Most homeowners discover a painful truth after the water recedes: their standard homeowners policy did not cover a single dollar of flood damage. This buy flood insurance online guide exists to prevent that situation. Standard homeowners policies explicitly exclude flood damage from external water sources, which means you need a dedicated policy before any storm threatens your property. The good news is that buying flood insurance online is faster and more accessible than ever. You just need to understand your coverage options, how pricing works, and where to avoid common mistakes.

Table of Contents

- Key takeaways

- Your buy flood insurance online guide starts here

- How to buy flood insurance online, step by step

- Common mistakes that cost homeowners coverage

- Managing your policy after purchase

- My honest perspective on buying flood insurance

- Get flood coverage quotes without the guesswork

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Homeowners policies exclude floods | Your standard policy will not pay for flood damage; a separate flood policy is required. |

| Two main coverage paths exist | You can choose between federally backed NFIP coverage or a private flood insurance policy. |

| Waiting periods affect timing | NFIP policies require 30 days before coverage activates, so early purchase matters greatly. |

| Price varies by property type | Newer or elevated homes often qualify for lower premiums through private carriers. |

| Annual review protects your investment | Reviewing your policy each year keeps your coverage aligned with your home’s current value. |

Your buy flood insurance online guide starts here

Before you request a single quote, you need to understand what kind of flood insurance you are actually buying. There are two distinct markets, and choosing between them is the most consequential decision in this entire process.

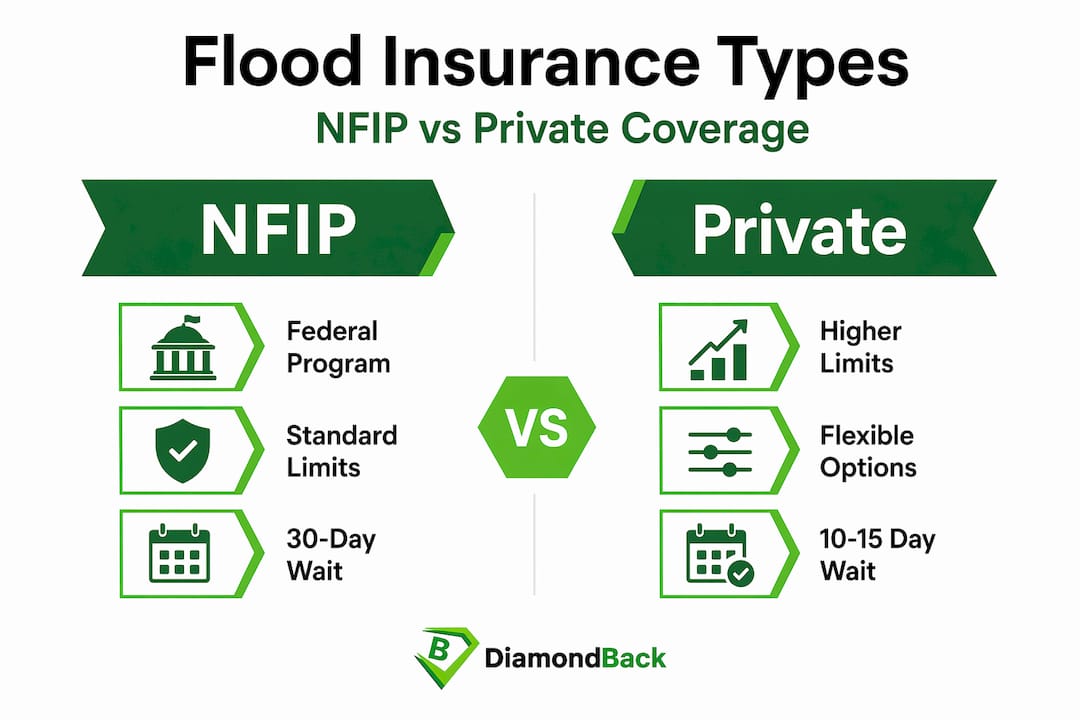

What is the NFIP and who is it for?

The National Flood Insurance Program, commonly called the NFIP, is a federal program administered by FEMA. It is the most widely known option and is available to homeowners in participating communities across the country. The NFIP caps building coverage at $250,000 and personal property coverage at $100,000, which works fine for modest homes but falls short for higher-value properties. One major factor to plan around is the waiting period. NFIP policies require 30 days before coverage becomes effective, which means you cannot buy a policy the week before a hurricane and expect it to help you.

How private flood insurance compares

Private flood insurance is underwritten by independent carriers rather than the federal government. These policies frequently offer coverage limits ranging from $1 million up to $10 million or more, which makes them a practical necessity for higher-value homes. Private carriers also move faster. Most private policies carry waiting periods of just 10 to 14 days, giving you more flexibility if your timeline is tight. For pricing, the NFIP national average runs about $926 per year while private policies average around $1,140 annually. That said, private flood insurance is cheaper roughly 60% of the time for newer or elevated homes, so newer construction should always compare both markets before deciding.

Understanding coverage elements

Both NFIP and private policies generally cover two broad categories. Building coverage protects the structure itself, including your foundation, electrical systems, HVAC equipment, and permanently installed fixtures. Contents coverage protects your personal belongings such as furniture, clothing, and appliances. Where private policies often pull ahead is in offering additional living expenses coverage, which pays for temporary housing while your home is being repaired. NFIP policies do not include this benefit by default, which can be a significant gap for families facing long repair timelines.

One more distinction worth understanding is replacement cost versus actual cash value. Replacement cost coverage reimburses the full cost of rebuilding your damaged property at today’s prices, while actual cash value coverage subtracts depreciation from that number. The difference on a 15-year-old roof or floor system can be thousands of dollars. Whenever possible, prioritize replacement cost coverage in your policy.

You can review how these flood coverage options compare for both residential and commercial properties to get a clearer picture of what each approach covers.

How to buy flood insurance online, step by step

Once you understand the types of coverage available, the online purchase process itself is straightforward if you approach it methodically.

Step 1: Gather your property information. You will need your property address, your current flood zone designation, and ideally an elevation certificate if your home has one. Flood zone designations are available through FEMA’s Flood Map Service Center. An elevation certificate, prepared by a licensed surveyor, documents your home’s elevation relative to the base flood elevation and can meaningfully lower your premium, particularly with NFIP.

Step 2: Get quotes from both markets. Do not limit yourself to one option. Use FEMA’s official NFIP resources to understand federal rates, and then request quotes from private carriers as well. Because flood quotes vary dramatically based on different flood models and underwriting rules used by each carrier, the same property can receive very different pricing from different insurers.

Step 3: Compare coverage details, not just price. Two quotes at similar price points can have very different deductibles, coverage limits, and exclusions. Look specifically at whether contents coverage is included, whether additional living expenses are covered, and what the deductible amount is for both building and personal property components.

Step 4: Work with a licensed agent virtually. Many online platforms allow you to consult with a licensed agent by phone, chat, or video without ever visiting an office. Independent agents who compare both NFIP and private markets side by side give you the most objective view of your options. They can clarify policy language and help you avoid coverage gaps that are easy to miss when reading documents on your own.

Step 5: Understand your effective date before you finalize. Confirm the waiting period for the policy you are purchasing. If you are buying an NFIP policy, your coverage will not activate for 30 days. Plan purchases well ahead of storm season, typically before May or June, to avoid any gap in protection.

Step 6: Complete the application and purchase online. Most insurers allow you to complete the full application, review your policy documents, and make your initial payment entirely online. Save your policy declarations page immediately after purchase. This document summarizes your coverage limits, deductibles, and effective dates in one place.

Pro Tip: If your lender requires flood insurance, confirm the policy meets their minimum coverage requirements before finalizing. Lenders often specify minimum building coverage amounts that differ from what you would choose independently.

Common mistakes that cost homeowners coverage

There are predictable errors that show up repeatedly when homeowners purchase flood insurance online without sufficient preparation. Recognizing these ahead of time protects both your coverage and your money.

The most widespread mistake is assuming your homeowners policy handles floods. This misconception is so common that it catches thousands of families off guard every year. Federal disaster aid is limited and frequently structured as loans that must be repaid rather than grants, meaning relying on government assistance after a flood is a financially dangerous strategy.

Buying based on premium alone is another costly error. A policy with a very low premium might carry a $10,000 deductible or exclude contents coverage entirely. Always read the declarations page of any policy before purchasing, not just the price summary. Two policies priced within $100 of each other annually can have wildly different actual payouts after a loss.

Waiting too long is a mistake that cannot be corrected after the fact. Insurers frequently stop issuing new policies once a storm is approaching, and waiting periods mean even a timely purchase can leave a window of exposure. The homeowners who feel most secure are those who bought their flood coverage months before storm season, not days before a named storm.

Skipping the private market comparison is a particular oversight for owners of newer or elevated homes. If you only check NFIP rates without exploring private carriers, you may be paying significantly more than necessary or settling for lower limits than your property actually requires.

Pro Tip: Before purchasing any flood policy online, verify the provider’s license through your state’s Department of Insurance website. Fraudulent insurance schemes tend to spike after major flood events, targeting homeowners anxious to get coverage quickly.

Managing your policy after purchase

Buying flood insurance online is not a set-it-and-forget-it transaction. The steps you take after purchase are just as important as the purchase itself.

First, read your policy declarations page carefully once it arrives. Confirm that the coverage limits, deductibles, and effective dates match what you were quoted. Errors in insurance documents are uncommon but not impossible, and catching them immediately is far easier than disputing them after a claim.

Second, set up online billing and renewal alerts with your insurer. Most carriers now allow full account management through a web portal, including payment scheduling, document downloads, and coverage change requests. Keeping your billing current prevents accidental lapses in coverage, which can trigger lender-required force-placed insurance at much higher rates.

Third, update your coverage any time you make significant improvements to your home. A finished basement, new HVAC system, or kitchen renovation changes the replacement cost of your property. If your coverage limit does not keep pace with these improvements, you may face a shortfall at claim time.

Fourth, monitor changes to your flood zone designation. FEMA updates flood maps on a rolling basis, and a remapping can move your property into a higher-risk zone, potentially affecting your premium and coverage requirements. Your local government planning office or FEMA’s website can tell you when maps for your area were last revised.

Fifth, schedule a brief annual policy review with your agent or through your insurer’s online platform. Confirm that your limits still reflect current construction costs in your area and that no coverage gaps have developed due to policy changes.

My honest perspective on buying flood insurance

I’ve spent years watching homeowners underestimate flood risk, and the pattern is consistent. People focus on their flood zone designation and conclude they are safe because they are not in a high-risk area. What I’ve learned is that most flood claims actually come from properties outside of designated high-risk flood zones. Flood zone maps are a starting point, not a guarantee.

What I’ve also seen is how damaging the federal disaster aid misconception can be. People genuinely believe the government will step in and cover their losses. In reality, FEMA disaster grants are modest, and loan-based assistance creates new financial obligations on top of existing ones. Flood insurance is the only mechanism that actually replaces what you lose.

My practical advice is this: buy before you think you need to. The waiting period exists specifically to prevent reactive purchases, so the only way to be covered when a storm arrives is to have already been covered before any threat materialized. If you are starting this process today and storm season is approaching, make getting quotes your first priority this week, not next month.

I’d also push back on the idea that shopping online means shopping alone. Use virtual agents. Ask hard questions about what is and is not covered. A ten-minute conversation with a knowledgeable agent has saved homeowners far more than any amount saved by choosing the cheapest option without reading the details.

— Vladimir

Get flood coverage quotes without the guesswork

Finding the right flood insurance policy should not feel like a research project without an endpoint. At Diamondbackins, comparing coverage options is fast, transparent, and guided by people who understand the details that matter.

Whether you are evaluating NFIP versus private flood options or reviewing your current policy limits, Diamondbackins connects you with licensed agents and multiple insurer quotes in one place. You can review your flood insurance options online and get a personalized quote without waiting on hold or visiting an office. The process takes minutes, and the coverage you secure could save you hundreds of thousands of dollars. Take the next step and request your instant quote today.

FAQ

Does homeowners insurance cover flood damage?

No. Standard homeowners policies exclude flood damage from external water sources entirely. You need a separate flood insurance policy to be protected.

How long does it take for flood insurance to go into effect?

NFIP policies have a 30-day waiting period before coverage activates. Private flood insurance typically activates in 10 to 14 days, making it a faster option when time is limited.

Is private flood insurance better than NFIP coverage?

It depends on your property. Private flood insurance offers higher limits and shorter waiting periods, and it is cheaper about 60% of the time for newer or elevated homes. However, NFIP may be more cost-effective for older homes in high-risk flood zones.

What information do I need to get a flood insurance quote online?

You will need your property address, flood zone designation, and basic details about your home such as construction type, year built, and number of floors. An elevation certificate can improve your rate but is not always required to get an initial quote.

Can I buy flood insurance online without an agent?

Yes, many carriers allow fully online applications and purchases. That said, working with a licensed independent agent who can compare NFIP and private markets side by side gives you the best chance of finding the right coverage at the right price.