Trucking insurance costs have been climbing steadily, and if you manage a fleet or run a transportation business, you’re almost certainly feeling it. Insurance costs rose 3% in 2024 to 10.2 cents per mile, following a sharp 12.5% jump in 2023, with further increases expected in 2026. Yet many fleet owners respond to rising premiums by buying the bare minimum coverage and hoping for the best. That approach carries real risk. This guide breaks down what transportation insurance is, what the law requires, which coverage types you need, and how to keep costs manageable without leaving your business exposed.

Table of Contents

- What is transportation insurance and who needs it?

- FMCSA minimum insurance requirements explained

- Types of coverage every fleet should understand

- What’s driving insurance costs and how to control them

- A smarter approach: Don’t stop at the legal minimum

- Get expert help for better fleet insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Minimums aren’t enough | Legal minimum insurance will not fully protect your business from all real-world risks. |

| Coverage is specialized | Fleet owners need a mix of liability, cargo, and physical damage coverage tailored to their exposures. |

| Costs are rising | Insurance expenses have steadily increased, so cost-control requires proactive management. |

| Smart design saves | Building insurance coverage by analyzing real risks, not just filing requirements, leads to greater savings long term. |

What is transportation insurance and who needs it?

Transportation insurance is a broad category of commercial insurance designed to protect businesses that operate vehicles for commercial purposes. It covers liability, physical damage, and cargo risks that come with moving goods or passengers across roads and highways. Whether you run a single owner-operator rig or manage a fleet of 50 trucks, the coverage requirements that apply to you depend on how, where, and what you haul.

For fleet managers and small business owners, understanding the basics of transportation insurance starts with recognizing that this is not simply an upgrade of personal auto insurance. Commercial transportation insurance addresses exposures that personal policies explicitly exclude, including cargo liability, third-party bodily injury from commercial operations, and regulatory compliance filings.

Who is legally required to carry it?

The Federal Motor Carrier Safety Administration, commonly known as the FMCSA, sets the federal rules for motor carriers operating in interstate commerce. If your business transports goods or passengers across state lines, you almost certainly need to comply with FMCSA requirements. Importantly, FMCSA will not grant operating authority registration until minimum levels of financial responsibility are on file, which means you cannot legally operate without the right coverage in place.

The requirement also depends on your entity type, cargo classification, and vehicle type. For-hire carriers, contract carriers, and certain private carriers all face different thresholds. Brokers and freight forwarders have their own separate surety bond or trust fund requirements. Intrastate carriers operating only within one state may follow that state’s rules, which often mirror federal standards but can vary.

“FMCSA insurance requirements are tied to whether you need operating authority and depend on the entity type, cargo, and vehicle type.” This means one-size-fits-all coverage rarely works in trucking. Your specific operation determines exactly what you need on file.

FMCSA minimum insurance requirements explained

Once you know that your operation requires coverage, the next question is how much. The FMCSA sets minimum public liability limits based on the type of freight you carry and whether your operation is classified as for-hire or private. These minimums exist to protect the public in the event your vehicle is involved in an accident.

For most interstate for-hire trucking operations, the FMCSA baseline is $750,000 in public liability coverage for non-hazardous general freight. Operations hauling certain hazardous materials can be required to carry up to $5,000,000 in coverage. These are not suggestions; they are legally enforceable thresholds tied directly to your operating authority.

The table below outlines the most common FMCSA minimum liability requirements so you can quickly identify where your operation falls.

| Operation type | Cargo category | Minimum liability required |

|---|---|---|

| For-hire, interstate | Non-hazardous general freight | $750,000 |

| For-hire, interstate | Hazardous materials (certain) | $1,000,000 to $5,000,000 |

| For-hire, interstate | Oil (non-hazardous) | $1,000,000 |

| Passenger carrier | Small vehicles (under 16 passengers) | $1,500,000 |

| Passenger carrier | Larger vehicles (16+ passengers) | $5,000,000 |

| Private carrier | Hazardous materials | Varies by cargo type |

What happens if you fall short?

Failing to maintain the required insurance minimums on file with the FMCSA can result in your operating authority being revoked. Carriers found operating without the required financial responsibility face civil penalties that can reach thousands of dollars per violation per day. More significantly, if an uninsured or underinsured fleet vehicle is involved in a serious accident, your business can be held personally liable for damages that far exceed the policy limits you do have in place.

It is worth noting that the FMCSA minimums have not been updated since the 1980s for most freight categories. Many industry professionals argue these limits are no longer adequate given the scale of modern settlements and jury awards in truck accident litigation. That is an important context for understanding why buying only the bare minimum is a riskier strategy than it appears on paper.

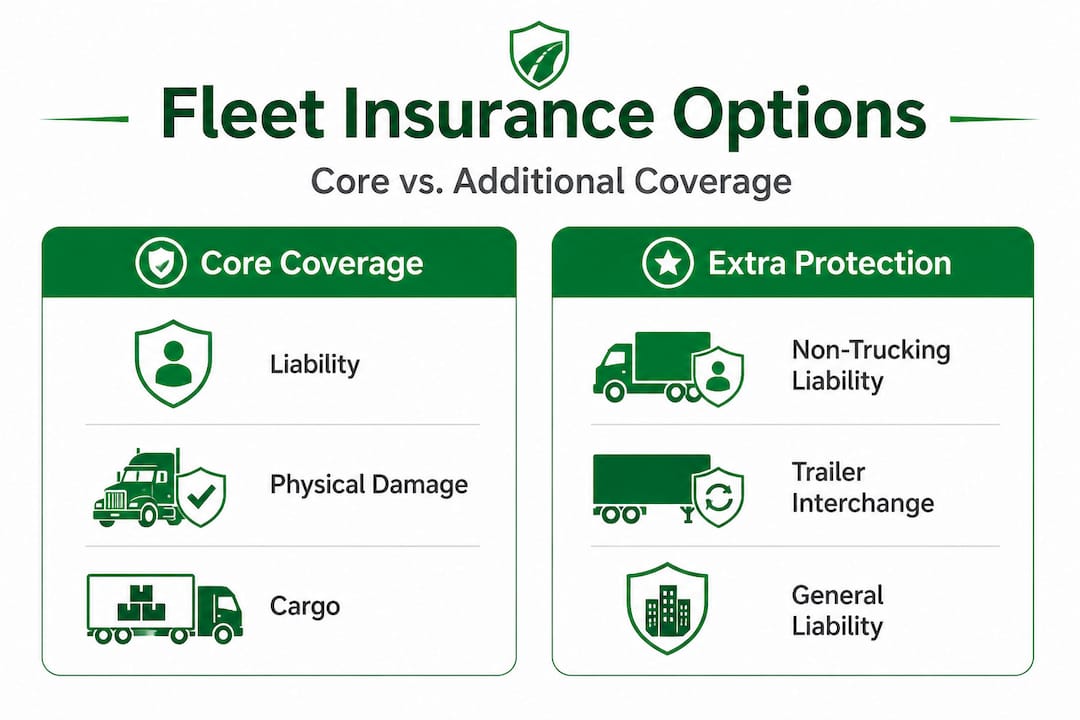

Types of coverage every fleet should understand

Meeting the FMCSA minimum gets you legal clearance to operate, but it does not necessarily protect all the things that matter most to your business. A well-designed insurance program for a fleet or trucking operation typically combines several types of coverage into a layered program, each addressing a distinct category of risk.

Primary liability coverage

This is the coverage tied to your operating authority and the one the FMCSA requires on file. It pays for bodily injury and property damage that your driver causes to third parties in an accident. This coverage travels with the truck and applies regardless of who owns the cargo onboard.

Physical damage coverage

Physical damage protects the truck itself, not the cargo or third parties. It includes collision coverage for accidents and comprehensive coverage for losses like theft, fire, or weather damage. For fleet operators with significant capital tied up in equipment, this protection is essential. A single total loss on a late-model semi-truck can exceed $150,000, and without physical damage coverage, that cost comes directly out of your operating budget.

Cargo insurance

Cargo coverage protects the freight your trucks are hauling. It pays out when cargo is lost, stolen, or damaged in transit. Shippers and brokers often require proof of cargo insurance before awarding loads. The right approach, as industry practice recommends, is to size cargo coverage to the maximum value of the load your fleet regularly carries and then add endorsements to match specific commodity risks such as refrigerated goods, electronics, or hazardous materials.

Pro Tip: One of the most common and costly cargo coverage mistakes is failing to review the commodity exclusions buried in your policy. Many standard cargo policies exclude electronics, pharmaceuticals, and temperature-sensitive goods by default. If you regularly haul any of these, a specific endorsement is not optional; it is essential.

Common endorsements and additional coverages

Beyond the core three, a complete fleet insurance program may include non-trucking liability (also called bobtail insurance) for when a driver operates the truck outside of dispatch, trailer interchange coverage, and uninsured motorist protection. Motor truck general liability, which covers accidents at loading docks or storage facilities, is another coverage that trucking insurance professionals frequently recommend for operations that involve regular facility stops.

The key principle is to build your coverage program around your actual exposures rather than around the lowest price point. Underinsuring cargo, skipping physical damage on high-value equipment, or ignoring bobtail exposure are all decisions that can cost far more than the premium savings they generate.

What’s driving insurance costs and how to control them

The 2024 increase in trucking insurance costs did not happen in a vacuum. Several interconnected pressures have been pushing rates up across the industry for several years, and the outlook for 2026 suggests these pressures are not easing.

The key drivers behind rising rates

Claims frequency and severity are both increasing. Accidents involving large commercial trucks tend to result in serious injuries, which translate into large settlements. Social inflation, meaning the tendency for juries to award larger verdicts in liability cases, has significantly increased the cost of resolving major claims. At the same time, the cost to repair or replace modern commercial trucks has risen sharply due to supply chain disruptions, parts shortages, and the growing complexity of truck technology.

Industrywide costs rose to 10.2 cents per mile in 2024, and the trend is expected to continue into 2026. For a truck that logs 100,000 miles per year, that translates to more than $10,000 in insurance costs per vehicle annually, before adding physical damage or cargo coverage.

“The carriers absorbing the largest rate increases are often those with the weakest safety records, highest claims frequency, and the least structured approach to risk management.” This means that how you manage your fleet directly affects what you pay.

Practical tactics to reduce your premiums

First, invest in a documented safety program. Insurers assess the quality of your safety management when pricing your policy. A formal written safety program, regular driver training, and a clean record of FMCSA compliance scores all signal lower risk, which translates to better rates. Your state-by-state insurance rates are also influenced by where your trucks operate most frequently, so understanding regional rating factors helps you plan routes and base locations strategically.

Second, review your factors affecting rates before each renewal. Driver age, years of CDL experience, MVR history, and prior claims all feed into your premium calculation. Removing high-risk drivers from your roster or investing in remedial training before renewal can move the needle noticeably.

Third, shop your coverage actively. The insurance market is competitive, and carriers price risk differently. Getting multiple quotes at each renewal, rather than simply accepting your renewal offer, frequently reveals meaningful savings. You can explore truck insurance cost benchmarks to understand what competitive pricing looks like for your operation type and size before you sit down to negotiate.

Fourth, consider your deductible structure carefully. Increasing your deductibles on physical damage coverage in exchange for a lower premium can make sense if your fleet has the cash reserves to absorb a minor loss. This effectively turns your fleet into a partial self-insurer for small claims while transferring the catastrophic risk to the insurer.

Pro Tip: Ask your insurer whether telematics data can lower your premium. Many carriers now offer discounts for fleets that install GPS and driver behavior monitoring systems. The data generated can demonstrate safe driving habits, reduce fraudulent claims, and provide critical documentation after an accident.

A smarter approach: Don’t stop at the legal minimum

Here is the uncomfortable truth that most discussions about fleet insurance gloss over. The minimum coverage required by the FMCSA was designed to protect the public, not your business. Treating these thresholds as your coverage target rather than your floor is one of the most financially dangerous decisions a fleet manager can make.

Consider a serious multi-vehicle accident where your truck is at fault. Medical costs alone for severe injuries can exceed $750,000 before any property damage, loss of income claims, or legal fees are factored in. If your coverage sits exactly at the $750,000 federal minimum and a jury awards $2 million in damages, the gap comes from your business assets. For a small fleet owner, that gap can mean bankruptcy.

The smarter perspective is to treat insurance not as a compliance cost to minimize, but as a risk management tool to optimize. That shift in thinking changes how you evaluate coverage decisions entirely. Instead of asking “what is the cheapest policy that keeps me legal?” you start asking “what level of coverage protects my business across the realistic range of losses I could face?”

Working with insurance experts who understand the trucking industry gives you access to this kind of strategic perspective. They can analyze your fleet’s actual exposure, identify gaps between what you carry and what your operation truly needs, and help you design a program that balances premium efficiency with genuine protection. The best fleet managers we have encountered treat their insurance renewal as a strategic review, not an annual transaction. They bring loss data, safety records, and route information to the conversation and use it to negotiate from a position of knowledge rather than guesswork.

Get expert help for better fleet insurance

Managing transportation insurance effectively requires more than just meeting the minimum requirements. It requires understanding your exposures, staying current with rate trends, and building a coverage program that actually protects your business when something goes wrong.

Diamondback Insurance makes that process faster and more transparent. You can read the full trucking insurance guide to deepen your understanding before you buy, or go straight to comparing options and get instant trucking quotes from multiple top-rated carriers in minutes. If cargo coverage is a gap in your current program, you can also explore cargo insurance options tailored to your commodity type and load values. The goal is to give you the information and the tools to make confident, cost-effective coverage decisions without the friction of a traditional broker process.

Frequently asked questions

What is the FMCSA’s minimum insurance requirement for commercial trucks?

Most interstate for-hire trucks carrying non-hazardous general freight must have at least $750,000 in public liability coverage, while certain hazardous materials operations can require up to $5,000,000.

Does transportation insurance cover both trucks and cargo?

Transportation insurance can cover both vehicles and cargo, but physical damage and cargo coverage are typically separate policies or endorsements that must be added intentionally based on your operation’s specific needs.

Why are trucking insurance costs rising?

Rates are climbing due to more frequent and severe accident claims, increased litigation costs, and higher repair expenses; industry costs rose 3% in 2024 to 10.2 cents per mile, and further increases are expected in 2026.

What are the main risks of buying only the minimum required coverage?

Bare-minimum coverage protects the public but leaves your business assets exposed to out-of-pocket losses that exceed your policy limits, which can threaten the financial survival of your entire operation after a serious accident.

How can I lower my fleet’s insurance premiums without sacrificing protection?

Develop and document a formal safety program, actively manage driver records, increase deductibles on physical damage where your cash reserves allow, and compare multiple carrier quotes at every renewal to ensure you are getting competitive pricing.