Excess liability insurance is a secondary policy that extends the coverage limits of your primary liability insurance once those limits are fully exhausted, protecting you from catastrophic financial loss on large claims. Unlike standard liability policies, it does not introduce new coverage terms. It mirrors the conditions, exclusions, and definitions of your underlying policy, a structure the industry calls a “follow-form” policy. For trucking companies, fleet operators, and business owners facing a litigation environment where a single verdict can exceed millions of dollars, understanding excess liability coverage is no longer optional. It is a core part of responsible risk management.

What is excess liability insurance and how does it work?

Excess liability insurance is defined as a policy that sits above your primary liability coverage and pays claims only after the underlying policy’s limits are completely used up. The primary policy functions as the first line of defense. Once its per-occurrence or aggregate limit is exhausted, the excess policy takes over and pays the remaining covered loss up to its own stated limit.

The “follow-form” principle is the most important mechanic to understand. Excess liability strictly mirrors the terms, conditions, and exclusions of the primary policy beneath it. If your primary commercial auto policy excludes a specific type of cargo damage, your excess policy excludes it too. No new coverage is created. This is a feature, not a flaw. It keeps the policy structure predictable and reduces disputes at claim time.

Here is how a typical claim sequence works in practice. Imagine a trucking company faces a $3 million bodily injury lawsuit after a serious highway accident. The primary commercial auto policy carries a $1 million limit. The insurer pays that $1 million in full. The remaining $2 million then triggers the excess liability policy, which pays the balance up to its own limit. Without excess coverage, the business owner absorbs that $2 million personally or through company assets.

One critical and often overlooked mechanic involves aggregate limits. Multiple smaller claims can deplete a primary policy’s annual aggregate limit far faster than a single large event. Once the aggregate is exhausted, every subsequent claim in that policy year goes directly to the excess layer. Monitoring your aggregate exposure throughout the year is not optional. It is a financial discipline.

Pro Tip: Review your primary policy’s aggregate limit at mid-year, not just at renewal. If you have had several claims, your excess coverage may already be closer to activation than you realize.

It is also worth noting that excess policies carry no separate deductible. The primary policy’s fully exhausted limit serves as the effective threshold before excess coverage begins paying. You do not write a separate check to activate it.

What are the key differences between excess liability and umbrella insurance?

Excess liability and umbrella insurance are frequently confused, but they serve meaningfully different functions. Choosing the wrong structure can leave significant gaps in your protection.

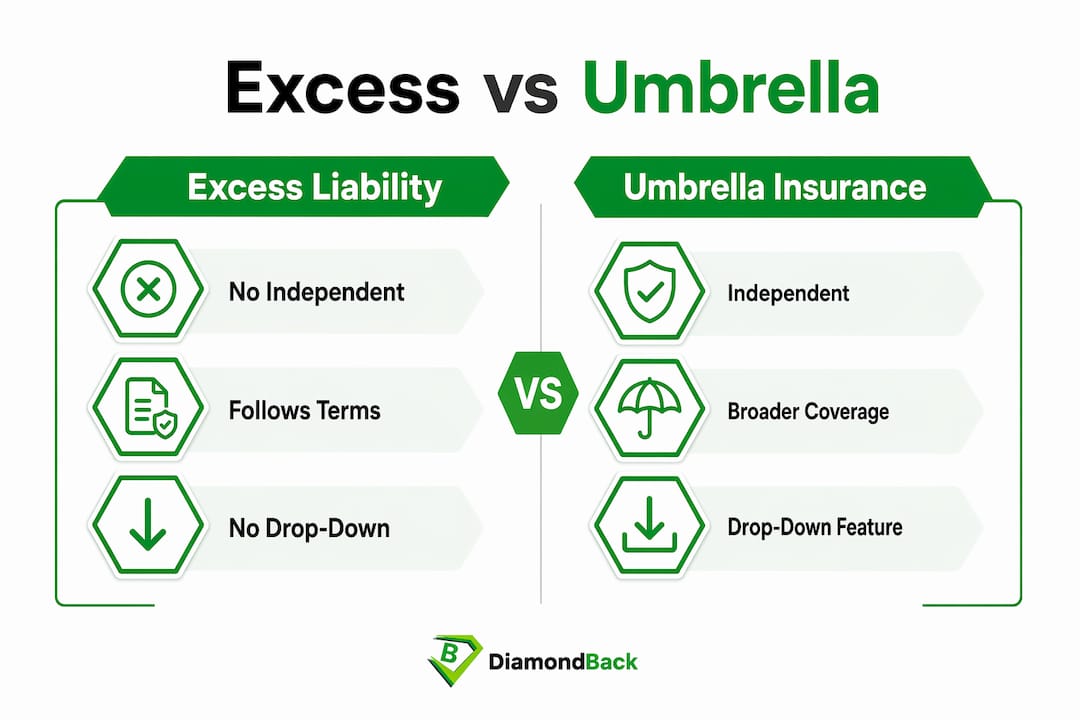

The most fundamental difference is the insuring agreement. Excess liability has no independent insuring agreement of its own. It borrows the agreement from the underlying policy and simply raises the dollar ceiling. An umbrella policy, by contrast, carries its own insuring agreement and can cover risks that the underlying policies do not address at all.

The second major distinction is the “drop-down” feature. Umbrella policies can drop down to cover a claim when an underlying policy is exhausted or when a gap exists in the underlying coverage. Excess liability cannot do this. It only pays when the specific underlying policy it sits above is fully exhausted. If a claim falls into a coverage gap in the primary policy, the excess layer does not respond.

| Feature | Excess Liability | Umbrella Insurance |

|---|---|---|

| Independent insuring agreement | No | Yes |

| Drop-down coverage for gaps | No | Yes |

| Mirrors underlying policy terms | Yes, strictly | Partially |

| Covers additional risk categories | No | Yes |

| Best suited for | Large, complex accounts | Small to mid-size businesses |

| Policy layering | Stacks above umbrella | Sits above primary policies |

Excess liability suits businesses with complex, layered insurance programs, large accounts, and sophisticated risk management teams. Umbrella policies are generally the better fit for smaller businesses that want broader protection without managing multiple policy layers. For trucking fleets with substantial assets and high-frequency operations, excess coverage often sits above an umbrella layer, creating a stacked structure that maximizes protection at each tier.

Cost differences follow logically from these structural differences. Umbrella policies typically cost more per dollar of coverage because they carry their own insuring agreement and broader risk scope. Excess policies are generally priced more narrowly because they are strictly limited to extending one underlying policy’s limits.

Why excess liability insurance matters for businesses and individuals

The financial case for excess liability coverage has never been stronger. Nuclear verdict awards reached $31.3 billion in 2024, doubling the prior year’s total. This figure represents a seismic shift in litigation risk that standard liability limits were never designed to absorb.

“Rising social inflation and nuclear verdicts have caused a 16% average rate increase in U.S. excess liability premiums year-over-year as of 2025. Businesses that delay purchasing excess coverage are effectively betting that their next claim will stay within their primary policy’s limits.”

For trucking companies and fleet operators, the exposure is especially acute. A single serious accident involving a commercial vehicle can generate bodily injury claims, property damage claims, and wrongful death suits simultaneously. Excess coverage protects business assets from catastrophic losses that exceed standard policy limits, preventing insolvency from unexpectedly large payouts. Without it, a judgment that exceeds your primary limit becomes a direct threat to your company’s solvency, real estate holdings, and personal assets.

The litigation environment has also grown more unpredictable. Juries in certain jurisdictions are awarding punitive damages at rates that would have been considered extreme just five years ago. Social inflation, defined as the tendency for claim costs to rise faster than general economic inflation due to legal system changes and jury behavior, is now a permanent feature of the risk environment. Businesses with significant public exposure, including transportation companies, contractors, and manufacturers, face the highest concentration of this risk.

Large multinational companies have responded by turning to specialized excess casualty facilities, with insurers like Chubb and Zurich launching dedicated programs to address scarce market capacity. This signals that even the largest organizations recognize that standard excess coverage structures are being tested by today’s claims environment.

What to consider before purchasing an excess liability policy

Buying excess liability coverage requires more than selecting a limit and signing a form. Several structural and contractual factors determine whether the policy actually performs when you need it.

The first consideration is the “no broader than underlying” principle. Your excess policy will never cover more than your primary policy covers. Before purchasing excess coverage, conduct a thorough review of your primary policy’s exclusions. Any gap at the primary level becomes a permanent gap at the excess level. This is especially relevant for trucking operators who may carry multiple underlying policies across commercial auto, general liability, and cargo coverage.

The second factor is aggregate limit monitoring. As noted earlier, aggregate limit exhaustion can activate your excess layer faster than expected when multiple smaller claims accumulate. Work with your broker to track aggregate consumption throughout the policy year, not just at renewal.

Policy wording deserves careful attention, particularly setoff clauses. Disputes over setoff language show that insurers may subtract payments received from third parties before settling an excess claim, effectively reducing the benefit you receive despite the policy’s stated limit. Ask your broker to identify any setoff or offset provisions in the policy before you bind coverage.

Choosing the right limit requires an honest assessment of your risk exposure. Consider the value of your business assets, the jurisdictions where you operate, your claims history, and the severity of potential accidents in your industry. For trucking fleets determining coverage limits, the calculation must account for the full range of liability scenarios, including multi-vehicle accidents and catastrophic bodily injury claims.

Pro Tip: When scheduling underlying policies on your excess application, list every primary policy that the excess layer is intended to sit above. An unlisted policy may not be covered by the excess layer, leaving you exposed in a claim.

Key takeaways

Excess liability insurance is the most direct tool available for protecting business assets against claims that exceed primary policy limits, and its value grows proportionally with your exposure to large verdicts.

| Point | Details |

|---|---|

| Follow-form structure | Excess policies mirror primary policy terms exactly, creating no new coverage. |

| Activation threshold | Excess coverage begins only after primary policy limits are fully exhausted. |

| Umbrella vs. excess | Umbrella policies offer drop-down coverage and broader terms; excess only raises the limit. |

| Nuclear verdict risk | Verdict awards reached $31.3 billion in 2024, making excess coverage a financial necessity. |

| Policy wording matters | Setoff clauses and aggregate limits can significantly affect actual payout at claim time. |

My take on excess liability in a market that has changed permanently

I have watched the excess liability market shift from a relatively predictable, affordable layer of protection to one of the most volatile segments in commercial insurance. The businesses that are getting hurt are not the ones that skipped coverage entirely. They are the ones that bought it years ago, never reviewed it, and assumed their limits were still adequate.

The follow-form structure is both the strength and the trap of excess liability. It keeps things simple, but it also means that a poorly written primary policy creates a poorly protected excess layer. I have seen trucking operators with $10 million in excess coverage discover at claim time that a key exclusion in their primary commercial auto policy rendered the excess layer irrelevant for the specific loss they suffered.

The rise of nuclear verdicts changes the math on limit selection. A $5 million excess limit felt generous in 2018. In 2026, with layered liability protection becoming standard practice for serious fleet operators, that same limit can look thin against a catastrophic multi-plaintiff claim. My advice is to review your limits every renewal cycle, not every few years.

The market capacity issue is real and growing. Large accounts are finding that excess capacity is harder to place and more expensive than it was three years ago. If you operate a mid-size fleet and have not locked in your excess layer early in your renewal cycle, you may find fewer options and higher premiums than expected. Start the conversation with your broker 90 days before renewal, not 30.

— Vladimir

How Diamondbackins can help you secure the right coverage

Diamondbackins specializes in helping trucking companies and fleet operators build layered insurance programs that include the right excess liability coverage for their specific risk profile. The platform aggregates quotes from multiple top-rated insurers, giving you the ability to compare excess liability options side by side without the delays of traditional brokerage. Whether you operate a single commercial truck or a regional fleet, Diamondbackins provides instant, tailored quotes that account for your underlying policy structure. Explore commercial trucking insurance in Georgia or review trucking insurance options to find the excess coverage layer your business needs today.

FAQ

What is excess liability insurance in simple terms?

Excess liability insurance is a policy that pays claims after your primary liability insurance limit is fully used up. It extends your coverage ceiling without changing the terms of your underlying policy.

How does excess liability differ from umbrella insurance?

Umbrella insurance carries its own insuring agreement and can cover gaps in underlying policies, while excess liability only raises the dollar limit of one specific underlying policy and cannot drop down to fill coverage gaps.

Who needs excess liability insurance?

Businesses with significant assets, high public exposure, or operations in litigation-heavy industries, including trucking companies, contractors, and manufacturers, benefit most from excess liability coverage. Individuals with substantial personal assets also use it to protect against large civil judgments.

Does excess liability insurance have a deductible?

Excess liability policies carry no separate deductible. The primary policy’s fully exhausted limit serves as the effective threshold, and the excess layer begins paying only after that threshold is met.

How much does excess liability coverage cost?

Excess liability premiums vary based on the underlying policy limits, industry risk profile, claims history, and chosen excess limit. Rates have risen an average of 16% year-over-year as of 2025, driven by nuclear verdicts and social inflation trends.

Recommended

- The Essential Guide to General Liability Insurance for Small Businesses – Diamondback Insurance – Solutions with Instant Online Quotes

- Navigating the Waters of General Liability Insurance What It Means for Your Business – Diamondback Insurance – Solutions with Instant Online Quotes

- What Is Primary Liability Insurance for Business Owners

- What is General Liability Insurance? Your Shield in the Business World – Diamondback Insurance – Solutions with Instant Online Quotes