Many trucking operators and small business owners believe that forming an LLC or carrying the state minimum insurance is enough to protect them from financial ruin. It is not. A single accident on the road can trigger a lawsuit that runs well past your policy limits, leaving your business assets exposed. Limited liability coverage sits at the intersection of legal protection and insurance policy design, and misunderstanding how either one works can cost you everything. This guide breaks down what limited liability coverage actually means, how it functions in trucking and small business insurance, what it costs, and where the gaps are that most operators never see coming.

Table of Contents

- What is limited liability coverage?

- How does limited liability coverage work in trucking and small business insurance?

- Comparing types of liability insurance: What fits your operation?

- How much does limited liability coverage cost?

- Why liability coverage alone isn’t enough: Hard truths for operators

- Get covered: Protect your trucks and business with the right liability insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Liability coverage limits | Your insurance only pays up to policy limits—big verdicts can go higher. |

| Legal vs insurance shield | LLC structure and liability coverage together reduce but don’t eliminate your risk. |

| Cost factors | Premiums depend on coverage chosen, vehicle details, and business history. |

| Understand exclusions | Some activities, like off-dispatch and loading, require additional policies. |

What is limited liability coverage?

With the risks clearly set, let’s clarify what limited liability actually means for your business. The term gets used in two very different contexts, and mixing them up is one of the most common and costly mistakes operators make.

In a legal sense, limited liability refers to the protection that business structures like LLCs and corporations provide to their owners. When you form an LLC, the law generally separates your personal assets from your business debts and obligations. If your trucking business gets sued, creditors typically cannot come after your personal home, savings, or vehicle. This protection is real, but it is not absolute. Courts can and do pierce the corporate veil when owners fail to maintain proper separation between personal and business finances, skip required documentation, or act fraudulently.

In an insurance sense, limited liability coverage means something more specific. Business liability insurance pays for damages to third parties, covering bodily injury and property damage in covered incidents, up to the policy limit. The word “limited” here refers to the dollar cap on your policy. Once a claim exceeds that cap, you are personally or commercially responsible for the remainder. This is the gap most operators overlook.

Think of it this way: your LLC is a legal wall, and your insurance policy is a financial cushion in front of that wall. Both have limits. Understanding general liability coverage for LLCs helps you see how these two layers interact and where each one stops protecting you.

Here is what limited liability coverage generally includes in a standard commercial policy:

Third-party bodily injury costs, including medical expenses and lost wages for people injured in accidents you cause. Property damage to vehicles, buildings, or cargo belonging to others. Legal defense costs, which can be significant even when you win a case. Settlements and court-ordered judgments, up to your selected policy limit.

What it does not include is just as important. What general liability insurance covers goes beyond the basics, but standard policies typically exclude damage to your own property, employee injuries (covered by workers’ compensation), and intentional acts.

Key insight: Your policy limit is your real ceiling of protection. A $1 million policy does not mean unlimited coverage. It means the insurer pays up to $1 million, and anything above that becomes your problem.

How does limited liability coverage work in trucking and small business insurance?

Once you understand the definitions, it is crucial to see how these protections operate in real-world trucking and business insurance. Coverage does not activate automatically. It triggers based on specific conditions defined in your policy.

Primary liability insurance is the foundation of any trucking operation. It covers third-party injuries and property damage that you cause while operating your commercial vehicle during business operations. The key phrase is “during business operations.” If you are driving your rig to a repair shop off-dispatch, that trip may not be covered under your primary policy. You would need bobtail or non-trucking liability (NTL) coverage for those gaps.

The Federal Motor Carrier Safety Administration, known as the FMCSA, sets the floor for how much coverage you must carry. FMCSA minimum coverage requires at least $750,000 for most general freight trucking operations. Carriers hauling hazardous materials face minimums of $1 million to $5 million depending on the commodity. Many brokers and shippers will not work with you unless you carry at least $1 million in coverage, regardless of what the law requires.

Here is why those minimums may not be enough. The average trucking verdict now exceeds $2.3 million, and so-called nuclear verdicts, those massive jury awards in catastrophic cases, can top $10 million. A $750,000 policy leaves a significant gap in those scenarios.

Pro Tip: Review your policy declarations page carefully. Confirm whether your limit is per-occurrence (applies to each individual claim) or aggregate (the total the insurer pays across all claims in a policy year). Both matter, and confusing them can leave you underinsured mid-year.

Understanding general liability insurance costs is part of planning your coverage strategy. Paying a bit more for higher limits now is almost always cheaper than facing a judgment that blows past your policy ceiling.

Key situations where coverage does not apply include: driving off-dispatch without bobtail coverage, loading and unloading accidents without a specific endorsement, incidents involving employees (workers’ compensation applies instead), and claims that exceed your policy’s dollar limit.

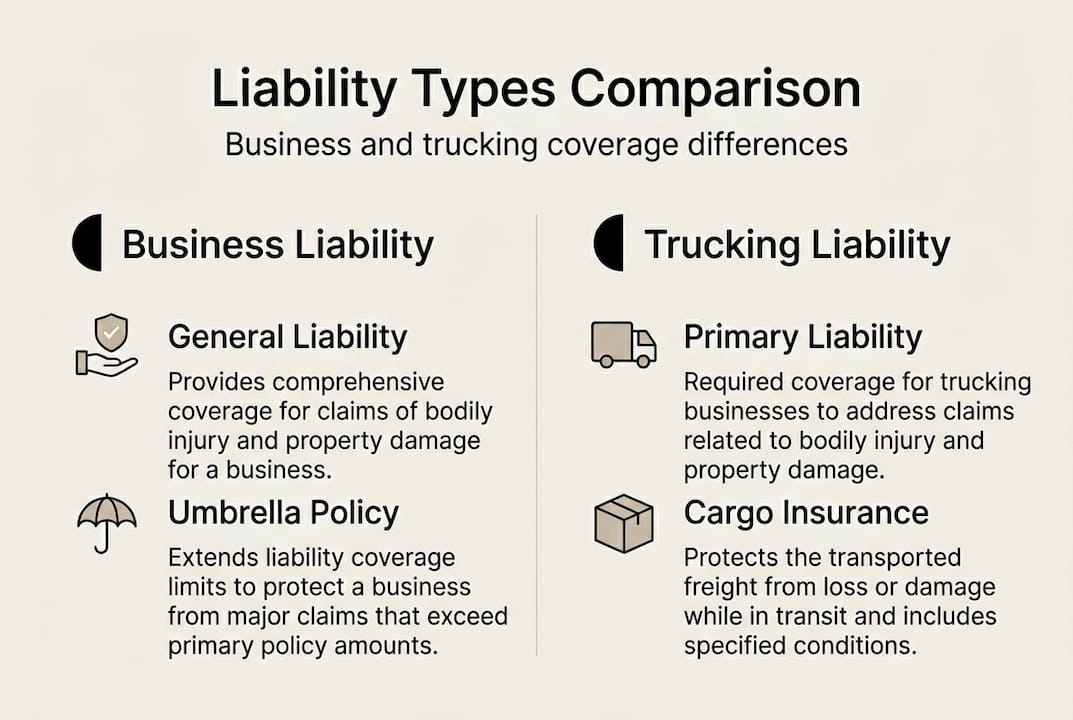

Comparing types of liability insurance: What fits your operation?

Knowing how coverage works, compare the different policy types you might need as your risk grows. Not every trucking operation has the same exposure, and stacking the right coverage types is how you close the gaps.

| Coverage type | What it covers | When you need it |

|---|---|---|

| Primary liability | Third-party injury/property damage on dispatch | Required by law for all motor carriers |

| General liability | Slip-and-fall, loading dock accidents, non-auto incidents | Small businesses, owner-operators with physical locations |

| Cargo insurance | Damage or loss of the freight you haul | Required by most brokers and shippers |

| Bobtail/NTL | Off-dispatch driving without a trailer | Owner-operators leased to a carrier |

| Umbrella/excess liability | Claims above your primary policy limits | High-value loads, high-traffic routes, larger fleets |

Primary liability is the legal baseline. It protects you when you cause an accident while on the job. But it does not cover everything. Bobtail/NTL, general liability, and umbrella insurance may all be required beyond primary liability for truly comprehensive protection.

General liability fills the spaces that commercial auto does not reach. If a customer slips on your loading dock or your employee damages a client’s property while not driving, general liability responds. Protecting your LLC with general liability coverage is especially important for small businesses that interact with the public or operate out of a physical space.

Umbrella and excess liability policies sit on top of your existing coverage. They activate only after your primary limits are exhausted. For operators running high-value loads or operating in dense urban corridors, an umbrella policy is not optional. It is the liability insurance safety net that catches what everything else misses.

Cargo insurance is separate from liability but equally important. It covers the freight itself if it is lost, stolen, or damaged in transit. Most brokers require proof of cargo coverage before they will assign you a load.

How much does limited liability coverage cost?

After examining what coverage you need, cost becomes the next major hurdle. Let’s spell out the numbers.

For owner-operators running a single truck, annual liability premiums typically range from $8,000 to $14,000 per year. That range is wide because your actual premium depends on several variables that insurers weigh carefully.

| Factor | Impact on premium |

|---|---|

| Type of cargo hauled | Hazmat or high-value loads cost more |

| Operating radius | Long-haul interstate costs more than local |

| CSA safety score | Poor scores raise premiums significantly |

| Claims history | Prior claims increase your risk profile |

| Years in business | New authorities pay more than established ones |

| Coverage limits selected | Higher limits mean higher premiums |

Your CSA score, which stands for Compliance, Safety, Accountability and is tracked by the FMCSA, is one of the most controllable factors. Operators with clean safety records and no recent violations consistently pay less. Investing in driver training and vehicle maintenance is not just good practice. It directly reduces what you pay for insurance.

Pro Tip: Ask your insurer about a Business Owner’s Policy (BOP), which bundles general liability and commercial property coverage at a lower combined rate than buying each separately. Not all trucking operations qualify, but small businesses with a physical location often do.

Understanding liability insurance costs in detail helps you budget accurately and avoid being caught off guard at renewal. Shopping multiple carriers, maintaining a clean record, and reviewing your limits annually are the three most reliable ways to keep premiums manageable without sacrificing protection.

Why liability coverage alone isn’t enough: Hard truths for operators

While the cost and options are clear, the next step is understanding where even full coverage might still leave you at risk. This is where we want to be direct with you.

Many operators assume that carrying insurance and forming an LLC makes them lawsuit-proof. It does not. Courts can pierce the LLC veil when business and personal finances are mixed, when corporate formalities are ignored, or when fraud is involved. Your legal protection disappears the moment a court decides you did not treat your business like a real business.

On the insurance side, nuclear verdicts are not rare events anymore. A $2 million judgment against a $750,000 policy leaves $1.25 million uncovered. That gap can bankrupt an operation that took years to build. What liability insurance means in practical terms is that you are protected up to a number, not unconditionally.

Our advice: keep your business and personal finances completely separate, document every policy and safety procedure, and revisit your coverage limits every year. The trucking landscape changes, verdicts grow, and your operation evolves. Your insurance should keep pace.

Get covered: Protect your trucks and business with the right liability insurance

You now understand what limited liability coverage is, how it works, what it costs, and where it can fall short. The next step is turning that knowledge into real protection for your business.

At Diamondback Insurance, we make it straightforward to compare solutions for general liability insurance tailored specifically for trucking operators and small business owners. Our platform pulls quotes from multiple top-rated insurers so you can compare options in minutes, not days. Whether you are looking for primary liability, general liability, or umbrella coverage, the liability guide for small businesses on our site can help you identify the right fit. Start comparing instant insurance quotes today and secure the coverage your operation actually needs.

Frequently asked questions

What does limited liability coverage actually cover?

Limited liability coverage pays for bodily injury and property damage to third parties that you cause in covered incidents, up to the selected policy limit. It does not cover your own injuries, your own property, or claims that exceed your policy cap.

Is limited liability insurance required for all trucking companies?

The FMCSA minimum is $750,000 for most general freight trucking operations, but brokers and shippers frequently require $1 million or more before assigning loads.

What are the main exclusions in limited liability coverage?

Liability coverage excludes off-dispatch driving, loading and unloading incidents without an endorsement, intentional acts, and any claim amount that exceeds your policy’s dollar limit.

How can I lower my liability insurance costs as an owner-operator?

Improving your driving record, keeping your CSA score clean, and maintaining your vehicles consistently are the most effective ways to reduce premiums, and annual premium factors like claims history and coverage selected also play a significant role.

Recommended

- Safeguarding Your LLC: General Liability Insurance Explained – Diamondback Insurance – Solutions with Instant Online Quotes

- Safeguarding Your Texas Business: General Liability Insurance in the Lone Star State – Diamondback Insurance – Solutions with Instant Online Quotes

- Shielding Your California Business: General Liability Insurance in California – Diamondback Insurance – Solutions with Instant Online Quotes

- Protecting Your Business with General Liability and Workers’ Comp Insurance – Diamondback Insurance – Solutions with Instant Online Quotes