First-party insurance is coverage that pays you, the policyholder, directly for your own losses. It does not compensate someone else who was harmed. When your commercial truck is damaged in a collision, when fire destroys your warehouse, or when a cyberattack locks your business systems, first-party insurance is what steps in to cover your costs. The term “first-party” refers to the contractual relationship: you are the first party, your insurer is the second party, and anyone outside that contract is a third party. Understanding this distinction shapes every coverage decision you make as an individual or business owner.

What is first-party insurance and how does it work?

First-party insurance pays you directly for covered losses such as property damage, vehicle repairs, or medical costs. The insurer’s obligation runs to you, not to someone else who may have been affected by an incident. This is the foundational first-party insurance definition that separates it from liability-based coverage.

How first-party insurance works is straightforward in principle. You purchase a policy that lists specific covered perils. When one of those perils causes a loss, you file a claim with your own insurer. First-party claims require no proof of fault from another party. You only need to demonstrate that a covered event occurred and that your loss falls within policy terms. This makes the process more direct than pursuing a third-party claim.

Common perils covered under first-party policies include fire, theft, windstorm, collision, vandalism, cyber incidents, and certain medical expenses. Business interruption coverage, which compensates for lost revenue when operations halt due to a covered event, also falls under the first-party category. Personal Injury Protection, known as PIP, is another example. PIP pays your medical bills after an auto accident regardless of who caused the crash.

The major types of first-party insurance include property insurance, auto collision and comprehensive coverage, health insurance, cyber insurance, and business interruption insurance. Each policy specifies covered perils, coverage limits, and deductibles. Your payout will not exceed the policy limit, and your deductible reduces the net amount you receive.

Pro Tip: Document the cause of every loss thoroughly before filing. Photograph damage, preserve records of the incident, and confirm that the event matches a covered peril in your policy. Insurers assess first-party claims based on causation and policy compliance, so clear documentation speeds resolution significantly.

First-party vs third-party insurance: what is the difference?

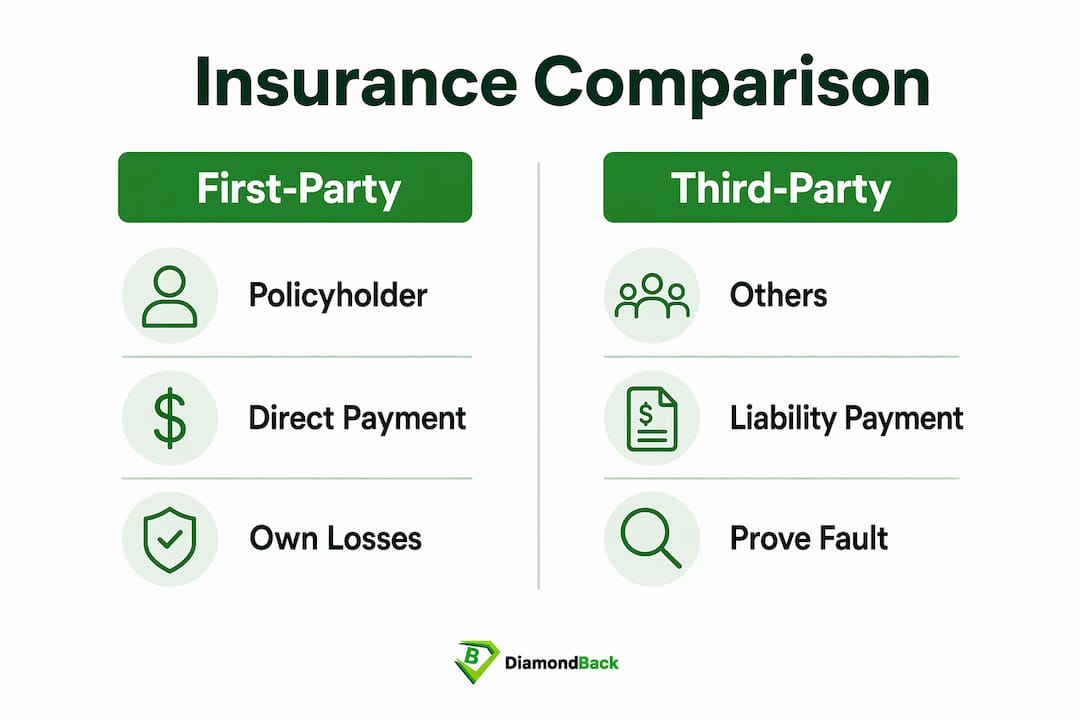

The core difference between first-party and third-party insurance is who gets paid and who you file the claim against. Third-party insurance pays others harmed by your negligence. First-party insurance pays you for your own losses. One event can trigger both types of claims simultaneously, with separate adjusters and separate evidence requirements.

Consider a trucking accident where your vehicle is damaged and another driver is injured. Your collision coverage, a first-party policy, pays to repair your truck. Your liability coverage, a third-party policy, pays the injured driver’s medical bills and property damage. The event is the same, but the claim relationships are entirely different.

Third-party claims require proving fault. The injured party or their insurer must establish that you were negligent before any payment is made. That process involves investigations, legal disputes, and often extended timelines. First-party claims resolve faster because your insurer already holds your policy details and owes you a direct contractual duty, including good faith handling and prompt payment.

The table below summarizes the key distinctions:

| Feature | First-party insurance | Third-party insurance |

|---|---|---|

| Who is compensated | You, the policyholder | A third party harmed by you |

| Who you file with | Your own insurer | The at-fault party’s insurer |

| Fault required | No | Yes |

| Payment speed | Typically faster | Often slower due to fault investigations |

| Common examples | Collision, property, cyber, health | Auto liability, general liability |

| Deductible applies | Yes | No (paid by at-fault party’s insurer) |

One nuance worth understanding: filing a first-party claim may affect your premiums at renewal, since your insurer absorbs the cost. Third-party claims filed against someone else’s policy generally do not affect your own premium. This is a practical consideration when deciding which route to pursue after an incident where both options are available.

Pro Tip: After an accident involving another driver, assess whether to file with your own insurer first or pursue the at-fault driver’s insurer. If fault is clear and the other driver is insured, a third-party claim avoids a deductible and protects your premium. If fault is disputed or the other driver is uninsured, your first-party coverage is the faster, more reliable path.

Real-world examples of first-party insurance claims

Seeing how first-party insurance applies in practice removes any remaining ambiguity about when and how to use it. The scenarios below cover both personal and commercial situations.

Personal examples are the most familiar. A homeowner whose roof collapses under heavy snow files a first-party claim under their homeowners policy. An auto policyholder whose car is stolen files a comprehensive coverage claim with their own insurer. A driver injured in a crash files a PIP claim for medical expenses, regardless of who caused the accident. In each case, the claim is filed with your own insurer for your own losses.

Commercial examples are where first-party insurance becomes especially critical. A trucking company whose warehouse catches fire files a commercial property claim to cover structural damage and lost inventory. A logistics firm hit by a ransomware attack files a cyber insurance claim to cover recovery costs, ransom payments, and business interruption losses. A fleet operator whose equipment is stolen from a job site files a first-party inland marine claim. Businesses rely on first-party coverage as the primary recovery method for direct damages, with third-party claims pursued separately when external negligence is involved.

Here is a breakdown of typical first-party claims by category:

Personal first-party claims:

Fire or storm damage to a home, auto collision repairs, vehicle theft, medical expenses under PIP, and stolen personal property covered by renters insurance.

Commercial first-party claims:

Commercial property damage from fire or weather, business interruption losses from covered events, cyber incidents including ransomware and data breaches, equipment theft, and cargo damage under inland marine policies.

For quick claim resolution in any of these scenarios, you need three things: proof that the event occurred, documentation linking the event to the loss, and confirmation that the peril is listed in your policy. Missing any one of these elements creates delays. Insurers assess first-party claims based on whether the event matches a covered policy peril and whether the valuation aligns with policy terms.

If you manage a commercial fleet, understanding trucking insurance coverage needs helps you identify which losses require first-party policies and which require liability coverage.

Benefits and limitations of first-party insurance coverage

The benefits of first-party insurance are significant, particularly for business owners who need fast financial recovery after a loss. The most direct advantage is speed. Because your insurer already holds your policy information and owes you a contractual duty, first-party claims typically resolve faster than third-party claims that require fault investigations and negotiations with another insurer.

You also do not need to prove that anyone else was negligent. A fire, a theft, or a cyberattack triggers your coverage based on the event itself, not on someone else’s liability. This removes a significant legal and procedural burden from your recovery process. For a trucking company or small business owner, that speed difference can determine whether operations resume in days or months.

First-party coverage also comes with clear limitations you should understand before relying on it. Coverage limits cap your payout, so underinsuring your property or fleet creates a gap between your actual loss and what the insurer pays. Deductibles reduce your net recovery. Filing a first-party claim may increase your premiums at renewal, which is a cost that accumulates over time.

First-party insurance does not cover damages you cause to others. If your truck injures another driver, your first-party policies do not respond to that driver’s losses. That is the role of liability coverage. Confusing the two leads to coverage gaps that can expose you to significant financial risk.

Common mistakes policyholders make include failing to read covered peril lists carefully, assuming all losses are covered when many policies exclude floods, earthquakes, or specific business risks, and delaying claim filing past policy deadlines. Review your policy terms annually, confirm that your coverage limits reflect current asset values, and understand your deductible structure before a loss occurs.

Key takeaways

First-party insurance pays you directly for your own covered losses, making it the fastest and most direct path to financial recovery after a covered event.

| Point | Details |

|---|---|

| First-party definition | Coverage that pays the policyholder directly for their own losses, not others’ damages. |

| No fault required | You only need to show a covered event caused the loss, not that someone else was negligent. |

| Faster claims resolution | Direct insurer duty to you speeds payment compared to third-party fault investigations. |

| Coverage has limits | Deductibles and policy caps reduce payouts; premiums may rise after filing a claim. |

| One event, two claims | A single incident can trigger both first-party and third-party claims with separate processes. |

Why knowing this distinction matters more than most people realize

I have worked with enough fleet operators and small business owners to know that most of them conflate first-party and third-party insurance until a loss forces the distinction into focus. By then, the confusion costs them time and money.

The most common mistake I see is business owners filing a third-party claim when a first-party claim would resolve faster and with less friction. After a collision where fault is disputed, waiting for the other insurer to accept liability can take weeks. Filing under your own collision coverage gets your truck repaired and back on the road in days. You pay the deductible, yes, but you recover operational capacity immediately.

The second mistake is underestimating how first-party coverage fits into a broader risk management strategy. Cyber insurance, business interruption coverage, and commercial property policies are all first-party instruments. They are not optional add-ons for large corporations. A single ransomware attack or warehouse fire without adequate first-party coverage can end a small trucking operation permanently.

My recommendation is to treat your first-party policies as your primary financial recovery tools and your liability policies as your legal protection layer. Review both annually, confirm that limits match current asset values, and work with an insurer who explains the difference clearly rather than selling you a package without context. If you manage a fleet, understanding how to file claims efficiently is as important as having the right coverage in the first place.

— Vladimir

Protect your fleet with the right first-party coverage

Diamondbackins specializes in commercial trucking and fleet insurance that includes first-party coverage options built for the realities of transportation operations. Whether you need commercial property protection, collision coverage for your vehicles, or cyber insurance for your business systems, Diamondbackins aggregates quotes from multiple top insurers so you can compare options and purchase a policy in minutes. If you operate in Georgia or across state lines, explore commercial trucking insurance options tailored to your fleet’s specific needs. For a broader overview of what trucking coverage includes, the trucking insurance guide at Diamondbackins walks you through every coverage type clearly and without the sales pressure.

FAQ

What is the first-party insurance definition in simple terms?

First-party insurance is coverage that pays you, the policyholder, for your own losses caused by a covered event. Common examples include homeowners insurance, auto collision coverage, and business interruption insurance.

Does first-party insurance require proving fault?

No. First-party claims require only that a covered event caused your loss, not that another party was negligent. This is one of its primary advantages over third-party claims.

What is the difference between first-party and third-party insurance?

First-party insurance pays the policyholder for their own losses; third-party insurance pays others harmed by the policyholder’s negligence. The claim is filed with your own insurer for first-party coverage and against someone else’s insurer for third-party coverage.

Who needs first-party insurance?

Any individual or business with assets at risk needs first-party coverage. Fleet operators, trucking companies, homeowners, and businesses with physical or digital assets all depend on first-party policies for direct loss recovery.

Can one accident trigger both first-party and third-party claims?

Yes. One loss event can trigger both claim types simultaneously, with separate adjusters and separate evidence requirements. For example, a trucking collision may generate a first-party collision claim for your vehicle and a third-party liability claim for the other driver’s injuries.

Recommended

- What Is Primary Liability Insurance for Business Owners

- Fleet Manager Insurance Guide: Protect Your Fleet in 2026

- The Essential Guide to General Liability Insurance for Small Businesses – Diamondback Insurance – Solutions with Instant Online Quotes

- Explaining Insurance Rating Factors for Smarter Coverage