Flood damage can financially devastate a property, yet most owners discover too late that liability in flood insurance works very differently from what they expected. Standard homeowners insurance does not cover flood damage caused by water entering from outside at ground level, which means you need a separate flood policy entirely. But even with that policy in hand, the concept of liability gets misunderstood constantly. This article breaks down exactly what flood insurance covers, where liability fits into that framework, how coverage limits affect your exposure, and what steps protect you when a claim actually arrives.

Table of Contents

- Key takeaways

- Liability in flood insurance: what your policy actually covers

- Procedural requirements and flood liability claims

- Coverage limits and excess flood insurance policies

- Common disputes in flood liability claims

- Practical steps to manage flood liability risks

- My honest take on flood insurance liability

- Protect your property with the right coverage today

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Flood insurance is separate | Standard homeowners insurance excludes flood damage; you need a dedicated flood policy to cover water losses. |

| Liability in flood insurance means financial responsibility | Flood insurance liability refers to your policy’s financial obligation for flood damage, not third-party injury claims. |

| Procedural deadlines decide claims | Missing the 60-day proof of loss deadline can void your claim even when flood damage is obvious and severe. |

| NFIP limits leave gaps | Coverage caps at $250,000 for buildings and $100,000 for contents, leaving high-value properties underinsured. |

| Excess flood policies fill those gaps | Excess flood insurance activates after NFIP limits are exhausted, protecting properties that exceed standard caps. |

Liability in flood insurance: what your policy actually covers

Before you can protect your property effectively, you need to understand what flood insurance covers and where liability enters the picture. FEMA explains that flood insurance helps policyholders recover after floodwaters recede by covering building structure damage and personal contents. That sounds straightforward, but the liability element is where most homeowners get confused.

Liability in flood insurance does not mean the same thing as liability in a standard homeowners policy. In a homeowners policy, liability coverage protects you if someone is injured on your property. In a flood policy, liability refers to the financial responsibility your insurer accepts for flood damage losses up to your policy limits. There is no third-party bodily injury component in a standard NFIP flood policy. You need to keep that distinction clear when reviewing your coverage.

What flood insurance does cover breaks down into two main categories:

- Building coverage: Structural elements including walls, floors, foundation, electrical systems, plumbing, HVAC equipment, and major appliances permanently installed in the home

- Contents coverage: Personal belongings such as clothing, furniture, electronics, and portable appliances, typically purchased as a separate add-on

Homeowners insurance excludes flood damage caused by water entering from outside at or below ground level. That exclusion is deliberate. It concentrates flood risk into dedicated flood insurance programs so that each policy type addresses the risks it was designed to handle. Understanding that boundary is the foundation of sound flood damage liability planning.

Pro Tip: Purchase building and contents coverage together. Many homeowners buy only building coverage and then discover their belongings have no protection after a flood. Both components are purchased separately under NFIP, so confirm your policy includes both.

Replacement cost versus actual cash value also matters here. NFIP pays replacement cost for building damage on single-family homes when you insure to at least 80% of the building’s replacement cost. Contents, however, are almost always paid at actual cash value, which accounts for depreciation. That difference can significantly reduce your recovery on older belongings.

Procedural requirements and flood liability claims

Understanding the coverage is only part of the equation. How you file your claim determines whether you actually collect on it, and the rules governing flood liability claims are strict.

NFIP policies operate under the Standard Flood Insurance Policy, or SFIP. This policy framework carries firm procedural obligations that the courts enforce without sympathy for good-faith mistakes. The most consequential requirement is the proof of loss deadline.

- You must notify your insurer promptly after flood damage occurs

- You must submit a signed and sworn proof of loss within 60 days of the flood event

- The proof of loss must document all claimed damages in precise detail, including amounts for each category of loss

- You must cooperate fully with the insurer’s adjuster and provide access to the property

- You must preserve the statute of limitations window, typically one year from denial of the claim, to file suit if your claim is disputed

Missing the signed proof of loss deadline can result in complete denial of your claim, regardless of how severe or obvious the flood damage is. Courts have consistently held insurers to this strict enforcement standard. This is not a technicality that gets waived because you had a good reason for the delay.

“The proof of loss is the backbone of the claim file. Missing information or a missed deadline can jeopardize coverage regardless of damage severity.” — SFIP claims guidance

Strict deadline compliance often decides claim outcomes more than the underlying flood damage itself. That reality is hard to accept, but it is how flood insurance liability claims actually work in practice. Your job as a policyholder is to treat the paperwork with the same urgency you give the physical repairs.

After a flood event, start documenting immediately. Photograph everything before moving or discarding damaged items. Keep all receipts for emergency repairs you make to prevent further damage. Create a written inventory of every damaged item with estimated values. These records form the evidentiary foundation of your proof of loss submission.

Coverage limits and excess flood insurance policies

Once you understand how flood insurance liability works procedurally, the next critical issue is whether your coverage limits are actually adequate for your property’s value.

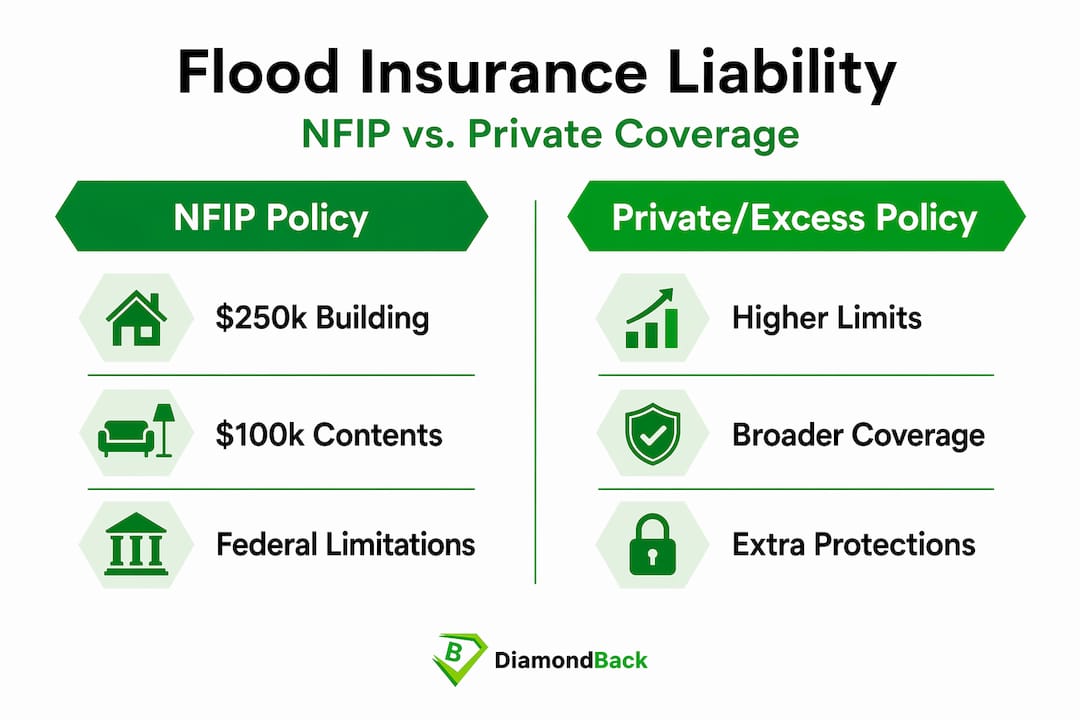

NFIP coverage is capped at $250,000 for residential building coverage and $100,000 for contents. For many homeowners, especially those in coastal areas or high-value markets, those limits fall well short of actual property value. A custom-built home worth $700,000 carries $450,000 in uncovered exposure under NFIP limits alone.

The table below illustrates the coverage gap that excess flood insurance addresses:

| Coverage type | Maximum limit | Typical use case |

|---|---|---|

| NFIP building coverage | $250,000 | Primary residence with moderate rebuild cost |

| NFIP contents coverage | $100,000 | Standard household belongings |

| Excess flood insurance | Negotiated with private insurer | High-value homes, investment properties, large contents |

| Private flood policy | Varies by insurer | Additional living expenses, broader definitions |

Excess flood insurance pays only after NFIP limits are fully exhausted, functioning as a second layer of financial protection. You typically carry both policies simultaneously. The NFIP policy responds first up to its cap, and the excess policy activates for any remaining covered loss above that threshold. Examples of excess flood policies often cover the same perils as the underlying NFIP policy but extend the dollar ceiling to match your property’s full replacement cost.

Private flood insurance policies, purchased outside the NFIP entirely, can offer features that NFIP excludes. These may include additional living expense coverage while your home is uninhabitable, broader basement coverage, and faster claims processing. For property managers overseeing multiple rental units, private flood options deserve serious evaluation.

Pro Tip: If your home’s rebuild cost exceeds $250,000, request a separate excess flood quote from a private insurer before your next renewal. The premium difference is usually far smaller than the coverage gap you are currently carrying.

Excess flood coverage is a recognized tool for homeowners with properties valued above NFIP caps. Yet a surprisingly large portion of high-value property owners never purchase it. The result is a significant and entirely preventable financial exposure sitting unaddressed inside their property portfolio.

Common disputes in flood liability claims

Even when you file on time and document thoroughly, disputes can arise. Some of the most consequential involve how your property is classified within the policy’s definitions.

A real-world example from Hurricane Helene illustrates this sharply. A flood claim dispute over basement classification turned on whether a below-grade space qualified as a “basement” under SFIP definitions. NFIP covers basements at a much more limited level than above-grade living spaces. If your insurer classifies a finished lower level as a basement, your liability recovery for that space drops dramatically.

These classification disputes are more common than most homeowners realize:

- Basement versus non-elevated space: Below-grade rooms classified as basements receive only limited coverage for specific mechanical systems, not for finished walls, flooring, or personal property stored there

- Manufactured versus standard construction: Different construction classifications affect both premiums and claim payouts under flood insurance limits

- Primary residence versus secondary property: Occupancy classification changes how contents claims are processed and valued

- Residential versus mixed-use buildings: Properties with a commercial element may face different coverage rules under NFIP than pure residential structures

Technical policy definitions such as basement classification can be the deciding factor in dispute resolution for liability claims. The lesson is not to wait until after a flood to understand how your property is classified. Review your declarations page now, confirm your building type and occupancy classification with your agent, and ask direct questions about how any below-grade space in your home is defined under your current policy.

Good documentation discipline also reduces your exposure in disputes. Keep dated photographs of your property’s condition before any flood event occurs. Maintain receipts for major purchases and home improvements. Store those records somewhere off-site or in cloud-based storage so a flood cannot destroy the evidence you need to support your claim.

Practical steps to manage flood liability risks

Knowing the coverage structure matters, but consistent action is what actually protects your assets when a flood happens.

- Review your flood policy annually. Confirm your coverage limits still reflect your property’s current replacement cost. Home values and rebuild costs change, and your policy should keep pace with those changes.

- Account for NFIP’s 30-day waiting period. New flood policies require a 30-day waiting period before coverage takes effect, with limited exceptions. You cannot purchase coverage the week before a named storm and expect it to be active.

- Document everything before and after a flood. Pre-flood photos and inventories give you a baseline. Post-flood documentation supports your proof of loss and strengthens your position if a dispute arises.

- Purchase excess flood insurance if your property value exceeds NFIP limits. This applies especially to property managers overseeing multi-unit buildings or homeowners in high-value coastal markets.

- Work with a licensed insurance professional for complex properties. Multi-family buildings, mixed-use properties, and historic homes involve classification and valuation issues that benefit from expert guidance.

Pro Tip: Set a calendar reminder three months before your flood policy renewal date. That gives you enough time to get competing quotes, evaluate whether your limits are still adequate, and make changes without rushing.

You can also explore flood insurance coverage options for properties with more complex needs, including structures where both physical assets and operational continuity are at risk from flood damage. Understanding the full range of available options helps you make genuinely informed coverage decisions rather than simply accepting whatever your current policy provides.

My honest take on flood insurance liability

I have reviewed enough flood insurance situations to know that most homeowners dramatically underestimate how much procedural discipline drives claim outcomes. People focus on the coverage question, which is natural. They want to know what is covered. But the coverage question matters far less than the compliance question when a real claim arrives.

I have seen well-documented flood losses get denied because the proof of loss arrived on day 62 instead of day 60. That is not an edge case. That is how the SFIP is designed to work, and the courts enforce it consistently. The 60-day deadline is not a guideline. It is the rule.

My other consistent observation is that excess flood insurance is treated as optional by most homeowners who genuinely need it. If your home would cost more than $250,000 to rebuild, you are self-insuring the difference every day you carry only an NFIP policy. That is a deliberate financial decision most people are making without realizing they made it.

The classification issue also deserves more attention than it gets. Knowing that your finished lower level might be treated as a basement under flood insurance definitions, before a flood, gives you time to ask questions, explore private flood alternatives, or at minimum understand your real exposure. Finding out after water fills that space is a painful way to learn about policy definitions.

My honest recommendation: treat your annual flood policy review the same way you treat any other significant financial obligation. Read the declarations page. Confirm the limits. Ask about your property classification. Understanding liability coverage across all your policies is a discipline that pays off directly when you actually need to file a claim.

— Vladimir

Protect your property with the right coverage today

At Diamondbackins, we understand that securing the right protection for your property requires more than a generic policy. Whether you manage a single-family home or a portfolio of rental properties, the gap between what standard flood insurance covers and what your property is actually worth can represent serious financial exposure. Diamondbackins gives you fast access to tailored insurance quotes from multiple top-rated carriers, so you can compare options and confirm your coverage matches your real needs. Take a few minutes today to get an insurance quote online and make sure your coverage is genuinely working for you. If you are in Georgia and want coverage tailored to your specific market, Georgia property protection is available through Diamondbackins right now.

FAQ

What does liability mean in flood insurance?

Liability in flood insurance refers to the financial responsibility your policy accepts for covered flood damage losses, not third-party injury claims. Unlike homeowners insurance, flood policies do not include personal liability coverage for injuries to others on your property.

What are the NFIP flood insurance limits?

NFIP coverage caps at $250,000 for residential building damage and $100,000 for contents. Properties valued above these thresholds need excess flood insurance to cover the remaining exposure.

What happens if I miss the proof of loss deadline?

Missing the 60-day proof of loss deadline under the SFIP can result in complete denial of your flood claim, regardless of how clear or severe the damage is. Courts consistently uphold this enforcement standard.

What is excess flood insurance and when do I need it?

Excess flood insurance extends your coverage beyond NFIP limits and pays after your primary NFIP policy is exhausted. You need it when your property’s replacement cost or contents value exceeds the NFIP caps.

Does flood insurance cover my basement?

NFIP flood insurance covers basements only for specific mechanical and utility systems, not for finished walls, flooring, or personal property stored there. If your below-grade space is classified as a basement, your claim recovery for that area will be significantly limited.

Recommended

- Flood insurance coverage options for your business and fleet

- Safeguarding Your Voyage Boat Insurance in the Hurricane Zone – Diamondback Insurance – Solutions with Instant Online Quotes

- Navigating Through the Storm Understanding Boat Insurance in the Hurricane Box – Diamondback Insurance – Solutions with Instant Online Quotes

- Types of liability coverage: protect your fleet and business