshold of $1,600 in 2026, and once you meet that annual amount through accumulated medical expenses, your insurer covers the rest for the remainder of the year.

| Deductible type | How it works | Typical insurance context |

|---|---|---|

| Flat-dollar | Fixed amount per claim, e.g., $1,000 | Homeowners, auto, renters |

| Percentage-based | Percentage of insured value, e.g., 2% of $400,000 | Homeowners hurricane/wind riders |

| Per-occurrence | Applies separately to each individual claim | Auto, homeowners |

| Annual aggregate | Accumulates across all claims within one policy year | Health insurance |

Understanding which type applies to your policy prevents surprises at claim time. A homeowner in Florida with a 5% wind deductible on a $350,000 home faces a $17,500 out-of-pocket cost before any hurricane coverage kicks in. That figure demands a very different savings strategy than a standard $1,000 flat deductible.

Why does choosing the right deductible matter?

Selecting a deductible is not simply about finding the lowest premium. It is a risk management and financial planning decision that reflects how much loss you can absorb without disrupting your household finances.

The most common mistake policyholders make is choosing the highest deductible available to minimize monthly premiums, without verifying they could actually pay that amount in an emergency. A $5,000 deductible on a homeowners policy is only a good choice if you have $5,000 liquid and accessible. If a pipe bursts in January and you have $800 in savings, that premium discount becomes a financial crisis. Choosing the right deductible depends on your ability to absorb out-of-pocket risk without financial strain, not just on the premium savings it generates.

Your claim history also matters. If you have filed multiple claims in recent years, a lower deductible may serve you better even at a higher premium cost. Frequent claimants face a compounding problem: each claim raises premiums, and a high deductible on top of elevated rates can leave you paying more on both sides. Reviewing your commercial vehicle insurance renewal history annually gives you a clear picture of whether your current deductible structure is working.

The concept of self-insurance is worth understanding here. When you choose a high deductible, you are effectively self-insuring the first layer of any loss. The excess ratio concept used by commercial insurers makes this explicit: the higher the deductible, the greater the share of losses you retain before the insurer’s coverage begins. This is not inherently bad. It is simply a deliberate trade-off that requires a funded emergency reserve to execute responsibly.

Pro Tip: Set your deductible at the maximum amount you could pay within 30 days from existing savings, not from a credit card or future income. That constraint gives you a realistic ceiling and prevents the deductible from becoming a debt trigger.

How are deductibles applied during insurance claims?

When a covered loss occurs, the deductible application follows a consistent sequence regardless of insurance type.

- Loss occurs. You report the claim to your insurer and document the damage or expense.

- Claim is assessed. Your insurer or an adjuster determines the total covered loss amount.

- Deductible is subtracted. Your deductible amount is deducted from the total payout.

- Net payment is issued. For property and auto claims, deductible payments often go directly to the repair shop or contractor, with the insurer paying the remaining balance to the vendor.

- Health claims accumulate. For health insurance, each covered expense counts toward your annual deductible until the threshold is met, after which cost-sharing shifts to copays or coinsurance.

The payment flow in property and auto claims surprises many policyholders. You do not write a check to your insurer. Instead, when your car goes to a body shop for $4,000 in repairs and your deductible is $500, you pay the shop $500 and your insurer pays the shop $3,500. The insurer never touches your deductible payment directly.

Health insurance operates differently. Each medical bill you receive before meeting your deductible is paid entirely by you, at the insurer’s negotiated rate. Once your cumulative payments reach the deductible threshold, your plan begins sharing costs through coinsurance or copays until you hit the out-of-pocket maximum.

| Claim scenario | Total loss | Deductible | Insurer pays | You pay |

|---|---|---|---|---|

| Homeowners roof damage | $12,000 | $1,500 flat | $10,500 | $1,500 |

| Auto collision repair | $4,000 | $500 flat | $3,500 | $500 |

| Hurricane damage (2% deductible, $300K home) | $25,000 | $6,000 | $19,000 | $6,000 |

| Health: surgery before deductible met | $8,000 | $1,600 HDHP | $6,400 (after deductible) | $1,600 |

Understanding the claims process in advance removes the stress of figuring it out during an already difficult situation.

What are the consequences of deductible choices for homeowners and health insurance holders?

Deductible decisions carry consequences that extend well beyond the initial premium calculation, and some of those consequences only become visible after a claim.

For homeowners, filing small claims that barely exceed the deductible is one of the most reliable ways to trigger a premium increase or even a non-renewal notice. Insurers track claim frequency, not just claim size. Two $1,200 claims in three years on a $1,000 deductible policy signals risk behavior to underwriters, even though each individual claim was modest. Self-paying losses below or near your deductible threshold is often the smarter long-term strategy.

Catastrophic perils like hurricanes introduce a separate layer of complexity through percentage-based deductibles. Homeowners in coastal states often carry standard flat deductibles for most perils but face 1% to 10% percentage deductibles specifically for wind or hurricane damage. On a $500,000 home, a 3% hurricane deductible means $15,000 out of pocket before coverage applies. Many homeowners discover this figure only when filing a claim after a major storm.

For health insurance holders, the 2026 ACA individual out-of-pocket maximum of $9,200 sets a ceiling on annual exposure, but the path to that ceiling matters. High-deductible health plans paired with Health Savings Accounts (HSAs) allow you to set aside pre-tax dollars specifically to cover deductible costs, making the financial exposure more manageable. Choosing a high-deductible health plan without funding an HSA removes the primary financial benefit of that structure.

The practical guidance here is straightforward. Review your deductible levels annually, keep a dedicated reserve equal to your highest deductible, and treat your insurance policy as a tool for catastrophic protection rather than routine expense reimbursement.

Key takeaways

The role of insurance deductibles is to create a cost-sharing structure that lowers premiums, filters out minor claims, and requires policyholders to fund a liquid reserve equal to their chosen deductible amount.

| Point | Details |

|---|---|

| Deductibles lower premiums | Higher deductibles reduce insurer exposure, directly lowering your monthly premium cost. |

| Type determines exposure | Flat-dollar deductibles are predictable; percentage deductibles can produce large unexpected costs in catastrophic events. |

| Claims filing strategy matters | Filing small claims near your deductible threshold often triggers premium increases that outweigh the payout. |

| Liquidity is the real constraint | Your deductible ceiling should match the cash you can access within 30 days, not your theoretical savings target. |

| Annual review is non-negotiable | Deductible suitability changes as your income, savings, and claim history evolve each policy year. |

What I’ve learned about deductibles after years in the insurance space

Most people treat deductible selection as a one-time decision made at policy inception and never revisited. That is the single most costly mistake I see repeated across homeowners and health insurance holders alike.

The premium savings from a high deductible are real, but they are gradual. The financial exposure from a high deductible is immediate and concentrated. When a loss happens, you need that money now, not spread across three years of premium savings. I have seen homeowners delay roof repairs because they could not cover a $3,500 deductible, even though they had been saving $400 per year by choosing that amount. The math looked good on paper and failed completely in practice.

The other overlooked factor is claim history’s compounding effect on premiums. Filing two or three small claims in a short window can raise your annual premium by more than the total claims paid. Self-paying losses below $2,000 and reserving your coverage for genuine catastrophic events is a discipline that pays off over a five to ten year horizon. Treat your policy as protection against financial ruin, not as a reimbursement account for routine repairs.

Review your deductible every renewal cycle. As your savings grow, a higher deductible becomes more defensible. As your financial situation tightens, moving to a lower deductible is worth the premium increase. The right deductible is not a fixed answer. It is a number that should track your actual financial capacity year by year.

— Vladimir

Find the right coverage structure with Diamondbackins

Deductible strategy is only one part of building a policy that actually protects you. Diamondbackins specializes in helping fleet operators, trucking professionals, and commercial vehicle owners find coverage structures that balance premium costs with realistic deductible levels. The platform aggregates quotes from multiple top-rated insurers, so you can compare deductible options and premium trade-offs side by side in minutes. If you operate commercial vehicles or manage a fleet, explore commercial trucking insurance options built around your specific risk profile. You can also review cargo insurance protections to understand how deductibles apply across different coverage lines within a single fleet policy.

FAQ

What is the role of insurance deductibles?

An insurance deductible is the amount you pay out of pocket before your insurer covers a claim. Its primary role is to share risk between you and the insurer, which lowers premiums and reduces minor claim filings.

Do higher deductibles always mean lower premiums?

Higher deductibles reduce the insurer’s financial exposure, which directly lowers your premium. The trade-off is greater out-of-pocket cost when a claim occurs, so the savings only benefit you if you have sufficient liquid reserves.

How does a percentage deductible differ from a flat deductible?

A flat deductible is a fixed dollar amount regardless of claim size, while a percentage deductible is calculated as a percentage of your home’s insured value. Percentage deductibles for hurricanes can reach 1% to 10% of insured value, producing far larger out-of-pocket costs than a standard flat deductible.

Should I file a claim if the loss is close to my deductible?

Filing a claim just above your deductible is rarely worth it. Frequent small claims often trigger premium increases or non-renewal, making self-payment the smarter financial choice for losses near your deductible threshold.

What is the 2026 ACA out-of-pocket maximum for individuals?

The ACA individual out-of-pocket maximum in 2026 is $9,200, which includes deductibles, copays, and coinsurance. Once you reach this limit, your insurer covers 100% of covered in-network expenses for the remainder of the year.

Recommended

- Fleet Manager Insurance Guide: Protect Your Fleet in 2026

- Navigating Workers’ Comp Insurance for the Self-Employed: A DiamondBack Insurance Guide – Diamondback Insurance – Solutions with Instant Online Quotes

- Online insurance platforms: Save up to 25% on fleet costs

- Required Documents for Insurance Claim: 2026 Guide