If you operate a commercial fleet or run trucks under lease agreements, your primary liability coverage may not protect you as much as you think. Most fleet owners assume their standard trucking policy has them covered around the clock, but NTL covers third-party injury and property damage specifically when a truck is used for personal, non-business activities. That gap between business use and personal use is exactly where expensive lawsuits and out-of-pocket claims can catch you off guard. With rising claims costs across the industry, understanding non-trucking liability (NTL) insurance is no longer optional; it is essential for any responsible fleet operator.

Table of Contents

- What is non-trucking liability insurance?

- Why fleet managers and owners can’t ignore off-duty risk

- How non-trucking liability fits your risk management strategy

- Non-trucking liability: Cost, compliance, and real-world benefits

- The truth insurance agents don’t tell fleets about off-duty coverage

- Protect your fleet: Affordable, trusted non-trucking liability options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Covers off-duty risks | Non-trucking liability insurance protects you when your truck is used for non-business activities. |

| Protects assets and compliance | NTL shields both fleet assets and personal finances, while keeping you compliant with most lease contracts. |

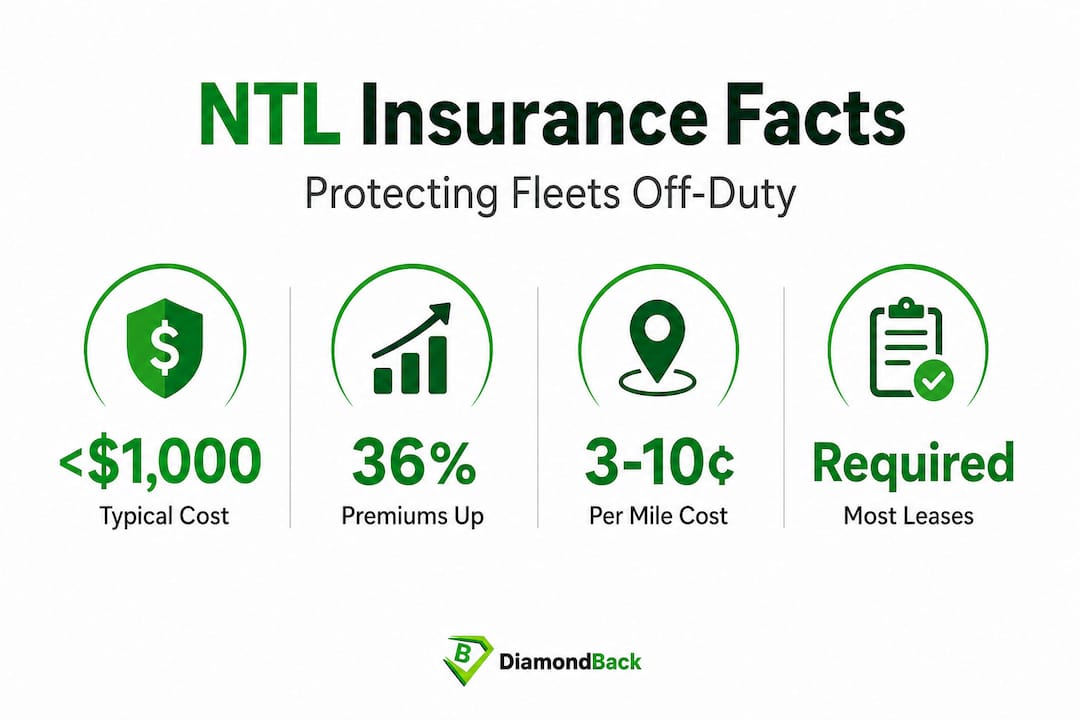

| Cost-effective protection | Typical premiums are under $1,000 per year, making NTL an affordable safeguard. |

| Controls rising insurance costs | NTL helps manage the industry trend of increasing liability expenses, supplementing other fleet coverage. |

What is non-trucking liability insurance?

Now that we’ve set the context for why off-duty risks matter, let’s break down what non-trucking liability insurance actually is. NTL is a separate commercial insurance policy designed to protect you and your drivers when a truck is being used for purposes that fall outside of active business operations. Think of it as the coverage that kicks in during the hours and activities your primary policy simply doesn’t touch.

When your driver takes a company truck home for the weekend, makes a personal grocery run, or visits a mechanic for routine maintenance on personal time, none of those trips are covered under a standard primary liability policy. NTL covers third-party bodily injury and property damage when a commercial truck is not under dispatch, meaning personal use. The moment you’re no longer moving freight for a customer or operating under a motor carrier’s authority, your primary policy is essentially inactive.

Many fleet managers confuse NTL with bobtail insurance. These are related but distinct products, and mixing them up can leave real coverage gaps on the table. The table below clarifies the differences:

| Coverage type | When it applies | What it covers |

|---|---|---|

| Primary liability | Active haul, under dispatch | Third-party injury and property damage during business operations |

| Non-trucking liability (NTL) | Off-duty, personal use, not under dispatch | Third-party injury and property damage during personal trips |

| Bobtail insurance | Driving without a trailer, any time | Third-party claims when operating without a trailer, on or off dispatch |

| Physical damage | Any time the truck is damaged | Collision, fire, theft, and weather damage to your own truck |

Understanding where each policy begins and ends is critical. You can explore liability coverage explained in detail to build a clearer picture of how these layers interact. Common off-duty scenarios that trigger NTL coverage include a driver running personal errands on a Saturday morning, moving a truck between locations that isn’t tied to a dispatched load, or a truck being parked at a driver’s home overnight and used briefly for a personal trip before returning to work routes. Each of these scenarios represents a real exposure that your primary policy won’t address.

For a broader view of coverage requirements, it also helps to review insurance for trucking companies so you can see NTL within the full landscape of required policies.

Why fleet managers and owners can’t ignore off-duty risk

With the basics down, it’s critical to understand why NTL isn’t optional for most fleets. Off-duty accidents may seem unlikely or low-stakes compared to highway collisions during active hauls, but the legal and financial consequences can be just as severe. A driver who causes a fender-bender in a parking lot on a Saturday, while operating your company truck for personal reasons, can easily result in a lawsuit naming your business.

Consider a concrete scenario: your driver borrows the truck over a long weekend to move some furniture. A simple lane-change incident causes minor injuries to another driver. Without NTL, your business faces the full cost of legal defense, settlement, and any damages awarded, because your primary liability policy will deny the claim as soon as it’s established the truck wasn’t under dispatch. That single incident, even without serious injuries, can cost tens of thousands of dollars in legal fees alone.

For fleet managers and small business owners, NTL protects assets by preventing personal liability from off-duty accidents and ensures lease compliance. Many owner-operators and fleet managers don’t realize that leasing companies often require NTL as part of the lease contract, sometimes even for trucks that are parked and not actively moving. A parked truck that rolls into another vehicle in a lot and causes damage still creates a liability event, and your lease may require NTL to cover exactly that.

Being unaware of these trucking insurance mistakes is one of the fastest ways to damage both your finances and your business reputation. Missing a required NTL clause in your lease can also trigger contract violations, potentially jeopardizing your leasing arrangement altogether.

“A single off-duty accident without proper NTL coverage can expose your business to six-figure legal costs, contract violations, and damaged relationships with leasing partners.”

Pro Tip: Keep a simple driver log for any personal use of company trucks. Recording dates, times, and trip purposes creates a clear audit trail that can significantly reduce disputes if a claim arises and your insurer needs to verify the vehicle’s status at the time of an incident.

Understanding the full spectrum of liability coverages for fleets is the most proactive step you can take to close gaps before they cost you.

How non-trucking liability fits your risk management strategy

Having illustrated the dangers, let’s look at where NTL fits into your overall risk management plan amid industry-wide premium hikes. Risk management in trucking isn’t a single policy purchase; it’s a layered system where each coverage type handles a specific type of exposure. NTL occupies a specific and critical layer in that system.

A sound fleet risk management approach typically looks like this: primary liability handles active haul operations, physical damage coverage protects the truck itself from collisions and weather events, cargo insurance protects the freight you’re moving, and NTL fills the off-duty personal use gap. Without NTL, your coverage has a hole in it regardless of how well you’ve built out the other layers.

The financial stakes for ignoring this layer are growing. Trucking insurance costs rose 3% to 10.2 cents per mile in 2024, driven by nuclear verdicts (extremely large jury awards) and higher repair costs. Adding NTL to your portfolio helps manage the off-duty portion of your exposure without dramatically increasing your overall spend.

The longer-term trend is equally sobering. Industry-wide liability premiums are up 36% per mile over the last eight years, even as crash rates have declined. That means the cost of a claim, not just the frequency, is what’s driving premiums higher. Targeted coverage like NTL is a smarter response than simply absorbing these increases without adjusting your coverage strategy.

| Coverage component | Primary purpose | Annual cost range (estimate) |

|---|---|---|

| Primary liability | Active haul operations | $8,000 to $15,000+ per truck |

| Physical damage | Truck repairs, collision, theft | $1,500 to $4,000 per truck |

| Cargo insurance | Freight value protection | $400 to $1,500 per shipment type |

| Non-trucking liability | Off-duty personal use | Under $1,000 per truck |

To understand why increasing insurance rates are reshaping fleet strategies, review current market dynamics in your region. The right mix of coverage doesn’t just protect you from losses; it also positions your business better when it’s time to renew.

Pro Tip: Bundling NTL with your primary liability or physical damage policy through the same insurer often results in a meaningful discount. Always ask your broker or online platform whether multi-policy pricing applies before purchasing NTL as a standalone product.

Reviewing the key insurance premiums factors that affect your rates helps you make smarter bundling decisions and control total fleet insurance costs over time.

Non-trucking liability: Cost, compliance, and real-world benefits

Let’s close the loop by making it practical: what you’ll actually pay, how it keeps your business compliant, and how to put coverage in place faster. One of the most common reasons fleet managers hesitate to add NTL is cost uncertainty, so let’s address that directly.

NTL is cost-effective at under $1,000 per year, and in many cases bundling it with existing coverage brings that figure even lower. For a coverage category that protects you from lawsuits that could reach six figures, the premium is modest by any measure. Final pricing depends on several factors including your geographic location, the driver’s record, the number of vehicles, and whether you bundle it with other policies. Trucks operated in high-traffic urban areas typically carry slightly higher NTL premiums than those in rural regions.

On the compliance side, most lease agreements specifically require NTL as a condition of the contract. Failing to carry it doesn’t just leave you financially exposed; it can also put you in technical default of your lease. Some motor carriers and leasing companies conduct periodic insurance audits, and a missing NTL policy can trigger penalties or contract termination. Reviewing your lease carefully for insurance requirements before signing is always a sound practice.

The real-world benefits of NTL extend beyond legal protection. When a claim is filed and your NTL policy responds, the insurer handles investigation, legal defense, and any settlement negotiations on your behalf. That means you stay focused on running your business rather than managing a lawsuit. For a small fleet operation without in-house legal staff, that benefit alone justifies the annual premium.

To get NTL coverage in place, follow these practical steps. First, assess your exposure by reviewing how and when your drivers use company trucks outside of active dispatch. Second, request quotes from multiple insurers using a platform that gives you side-by-side comparisons rather than a single-provider view. Third, evaluate whether bundling NTL with your existing coverage provides a cost advantage. Fourth, review your lease and any regulatory contracts to confirm the minimum coverage limits required. Fifth, purchase the policy and document it immediately for your lease file and any upcoming renewals.

Rates vary significantly by state, so checking insurance rates by state before you finalize your purchase helps you benchmark what you should be paying and identify whether a quote is competitive for your market.

The truth insurance agents don’t tell fleets about off-duty coverage

Beyond the basics, here’s what we’ve seen trip up even seasoned operators and where the real exposure lies. Most experienced fleet managers understand the mechanics of primary liability. What surprises them, consistently, is discovering that off-duty exposure is not just an edge case; it’s a regular, recurring risk that their policies have never addressed.

Here’s an uncomfortable reality: most agents leading with primary liability policies don’t bring up NTL unprompted. It’s not always bad faith; it’s often because the conversation stays focused on what happens during a haul. But that framing creates a blind spot. The moment your driver’s shift ends and he pulls into his driveway in your truck, your primary liability is off. Full stop.

What makes this especially dangerous is how lease language is written. Many lease clauses don’t differentiate clearly between “active dispatch” and “moving the truck for any reason.” That ambiguity means even a brief, unscheduled truck movement that seems routine to you could be classified by your carrier or lessor as a non-covered off-duty event. One minor incident in that gray zone, and you’re handling it out of pocket while also potentially violating your lease terms.

We’ve seen operators face six-figure outcomes from weekend accidents that involved no injuries beyond moderate whiplash to one other driver. Legal fees, lost time, lease complications, and settlement costs compounded rapidly. The NTL premium that would have covered it entirely cost less than a single monthly truck payment.

The proactive step is to get insurance explained for trucking from an advisor who maps your coverage to your actual operations, not just the standard checklist. Don’t wait for a claim to discover where your policies stop and your exposure begins.

Protect your fleet: Affordable, trusted non-trucking liability options

Ready to shield your business for good? Here are practical next steps to secure your fleet and peace of mind.

At Diamondback Insurance, we make it straightforward to compare NTL quotes from multiple top-rated insurers in minutes. You don’t need to navigate multiple brokers or wait days for callbacks. Our platform gives you instant, transparent pricing so you can make a confident decision quickly.

Whether you’re adding NTL for the first time or reviewing your current fleet coverage to close gaps, we’re here to help you build a policy stack that matches your real-world operations. You can start with a quick overview of more on trucking insurance to confirm your coverage foundation is solid, then compare top fleet coverages to see how NTL fits alongside your existing policies. Protecting your fleet shouldn’t be complicated, and with the right tools, it doesn’t have to be.

Frequently asked questions

What does non-trucking liability insurance actually cover?

Non-trucking liability insurance covers third-party bodily injury and property damage when a truck is used for personal, non-business purposes, not business hauling. It activates when the driver is off dispatch and using the truck outside of active freight operations.

Is non-trucking liability required by law or contract?

While NTL is not always a federal legal requirement, most lease agreements demand NTL for compliance and asset protection. Failing to carry it can constitute a contract default with your leasing partner.

How much does non-trucking liability typically cost?

NTL typically costs under $1,000 per truck annually, and bundling it with primary liability or physical damage coverage can bring the cost down further. It’s one of the most affordable protections relative to the financial risk it addresses.

Why isn’t my primary liability insurance enough?

Primary liability only covers business operations and active dispatch; any off-duty accident exposes you to personal lawsuits that your primary policy will deny. NTL fills that gap directly.

How do rising industry costs affect my need for NTL?

Trucking insurance costs rising to 10.2 cents per mile in 2024 highlight how even targeted gaps in coverage can become very expensive very fast. Adding NTL is a cost-efficient way to address off-duty risk without dramatically increasing your total fleet insurance spend.