Blanket insurance is defined as a single policy that covers multiple properties, buildings, or assets under one shared aggregate limit. Unlike a scheduled policy, which assigns a fixed dollar cap to each individual location or item, a blanket insurance policy pools the entire coverage limit across all insured assets. That pooling arrangement means a major loss at one location can draw on the full limit rather than being capped at a site-specific ceiling. For property owners managing more than one building, a fleet of vehicles, or a mix of equipment and inventory, understanding how blanket coverage works is the first step toward protecting your full portfolio.

What is blanket insurance and how does it work?

Blanket insurance pools multiple properties or assets under a single aggregate limit, allowing the full limit to respond to a loss at one location. That is the core mechanic that separates it from a scheduled policy, where each site carries its own sublimit. If you own three warehouses and one burns down, a blanket policy lets you apply the entire coverage limit to that single loss. A scheduled policy would cap your recovery at whatever limit was assigned to that specific warehouse.

The aggregate limit works like a shared pool. All your insured properties draw from the same bucket, and the insurer pays claims from that bucket regardless of which location suffers the loss. This flexibility is especially valuable when your properties have unequal values or when asset values shift over time.

Coinsurance requirements are stricter under blanket coverage than under basic scheduled policies. Blanket policies typically require at least 90% to 100% coinsurance on total portfolio value to avoid penalties. That means your blanket limit must equal at least 90% of the combined replacement value of all covered assets. Falling short triggers a proportional reduction in any claim payout.

Margin clauses add another layer of complexity. Margin clauses limit insurer payouts to a percentage above the declared value of individual assets, typically 110% to 125% of the declared value per site. Even if your blanket limit is large, the insurer will not pay more than that margin percentage above what you declared for a specific location. Policyholders who under-declare individual asset values can face coverage gaps even under a generous blanket limit.

Pro Tip: Ask your insurer to define the margin clause percentage in writing before binding a blanket policy. A 110% margin on a property you declared at $500,000 caps your recovery at $550,000, regardless of the actual replacement cost.

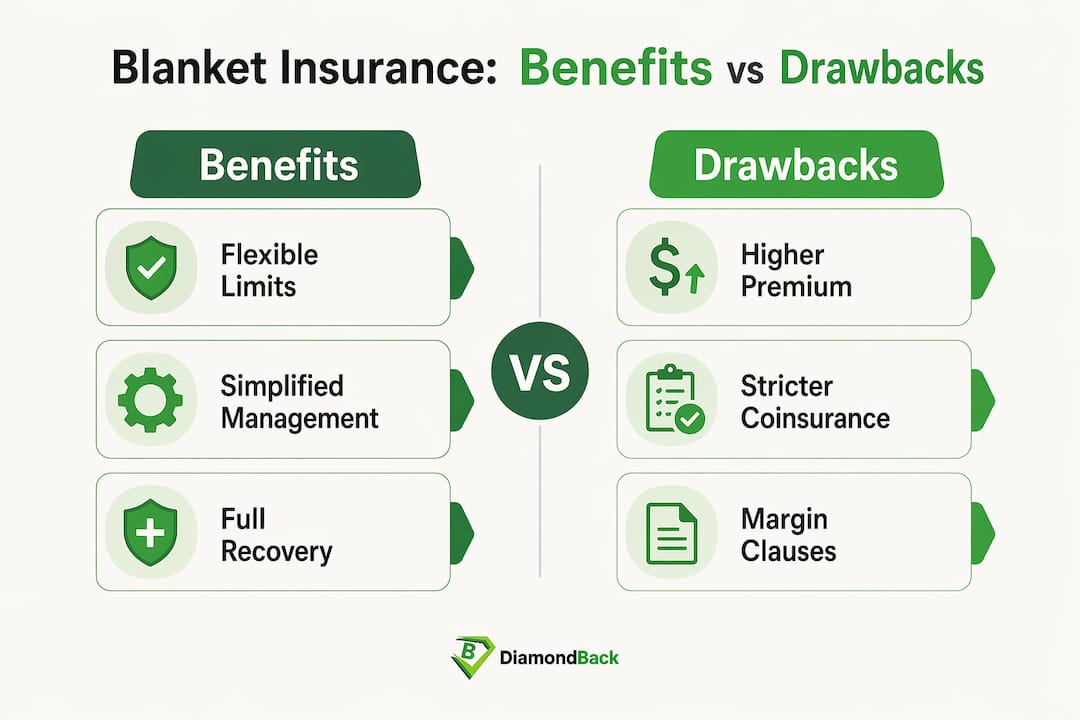

What are the benefits and drawbacks of blanket coverage?

Blanket insurance delivers three clear advantages over scheduled policies: flexible limit allocation, simpler administration, and protection against underinsurance at any single location.

The flexibility benefit is the most significant. The strategic value of blanket coverage is eliminating the risk of being underinsured at one location while holding surplus coverage at another. With a scheduled policy, excess coverage at Location A cannot help you at Location B. A blanket policy removes that barrier entirely.

Administration also becomes simpler. Risk managers choose blanket insurance for simplification and unified oversight, reducing the paperwork burden of maintaining separate limits and endorsements for each asset. For property owners with five or more locations, that administrative relief has real dollar value in staff time and policy management costs.

The drawbacks are real and worth understanding before you commit.

-

Higher premiums. Blanket insurance usually carries higher premiums than scheduled policies because the insurer absorbs broader risk exposure across the entire portfolio. The flexibility you gain comes at a cost.

-

Strict valuation requirements. You must maintain an accurate Statement of Values (SOV) listing every covered asset and its current replacement cost. Outdated valuations create coinsurance penalties that reduce your claim payment.

-

Margin clause exposure. Under-declaring individual asset values to save on premiums can backfire when a claim is filed. The margin clause will cap your recovery below actual replacement cost.

-

Complexity in mixed portfolios. Blanket policies covering both real property and personal property require careful structuring to avoid coverage gaps between asset categories.

“Clients are often surprised by higher premiums under blanket policies, but the flexibility of a pooled coverage limit frequently justifies the added cost when a major loss occurs at a single location.”

The right question is not whether blanket insurance is expensive. The right question is whether the cost of a coverage gap at your most valuable location exceeds the premium difference. For most multi-property owners, it does.

What types of blanket insurance policies are available?

Blanket insurance is not a standalone policy type. It is a structural approach that can be applied across several categories of commercial and personal property coverage.

The most common types include:

- Blanket building coverage. A single limit covers multiple structures at different addresses. This suits landlords, real estate investors, and businesses operating from several owned or leased buildings.

- Blanket personal property coverage. Inventory, equipment, and furnishings across multiple locations share one limit. Retailers with several storefronts and manufacturers with multiple production sites use this structure frequently.

- Blanket equipment coverage. Construction firms and transportation companies use blanket limits to cover machinery and vehicles that move between job sites or terminals. This is where blanket coverage aligns closely with cargo insurance protections for fleets moving goods across locations.

- Combined blanket limits. Some policies cover both buildings and personal property under one shared limit, which simplifies coverage for mixed-asset portfolios.

Blanket coverage also fits within Business Owner’s Policies (BOP) and commercial package policies. A BOP with a blanket limit gives small business owners unified protection without managing separate endorsements for each location or asset class. For transportation and logistics operators, blanket coverage works well for assets that frequently move between terminals, depots, and customer sites. An insured container haulage operation, for example, benefits from blanket coverage across locations because the assets rarely stay in one place long enough to justify fixed site-specific limits.

Individuals with two or more investment properties also benefit from blanket coverage. A landlord owning four rental homes in different zip codes can insure all four under one blanket limit rather than managing four separate policies with four separate renewal dates and four separate premium payments.

How do you maintain and optimize blanket insurance coverage?

Maintaining a blanket policy correctly requires discipline around three areas: coinsurance compliance, Statement of Values accuracy, and margin clause management.

Coinsurance compliance starts with knowing your total portfolio replacement value. Your blanket limit must meet the coinsurance threshold, which requires at least 90% to 100% of total portfolio value in 2026. Review your portfolio value annually, especially after acquiring new assets, completing renovations, or experiencing significant market value changes.

The Statement of Values is your policy’s foundation. Undervaluing assets to save premiums can trigger coinsurance penalties and drastically reduce claim payouts. Update your SOV every time you add a property, dispose of an asset, or complete a capital improvement. Many insurers require an updated SOV at renewal, but waiting until renewal is too late if a loss occurs mid-term.

| Maintenance Task | Frequency | Purpose |

|---|---|---|

| Update Statement of Values | Annually or after any asset change | Maintain coinsurance compliance |

| Review blanket limit vs. portfolio value | Annually | Prevent underinsurance penalties |

| Confirm margin clause percentages | At renewal | Avoid site-specific coverage gaps |

| Request Agreed Value endorsement review | Every 2–3 years | Suspend coinsurance requirement for volatile assets |

| Coordinate with insurance agent on new acquisitions | Immediately upon acquisition | Add assets before a loss occurs |

An Agreed Value endorsement is the most effective tool for volatile asset portfolios. An Agreed Value endorsement suspends the coinsurance requirement entirely, preventing penalties when the total agreed value matches the blanket limit. This endorsement is especially useful for fleets and equipment-heavy operations where replacement costs fluctuate with market conditions.

Pro Tip: Request an Agreed Value endorsement at every renewal if your portfolio includes assets with rapidly changing replacement costs, such as commercial vehicles or specialized equipment. It eliminates the coinsurance penalty risk without requiring a higher blanket limit.

For fleet managers and transportation operators, coordinating blanket coverage with your fleet insurance workflow ensures that every vehicle and piece of equipment is accounted for in the SOV before a loss occurs.

Key Takeaways

A blanket insurance policy provides the most reliable protection for multi-property portfolios when coinsurance requirements are met, valuations are current, and margin clauses are clearly understood.

| Point | Details |

|---|---|

| Pooled aggregate limit | One shared limit covers all locations, allowing full recovery at any single site. |

| Coinsurance threshold | Blanket policies require 90%–100% of total portfolio value to avoid claim penalties. |

| Margin clause awareness | Insurers cap site-specific payouts at 110%–125% above declared value per location. |

| Statement of Values accuracy | Outdated or underreported valuations trigger proportional reductions in claim payments. |

| Agreed Value endorsement | Suspending coinsurance requirements protects volatile asset portfolios from penalty risk. |

Why blanket insurance rewards the property owner who pays attention

I have worked with property owners who chose blanket coverage for the right reasons and then let the policy drift. They added a building, skipped the SOV update, and discovered the gap only when a claim was filed. The insurer applied the coinsurance penalty, and the recovery was thousands of dollars short of what the owner expected.

The policy itself was not the problem. The discipline around maintaining it was. Blanket insurance rewards owners who treat the Statement of Values as a living document, not a form they fill out once at inception. The flexibility of a pooled limit is genuinely valuable. That value disappears the moment your declared values fall out of step with reality.

The other mistake I see consistently is treating the blanket limit as a ceiling rather than a pool. Owners sometimes reduce their blanket limit to cut premiums, not realizing they are pushing themselves below the coinsurance threshold. The premium savings are real. The coinsurance penalty at claim time is also real, and it is usually larger. Evaluate your portfolio risk as a whole, not location by location. The entire point of blanket coverage is that your total exposure matters more than any single site’s value.

— Vladimir

Commercial coverage built for your portfolio

Property owners and fleet operators who understand blanket insurance know that the right policy structure is only half the equation. The other half is finding coverage that matches your actual portfolio at a price that makes sense.

Diamondbackins specializes in commercial and transportation insurance, giving you instant access to quotes from multiple top insurers without the back-and-forth of traditional brokers. Whether you manage a fleet of commercial trucks or a portfolio of properties, you can compare options and secure coverage in minutes. Explore commercial trucking insurance in Georgia or get a fleet insurance quote tailored to your operation. Diamondbackins puts the right coverage within reach, fast.

FAQ

What is blanket insurance in simple terms?

Blanket insurance is a single policy that covers multiple properties or assets under one shared limit. A loss at any covered location can draw on the full policy limit rather than a fixed site-specific cap.

How does blanket insurance differ from scheduled insurance?

A scheduled policy assigns a separate coverage limit to each individual asset or location. A blanket policy pools one aggregate limit across all covered assets, providing more flexibility when a major loss occurs at one site.

What does blanket insurance typically cover?

Blanket coverage applies to buildings, personal property, inventory, equipment, and vehicles across multiple locations. It is commonly used in commercial property, fleet, and mixed-asset portfolio policies.

Is blanket insurance worth the higher premium?

Blanket insurance carries higher premiums than scheduled policies, but the pooled limit eliminates the risk of being underinsured at your most valuable location. For owners with three or more properties or assets of unequal value, the protection typically justifies the added cost.

What is a coinsurance requirement in a blanket policy?

A coinsurance requirement means your blanket limit must equal at least 90% to 100% of your total portfolio’s replacement value. Falling below that threshold triggers a proportional reduction in any claim payout, which can significantly reduce your recovery after a loss.

Recommended

- What Is Insurance Exclusions: A Property Owner’s Guide

- Understanding Marine Insurance A Comprehensive Guide by DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- What Is an Insurance Binder? Your Coverage Guide

- What Boat Insurance Do I Need A Guide from DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes