Trailer interchange insurance is defined as physical damage coverage for non-owned trailers in your possession under a written interchange agreement. Standard commercial auto policies cover only trailers you own. The moment you accept a trailer under a formal contract like the Uniform Intermodal Interchange Agreement (UIIA), you carry legal responsibility for that equipment. Without a dedicated trailer interchange policy, any damage that occurs while the trailer is in your care falls entirely on you. For fleet operators and transportation businesses, that gap in coverage represents serious financial exposure.

What is trailer interchange insurance and why does it exist?

Trailer interchange insurance fills a specific coverage gap that standard commercial auto policies leave open. Commercial auto physical damage insurance covers trailers you own. It does not cover trailers belonging to another carrier that you have accepted under a contractual arrangement.

The UIIA is the most widely used framework governing these arrangements in the United States. Under UIIA standards, minimum coverage requirements include $1 million in general liability and $1 million combined single limit auto liability, along with specified trailer interchange limits and deductibles. These are not suggestions. They are binding contractual obligations that carriers must meet before accepting equipment.

The insurance industry created trailer interchange coverage specifically because the liability transfer in these agreements is immediate and absolute. The second you sign for a trailer at the gate, you are responsible for it. A standard trucking policy does not protect you in that moment. Trailer interchange coverage does.

How do trailer interchange agreements create coverage obligations?

A trailer interchange agreement is a written contract between two carriers that governs the temporary transfer of trailer possession. The agreement defines who is responsible for the equipment, under what conditions, and for how long. Understanding how these agreements work is the foundation for understanding why the insurance exists.

Coverage under a trailer interchange policy attaches and releases at two specific points:

- Gate-out (acceptance): Coverage begins the moment you accept the trailer at the originating location. The carrier taking possession assumes full responsibility for physical damage from this point forward.

- Gate-in (return): Coverage ends when the trailer is returned and accepted by the other party. Until that handoff is confirmed, you remain liable.

- Written agreement requirement: Coverage is void if no written agreement exists at the time of acceptance. Verbal arrangements do not trigger coverage. This is a hard rule with no exceptions.

- UIIA standardization: The UIIA creates uniform insurance and liability terms across participating carriers. This reduces disputes about who owes what when damage occurs.

The written agreement requirement catches many operators off guard. If you accept a trailer informally, even from a long-standing partner, your trailer interchange policy will not respond to a damage claim. Always confirm the written agreement is in place before the trailer leaves the gate.

What does trailer interchange coverage actually protect?

Trailer interchange coverage protects the physical structure of the trailer itself against a defined list of perils. Covered damage includes collision, fire, theft, vandalism, and other physical damage events. The policy pays to repair or replace the trailer up to the agreed coverage limit.

One critical distinction: trailer interchange insurance does not cover the cargo inside the trailer. Cargo protection requires a separate motor truck cargo policy. Fleet operators who assume their interchange coverage handles both the trailer and its contents will face an unpleasant surprise after a loss.

How trailer interchange coverage compares to related policies:

| Coverage type | What it protects | Ownership requirement | Written agreement needed |

|---|---|---|---|

| Trailer interchange insurance | Non-owned trailers in your possession | Trailer must be owned by another party | Yes |

| Non-owned trailer coverage | Non-owned trailers attached to your tractor | Trailer must be non-owned | No formal agreement required |

| Commercial auto physical damage | Your owned trailers and vehicles | Must be owned by you | No |

| Motor truck cargo insurance | Freight and cargo in transit | Not applicable | No |

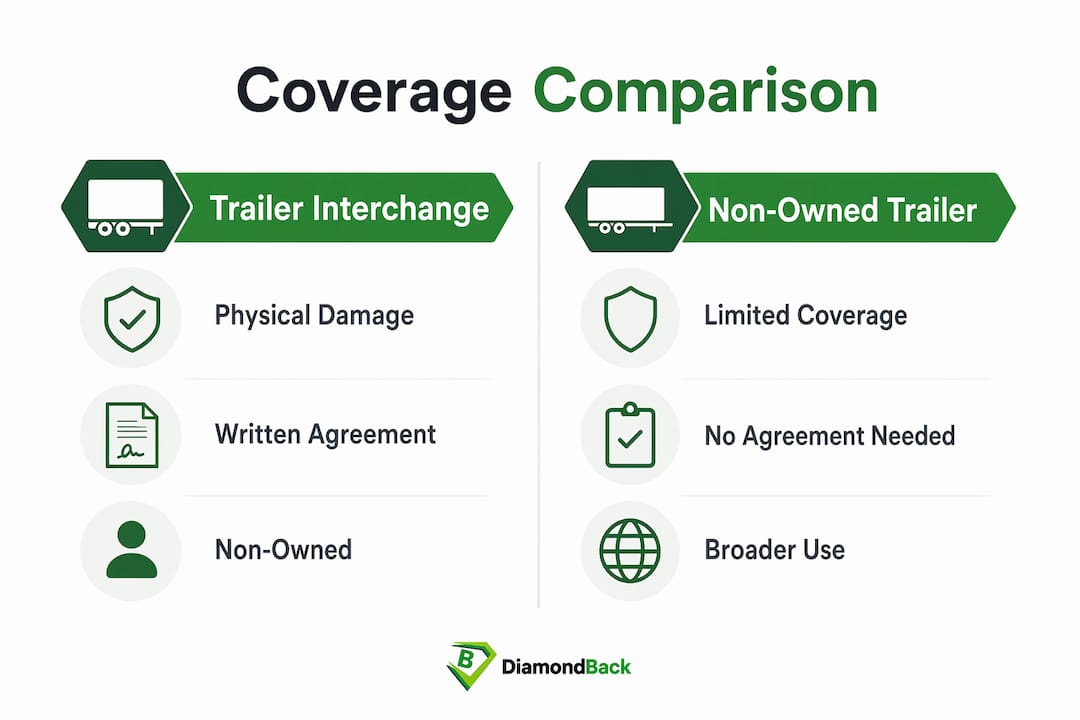

Non-owned trailer coverage and trailer interchange coverage are often confused. Non-owned trailer coverage typically applies when a trailer is attached to your tractor and no formal interchange agreement governs the arrangement. Trailer interchange coverage applies specifically when a written agreement assigns responsibility. The distinction matters because using the wrong policy at the wrong time results in a denied claim.

Policy limits also require careful attention. If your interchange agreement requires $50,000 in coverage but your policy only provides $20,000, you are personally responsible for the $30,000 difference in the event of a total loss. Matching your policy limits to your contractual requirements is not optional.

Pro Tip: Review every interchange agreement before you sign it. Pull the specific insurance limit requirements from the contract and confirm your policy meets or exceeds them. Do this every time you enter a new agreement, not just at policy renewal.

Why is trailer interchange insurance essential for your business?

Operating without proper trailer interchange coverage exposes your business to financial liability that can be both substantial and contractually binding. Physical damage to a trailer can easily reach tens of thousands of dollars. Without coverage, that cost comes directly out of your operating budget.

Beyond the immediate repair cost, there are broader business consequences to consider:

Breach of contract risk. Most interchange agreements require carriers to carry specific coverage limits. Failing to maintain those limits puts you in breach of contract. That breach can result in termination of the agreement, loss of business relationships, and potential legal action from the equipment owner.

Uninsured loss exposure. Industry experts consistently advise that carriers proactively manage coverage and contracts to avoid costly liability. A single uninsured trailer loss can disrupt cash flow, delay operations, and strain relationships with equipment providers.

Regulatory and compliance risk. Carriers operating under UIIA terms who fail to maintain required coverage levels risk losing their interchange privileges entirely. That loss can effectively shut down operations that depend on borrowed equipment.

Operational continuity. Proper coverage keeps your business moving after a loss event. With the right policy in place, a damaged trailer triggers a claim process rather than a financial crisis. That stability matters for fleet managers who need to maintain delivery commitments and client relationships.

Reviewing your trucking insurance coverage regularly is one of the most effective ways to prevent these gaps from developing. Agreements change, fleets grow, and coverage that was adequate last year may fall short today.

Pro Tip: Schedule a coverage review every time you sign a new interchange agreement or add trailers to your operation. Do not wait for annual renewal to catch a mismatch between your policy limits and your contractual obligations.

How to obtain trailer interchange insurance in practical steps

Securing the right trailer interchange policy requires a structured approach. Rushing the process often leads to coverage gaps that only surface after a loss.

- Assess your operational needs. Identify how many trailers you interchange, with which carriers, and under what agreements. This inventory determines the coverage limits and policy structure you need.

- Review all interchange agreements. Pull the insurance requirements from each written agreement. Note the required coverage limits, deductibles, and any additional insured requirements. These numbers set the floor for your policy.

- Engage a qualified insurance provider. Work with a provider experienced in commercial trucking insurance. Describe your interchange volume, the agreements you operate under, and the limits those agreements require. Diamondbackins specializes in this type of coverage and can match your needs to the right policy quickly.

- Verify coverage limits and endorsements. Confirm that your policy meets every contractual requirement before you accept any trailer. Check that the policy includes the correct deductible levels and any required endorsements.

- Obtain and distribute certificates of insurance. The certificate of insurance for trailer interchange coverage must list equipment providers as additional insureds and comply with UIIA documentation standards. Distribute updated certificates to all interchange partners promptly.

- Manage ongoing compliance. Review your policy at renewal and whenever your fleet size or interchange agreements change. Update coverage limits as needed to stay in compliance with all active agreements.

Trailer interchange insurance cost overview:

| Factor | Impact on premium |

|---|---|

| Fleet size | Larger fleets typically carry higher premiums |

| Coverage limits | Higher limits increase annual cost |

| Claims history | Prior losses raise premiums significantly |

| Deductible level | Higher deductibles reduce premium cost |

| Annual cost range | Approximately $100 to $1,500 per year |

The wide cost range reflects how differently individual operations are structured. A small carrier with a clean claims history and modest limits will pay far less than a large fleet with high coverage requirements and prior losses. Understanding the freight contract terms that govern your agreements also helps you negotiate coverage structures that keep costs manageable without creating liability gaps.

My take on trailer interchange insurance after years in this industry

Key Takeaways

Trailer interchange insurance is the only coverage that protects non-owned trailers in your possession under a written agreement, and no standard commercial auto policy replaces it.

| Point | Details |

|---|---|

| Coverage trigger | Protection starts at gate-out acceptance and ends at gate-in return, only with a written agreement. |

| Scope of protection | Covers physical damage to the trailer itself, not cargo, against collision, fire, theft, and vandalism. |

| Limit matching | Your policy limits must meet or exceed what each interchange agreement requires to avoid personal liability. |

| Documentation | Certificates of insurance must name equipment providers as additional insureds per UIIA standards. |

| Cost range | Annual premiums typically run $100 to $1,500, depending on fleet size, limits, and claims history. |

My take on trailer interchange insurance after years in this industry

The most common mistake I see fleet operators make is treating trailer interchange insurance as a formality rather than a financial safeguard. They get the policy, file the certificate, and never look at it again until something goes wrong. That approach works fine until it doesn’t.

The real risk is not a catastrophic accident. It’s the slow drift between what your agreements require and what your policy actually provides. Fleets grow. New interchange partners come with new contracts. Coverage limits that matched your agreements two years ago may fall short today. By the time you discover the gap, you’re already in breach of contract with a damaged trailer sitting in a yard.

My advice is straightforward. Read every interchange agreement before you sign it. Pull the insurance requirements out of the contract and put them next to your policy declarations page. If the numbers don’t match, fix the policy before you accept a single trailer. This takes 20 minutes and can save you tens of thousands of dollars.

I also recommend building a simple tracking document that lists every active interchange agreement, the required coverage limits, and your current policy limits. Review it quarterly. When agreements change or new ones are added, update the document and your coverage at the same time. Proactive management of your truck trailer coverage is far less expensive than reacting to an uninsured loss.

— Vladimir

Trailer interchange coverage made straightforward with Diamondbackins

Diamondbackins connects fleet operators and transportation businesses with tailored commercial trucking insurance, including trailer interchange coverage, through a fully online platform. You get instant quotes from multiple top insurers without the back-and-forth of traditional brokers.

Whether you operate under UIIA agreements or private interchange contracts, Diamondbackins helps you match your policy limits to your contractual requirements quickly and accurately. The platform is built for fleet managers who need coverage that works from the first gate-out to the last gate-in. Get your commercial trucking insurance quote today and confirm your trailer interchange coverage is exactly where it needs to be.

FAQ

What is trailer interchange insurance in simple terms?

Trailer interchange insurance covers physical damage to a trailer you don’t own while it’s in your possession under a written interchange agreement. It fills the gap that standard commercial auto policies leave open for non-owned equipment.

How does trailer interchange insurance differ from non-owned trailer coverage?

Trailer interchange insurance applies when a formal written agreement governs the transfer of trailer possession. Non-owned trailer coverage typically applies to trailers attached to your tractor without a formal interchange contract in place.

Is trailer interchange insurance required by law?

Trailer interchange insurance is not a federal legal requirement, but it is contractually required under most interchange agreements, including those governed by the UIIA, which mandates specific coverage limits and documentation standards.

How much does trailer interchange insurance cost?

Annual premiums for trailer interchange coverage typically range from $100 to $1,500, depending on fleet size, coverage limits, deductible levels, and claims history.

What happens if my coverage limits are lower than my agreement requires?

If your interchange agreement requires higher limits than your policy provides, you are personally liable for the difference. A $50,000 contractual requirement with only $20,000 in coverage leaves you responsible for a $30,000 shortfall on a total loss.