Running a fleet means managing a long list of moving parts, and your insurance coverage sits at the center of them all. Standard, off-the-shelf policies are built around assumptions that rarely match the actual risk profile of a trucking operation, which means you’re either paying for coverage you don’t need or, far worse, discovering gaps at the worst possible moment. Customized insurance changes that equation by aligning your coverage precisely with your routes, cargo types, vehicle count, and driver history, giving you stronger protection and a real path to lower premiums.

Table of Contents

- The pitfalls of standard insurance policies for fleets

- How customized insurance solutions work

- Major benefits: Savings, compliance, and business control

- Avoiding pitfalls: What to watch for when customizing your coverage

- The uncomfortable truth most fleet owners miss about insurance customization

- Ready to streamline your fleet’s insurance and save?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Standard policies fall short | Generic insurance often leaves costly gaps or overcharges trucking fleets. |

| Customization boosts savings | Tailored insurance can save fleets 20-30% over time and improve compliance. |

| Fleet safety matters | Documented safety practices directly lower premium costs for trucking businesses. |

| Watch for hidden costs | Customization is most valuable when you actively manage add-on fees and compliance documentation. |

| Proactive management pays off | True value from custom insurance comes when it’s paired with disciplined operations and risk controls. |

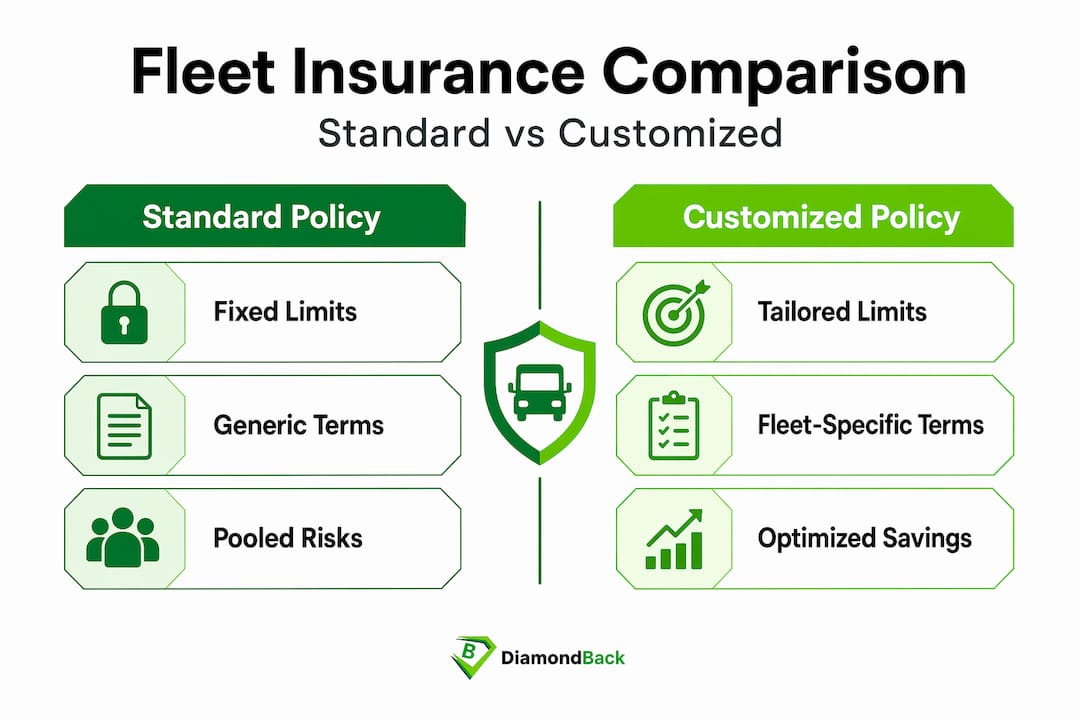

The pitfalls of standard insurance policies for fleets

If you manage a trucking fleet, you’ve probably encountered the frustration of trying to fit your operation into a policy that was never designed for it. Standard commercial auto policies are often written for a broad market, covering everything from delivery vans to construction vehicles. The result is a product that handles the average case adequately but the trucking-specific case poorly.

The core problem is coverage mismatch. A general commercial auto policy may set liability limits (the maximum your insurer pays on a claim) too low for the cargo values your trucks carry. It may exclude certain vehicle classes or leave out cargo coverage entirely. When you operate a refrigerated fleet or haul hazardous materials, those exclusions are not minor footnotes. They represent serious financial exposure that can threaten your entire business after a single incident.

Cost distortion is the other side of the same coin. Because standard insurers pool risk across many vehicle types and industries, your premium reflects averages rather than your actual track record. Specialized trucking insurance accounts for the specific exposures that a trucking fleet carries, which a generic policy simply cannot price accurately. You end up subsidizing risks that have nothing to do with your operation.

Modular add-on packages, which some insurers offer to make standard policies feel more flexible, bring their own challenges. Each added module introduces new terms, exclusions, and pricing layers. According to custom plan research, modular plans can generate higher costs for add-ons, and a poor safety history can push premiums up by 15 to 30 percent on top of already elevated base rates. Stacking modules without a clear strategy often produces a policy that is more expensive and harder to manage than a purpose-built trucking policy would be.

The key risks of using generic, cookie-cutter insurance for your fleet include the following realities. Coverage gaps in liability limits expose your assets directly when cargo values or route risks exceed what the policy covers. Blanket premium pricing ignores your fleet’s actual safety record and operational profile, so well-run fleets overpay. Confusing add-on structures make it difficult to verify what is and is not covered during a claim. Regulatory noncompliance is a serious risk when a standard policy fails to meet Federal Motor Carrier Safety Administration (FMCSA) minimum requirements for commercial trucking. Finally, premium spikes following even minor incidents can be disproportionate when your safety history is not properly documented.

“Standard policies often leave you paying for the average fleet’s risks, not your own. That pricing gap compounds every renewal cycle.”

With the drawbacks of standard fleet policies exposed, it’s important to understand how customized insurance stands apart.

How customized insurance solutions work

Customized fleet insurance starts with a detailed assessment of your operation rather than a generic application form. The insurer, or a platform that aggregates insurer options, gathers data about your vehicle types, cargo, routes, driver qualifications, safety programs, and claims history. That information becomes the foundation of a policy built around your actual risk profile rather than an industry average.

Understanding why trucking policies differ from standard commercial auto products helps you ask the right questions during this process. The differences touch every major coverage area, from primary liability to physical damage, non-trucking liability, and motor truck cargo coverage.

Fleet insurance often costs less per vehicle than individual policies and ensures regulatory compliance with FMCSA and state minimums, reducing the risk of fines and operational shutdowns. That compliance assurance alone is worth significant attention, because a single FMCSA violation tied to inadequate insurance can trigger a compliance review that disrupts your entire operation.

The customization process typically follows these steps.

First, you complete an operational profile that captures vehicle count, vehicle types, gross vehicle weight ratings, cargo categories, and primary operating states. Second, a coverage needs analysis maps your profile against FMCSA requirements and state-specific mandates, identifying the minimum thresholds you must meet. Third, an insurer or platform presents base policy options that satisfy those minimums and match your risk class. Fourth, you review optional enhancements such as increased cargo limits, trailer interchange coverage, or uninsured motorist provisions, evaluating each against its cost and your actual exposure. Fifth, the final policy is issued with documented coverage terms that you can verify against regulatory insurance requirements for your truck fleet at any time.

The comparison below shows how customized and standard fleet insurance typically differ across the factors that matter most to fleet managers.

| Factor | Standard fleet policy | Customized fleet policy |

|---|---|---|

| Liability limits | Fixed tiers, often generic | Set to match cargo value and route risk |

| FMCSA compliance | Varies, gaps possible | Built in and verified |

| Per-vehicle cost | Higher due to pooled risk | Lower through accurate risk matching |

| Cargo coverage | Often excluded or limited | Tailored to cargo type and value |

| Adjustment at renewal | Minimal flexibility | Adjusted to reflect current operations |

| Safety record credit | Rarely factored in | Directly reduces premiums |

Pro Tip: Documenting your fleet’s safety training, driver qualification files, and maintenance records before you begin the customization process gives insurers the evidence they need to price your risk accurately. Fleets that arrive at the quoting stage with organized records consistently receive better offers.

Now that you understand what sets customized insurance apart, let’s explore the concrete benefits fleets can gain beyond just basic compliance.

Major benefits: Savings, compliance, and business control

The financial case for customized insurance is well supported. Well-managed fleets save 20 to 30 percent on premiums over two consecutive insurance cycles when they combine customized coverage with documented safety and control practices. That is not a marginal improvement. For a mid-sized fleet carrying an annual premium of $150,000, a 25 percent saving represents $37,500 back in operating capital every year.

Compliance benefits are equally concrete. A customized policy built around FMCSA and state-specific minimums removes the guesswork from regulatory audits. When a compliance officer asks for your certificate of insurance, a customized policy provides clean documentation of every required coverage type and limit. Standard policies sometimes require supplemental endorsements to reach those minimums, which creates confusion and delays during audits.

Business control is the third major advantage, and it’s one that fleet managers often undervalue at the start. When your policy is structured around your actual operations, you control which risks you transfer to the insurer and which you manage internally. A fleet running well-maintained vehicles on known routes may choose higher deductibles in exchange for lower premiums, retaining the risk of smaller incidents while protecting against catastrophic losses. That kind of deliberate decision making is only possible when the policy is built around your specific profile.

The data below illustrates the documented savings potential at different fleet sizes.

| Fleet size | Estimated annual standard premium | Estimated customized premium savings | Annual savings |

|---|---|---|---|

| 5 vehicles | $45,000 | 20% | $9,000 |

| 15 vehicles | $130,000 | 25% | $32,500 |

| 30 vehicles | $255,000 | 28% | $71,400 |

| 50 vehicles | $420,000 | 30% | $126,000 |

Research on personalization in insurance shows that 60% of insurance customers are ready to switch providers when their coverage does not reflect their individual needs. For fleet managers, that willingness to switch is a practical reminder that your current insurer needs to earn your renewal with accurate, relevant pricing.

Learning how to compare insurance quotes across multiple insurers gives you the leverage to act on that willingness. Understanding how insurers evaluate transportation risk and cost for fleets helps you present your operation in the strongest possible light.

Pro Tip: Maintaining a clean record of safety audits, driver training completions, and preventive maintenance logs is the single most powerful action you can take before your next renewal. Insurers reward documented controls with direct premium reductions, and the evidence is far more persuasive than a verbal assurance about your safety culture. Platforms focused on saving on fleet insurance costs can help you organize and submit that documentation efficiently.

Having seen how custom insurance can boost compliance and financial control, it’s smart to anticipate common drawbacks and misunderstandings.

Avoiding pitfalls: What to watch for when customizing your coverage

Customization is genuinely powerful, but it comes with responsibility. The same flexibility that makes a custom policy valuable can create problems if you approach the process without preparation. Understanding the most common pitfalls before you start protects you from the situations where customization costs more rather than less.

Hidden fees in add-on modules are the most frequently reported problem. Modular plans can have hidden downsides including higher costs for individual add-ons and premium increases of 15 to 30 percent when safety histories are incomplete or negative. Each module you add should be evaluated not only on its sticker price but on how it interacts with your deductible structure, your claims history, and your compliance obligations.

Inadequate documentation is the second common pitfall. If you cannot demonstrate a clean safety record, drug and alcohol testing compliance, and current driver qualification files, an insurer will price your policy at a higher risk tier regardless of how the policy is structured. Customization cannot substitute for operational discipline.

Selecting coverage without experienced guidance is the third area where fleet managers frequently run into trouble. Finding the best insurance companies for truckers means working with advisors who understand the trucking regulatory environment, not just general commercial insurance principles.

The pitfalls to watch for, and the straightforward ways to avoid them, include the following. Review every add-on module line by line and request an explanation of how each one affects your base premium and deductible before you agree to it. Keep a centralized digital file of all safety records, maintenance logs, and driver qualification documents so you can produce them on demand during quoting and audits. Work with advisors who specialize in commercial trucking rather than general commercial auto, because the regulatory requirements are significantly different. Verify that every coverage limit in your customized policy meets or exceeds FMCSA minimums for your specific cargo and route classifications. And schedule an annual policy review at least 90 days before your renewal date, giving yourself time to make adjustments without pressure.

Pro Tip: Regularly review your policy with your insurance advisor at least once between renewal dates, not just at renewal. Operations change, routes expand, and vehicle counts shift throughout the year. A mid-cycle review ensures your coverage stays aligned with your current risk profile and prevents you from carrying either gaps or unnecessary coverage as your business evolves.

By understanding these risks from the start, you can approach custom insurance with confidence and get the best protection for your fleet.

The uncomfortable truth most fleet owners miss about insurance customization

Here is the view that most insurance discussions avoid: customized insurance is not a solution by itself. It is an amplifier. If your operations are disciplined, your safety records are current, and your drivers are well-managed, customization amplifies those strengths into real premium savings and airtight compliance. If your operations are inconsistent, your records are incomplete, and your safety culture is thin, customization amplifies those weaknesses into higher premiums, coverage disputes, and regulatory exposure.

Too many fleet owners approach custom insurance as a pricing shortcut. They believe that simply restructuring their policy terms will lower their costs without requiring any changes to how they actually run their operation. That belief leads to disappointment. Safety data gaps lead to higher fleet premiums, and well-managed fleets are the ones that genuinely save 20 to 30 percent over two cycles. The policy is the instrument. The operations are the music.

The fleet owners who extract the most value from customized insurance treat their insurer as a business partner rather than an annual vendor transaction. They share operational data proactively, update their safety documentation regularly, and have conversations about coverage adjustments before problems arise rather than after claims are filed. If you want to understand trucking insurance basics as a foundation, build on that knowledge by developing the operational discipline that makes a custom policy actually perform.

The lasting savings and compliance benefits from customized insurance come from the combination of a well-structured policy and a well-run fleet. Neither element alone gets you there.

Ready to streamline your fleet’s insurance and save?

Now that you understand the real impact of tailored coverage on your costs and compliance, taking the next step is straightforward. Diamondback Insurance is built specifically for fleet managers and trucking business owners who need fast, accurate, and genuinely customized insurance options without the complexity of working through traditional brokers.

You can streamline your fleet insurance process by getting multiple tailored quotes from top insurers in minutes, all through a single online platform designed around the trucking industry’s specific requirements. When you’re ready to evaluate your current coverage and see what a purpose-built policy would actually cost, instant fleet insurance quotes are available now, giving you the comparison data you need to make a confident, informed decision about your next policy cycle.

Frequently asked questions

How is customized fleet insurance more cost-effective than standard policies?

Customized fleet insurance often lowers per-vehicle costs by matching coverage to actual risks and meeting regulatory minimums precisely, unlike standard plans that can overcharge by pooling your fleet with unrelated vehicle types.

What risks come with customizing my fleet insurance?

Customization can introduce hidden costs if add-ons aren’t carefully selected, and incomplete safety records may lead to premium increases of 15 to 30 percent rather than savings.

How can documenting fleet safety affect our premiums?

Fleets with well-documented safety practices can save 20 to 30 percent on premiums over repeated insurance cycles by demonstrating measurably lower risk to insurers.

Do customized insurance plans guarantee regulatory compliance?

Well-designed customized plans should meet all FMCSA and state requirements, but it’s essential to work with advisors who specialize in trucking regulations to confirm every coverage limit is correct for your specific operation.