Two drivers the same age, living two streets apart, can pay dramatically different premiums for identical coverage. That gap isn’t random, and it isn’t unfair. It’s the result of a structured process called insurance rating, where carriers assess dozens of variables to calculate what your specific risk actually costs them to cover. Explaining insurance rating factors clearly is the starting point for every smart coverage decision you’ll ever make. Whether you’re insuring a personal vehicle, a commercial fleet, or a business property, understanding these factors lets you stop guessing and start making choices that protect both your assets and your budget.

Table of Contents

- Key takeaways

- Explaining insurance rating factors: the personal side

- How asset and location factors shape your rates

- Insurer financial strength ratings vs. your personal risk rating

- Coverage design as a rating factor you control

- My take on what policyholders consistently get wrong

- See how Diamondbackins puts this knowledge to work

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Personal factors are powerful but manageable | Age and claims history shape premiums significantly, but credit scores and driving records can be improved over time. |

| Location risk is often overlooked | Your property or vehicle’s location affects premiums through crime rates, climate exposure, and proximity to fire services. |

| Insurer ratings measure financial strength | AM Best and similar agencies rate an insurer’s ability to pay claims, not the cost of your individual policy. |

| Coverage design changes your premium | Deductible levels, coverage limits, and optional add-ons are levers you control to balance cost against protection. |

| Shopping with knowledge pays off | Understanding rating criteria helps you compare quotes accurately and choose coverage that fits your actual risk profile. |

Explaining insurance rating factors: the personal side

Every insurance policy starts with you. Insurers assess who you are before they assess what you own, and personal characteristics feed directly into their risk models.

Age is the most visible personal factor. Teenagers pay over $10,000 annually for car insurance on average, compared to roughly $2,400 for a 50-year-old. Premiums drop steadily after age 25, stay relatively flat between 30 and 60, and then rise again past 70 as accident rates climb. If you run a trucking or transportation business, this directly affects your payroll costs when adding young drivers to a commercial policy.

Driving experience is a separate calculation. A 35-year-old who only got their license two years ago will pay more than a 35-year-old with a 15-year clean record. Experience modifies risk independently of age, which means recently licensed commercial drivers represent a real cost to your fleet premium regardless of how mature they appear on paper.

Credit-based insurance scores are one of the most misunderstood factors affecting insurance premiums. These are not your FICO score. Late payments and high credit utilization create a separate insurance score that lowers your standing with carriers and raises your premium for several years, even after you’ve corrected the underlying credit issues. Most states allow carriers to use these scores. California, Massachusetts, and a small number of others restrict the practice. If you’re operating in a state where it applies, monitoring your credit behavior is a direct way to influence your insurance costs over time.

Claims and violation history carry significant weight. Carriers treat prior claims as a forward-looking indicator of future losses, not just a record of what happened. A single at-fault accident typically affects your rate for three to five years. Multiple violations compound the effect. For commercial operators, driver motor vehicle records become part of the fleet’s overall risk picture, and each driver’s history feeds into the policy’s premium calculation process.

Pro Tip: Review your drivers’ motor vehicle records every six months, not just at renewal. A violation that drops off one driver’s record can meaningfully lower your fleet’s premium at the next policy cycle.

How asset and location factors shape your rates

The second category of insurance rating criteria moves from who you are to what you’re insuring and where it lives.

Vehicle and property characteristics

For commercial auto and trucking insurance, the type of vehicle matters enormously. A new semi-truck with advanced collision avoidance technology costs less to insure per unit than an older model without safety systems, assuming comparable use. Repair costs, replacement parts availability, and the vehicle’s safety rating all feed into the premium calculation. Carriers look at the cargo the truck carries, its operating radius, and how many miles it runs annually. Each variable adds or reduces expected loss.

For property coverage, construction type, roof age, and building materials are the primary factors. A steel and concrete commercial warehouse carries different fire and structural risk than a wood-frame building of the same square footage. A newer structure built to current codes receives favorable treatment compared to an older building that predates modern requirements.

The location premium nobody talks about

Location drives insurance costs in ways most policyholders don’t fully account for. Properties far from fire stations typically face surcharges of 15 to 25 percent, and that applies to commercial properties as much as residential ones. Climate exposure matters too. Coastal properties and those in flood plains, wildfire zones, or hail corridors face persistently rising premiums as catastrophe models are updated.

The table below shows how location variables interact with asset type to shape commercial insurance rating:

| Location factor | Effect on premium | Example |

|---|---|---|

| Distance from fire station | 15-25% surcharge possible | Rural warehouse vs. urban facility |

| High-crime ZIP code | Increased theft/vandalism loading | Urban lot vs. suburban storage yard |

| Flood or wildfire zone | Significant surcharge or exclusion | Coastal depot vs. inland terminal |

| Local litigation environment | Higher liability premium | High-verdict states vs. low-verdict states |

For trucking businesses, the states where you operate also change your premium profile. States with high jury verdicts, more aggressive regulatory environments, or heavy traffic density push liability rates up. Understanding trucking insurance rates by state is a legitimate strategy for route planning, not just a curiosity.

Insurer financial strength ratings vs. your personal risk rating

This is where most consumers get genuinely confused, and the confusion can cost them in ways they don’t anticipate.

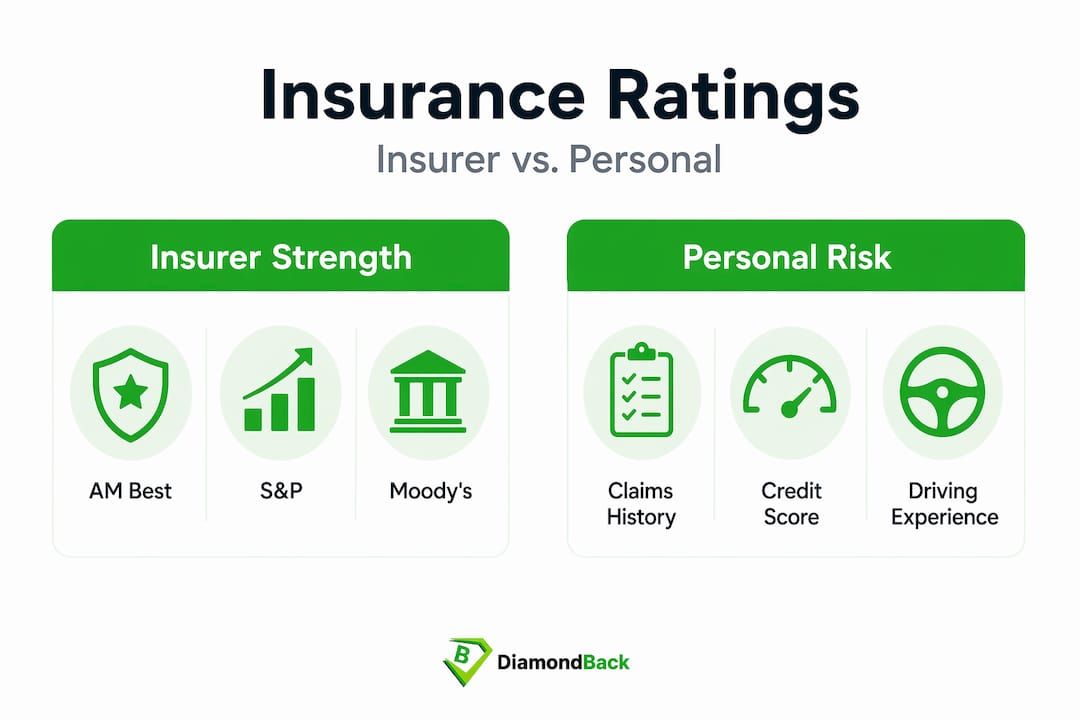

There are two completely different types of insurance ratings. One measures the insurer’s financial health. The other measures your personal or business risk profile. They operate on separate scales and serve different purposes, but people frequently conflate them.

Insurer financial strength ratings from agencies like AM Best, S&P, and Moody’s tell you whether a carrier has the reserves to pay claims when a large loss occurs. An AM Best A+ rating means the insurer has excellent capacity to meet its obligations. These ratings do not directly change your premium. A carrier rated A++ is not automatically cheaper or more expensive than one rated A. What the rating does is reduce your risk of choosing an insurer that fails to pay out when you actually need them.

The table below summarizes what the main agencies measure and how their scales work:

| Rating agency | Top rating | What it measures |

|---|---|---|

| AM Best | A++ | Insurance-specific financial strength |

| S&P Global | AAA | General creditworthiness and claims capacity |

| Moody’s | Aaa | Financial stability and default risk |

For commercial trucking operations, choosing a well-rated carrier matters because claims on large commercial policies can take months to resolve. A financially weak insurer may delay or dispute claims when cash reserves are stretched. Financial strength ratings should be part of your vetting process when comparing quotes, not an afterthought.

Your personal or business risk rating, by contrast, is the internal classification an underwriter assigns based on your driving record, claims history, credit score, vehicle type, and other factors. This classification is what determines your actual premium. Only 10 to 20 percent of applicants qualify for the top preferred tier, which reflects significantly better risk profiles and the lowest available premiums. Most people land in standard or substandard tiers, where premiums are higher and coverage terms may be more restrictive.

Pro Tip: Always ask for the financial strength rating of any carrier you’re considering. A quick look at AM Best’s public database takes under two minutes and tells you something no quote comparison page will show you automatically.

Coverage design as a rating factor you control

Unlike age or location, your coverage choices are entirely within your control. This is the category of insurance pricing factors where deliberate decisions make the biggest difference.

How deductibles work against premiums. A higher deductible reduces your premium because you’re absorbing more of the first loss yourself. Higher deductibles lower premiums while increasing your out-of-pocket exposure when a claim occurs. For a fleet operator with healthy cash reserves and a low annual claims frequency, a higher deductible can generate real savings. For a small owner-operator running tight margins, it can become a financial problem after a single incident.

Here’s a practical sequence for evaluating your coverage design:

- Calculate your realistic out-of-pocket capacity before selecting a deductible. If you can absorb a $5,000 loss without disrupting operations, a $5,000 deductible may make sense financially.

- Set liability limits above the minimum required by law. Minimum state requirements are rarely adequate for commercial operations. A single serious accident can generate claims that exceed minimum limits by a wide margin.

- Audit optional add-ons annually. Cargo coverage, non-trucking liability, and trailer interchange agreements each serve specific purposes. Paying for an add-on you no longer need is a direct waste.

- Review coverage structure at every renewal. Your fleet, your routes, and your risk profile change over time. The coverage choices that affect your premium should reflect your current operation, not last year’s.

The key insight here is that coverage design interacts with your fixed rating factors. A driver with a substandard risk rating can partially offset their higher base premium by choosing a higher deductible and tightly scoped coverage limits, provided their financial position supports it. The balance between protection and cost is yours to manage. Learn more about the specific factors affecting truck insurance premiums to see how these variables interact in commercial contexts.

My take on what policyholders consistently get wrong

I’ve spent enough time working through insurance pricing conversations to recognize the pattern. Most people walk into a renewal focused on the premium number and nothing else. They see a higher quote and assume something went wrong. They see a lower quote and assume they’re getting a deal. Neither assumption is reliable.

What I find consistently underappreciated is the interaction between factors. Your credit-based insurance score, your claims history, and your vehicle type don’t add up in a straight line. They feed into a model that weights each factor differently depending on the product and the carrier. Two insurers can look at the same risk and price it 30 percent apart because their models weight location or credit differently. That’s why shopping multiple carriers isn’t just about finding the cheapest number. It’s about finding the carrier whose rating model works in your favor given your specific profile.

I also see businesses ignore insurer financial strength until after a claim dispute. By then it’s too late to choose differently. The time to care about whether your carrier has an A+ from AM Best is before you sign, not when you’re waiting months for a large loss to be resolved.

The factor most trucking businesses can actually move is their claims and driver record profile. Investing in driver safety programs, telematics, and proactive vehicle maintenance genuinely reduces the frequency and severity of claims over time. That translates directly into premium savings at renewal. No other single investment has as clear a return in insurance terms.

— Vladimir

See how Diamondbackins puts this knowledge to work

Understanding insurance rating methodology is only useful when you can act on it. Diamondbackins makes that step straightforward for trucking and commercial fleet operators by aggregating quotes from multiple top-rated carriers in minutes.

When you compare quotes through Diamondbackins, you’re seeing how different carriers weigh your specific rating factors in real time. That means you can identify which insurer’s model works best for your driver profile, your fleet type, and your operating territory. Whether you need commercial trucking coverage in Georgia or instant coverage options in Virginia, the platform connects you to carriers whose ratings criteria align with your business profile. Get your quotes today and see exactly what your risk profile looks like across the market.

FAQ

What are insurance rating factors?

Insurance rating factors are the specific variables an insurer uses to calculate your premium, including personal characteristics, asset attributes, location, and coverage design choices. Together, these factors determine how much risk a carrier assigns to your policy.

How do credit scores affect insurance premiums?

Insurers use credit-based insurance scores, which are separate from your regular credit report, to assess risk. Late payments and high utilization lower this score and can raise your premium for several years.

What is the difference between insurer ratings and personal risk ratings?

Insurer financial strength ratings from agencies like AM Best measure a carrier’s ability to pay claims. Your personal risk rating is the internal classification that determines your individual premium and is based on your own record and profile.

Can I lower my insurance premium by changing coverage?

Yes. Adjusting your deductible, trimming unnecessary add-ons, and setting liability limits appropriate to your actual risk exposure are all ways to reduce your premium without changing your underlying risk profile.

Why do premiums vary so much by location?

Location affects premiums through crime rates, proximity to fire services, climate risk, and the local legal environment. Properties far from fire stations face surcharges of 15 to 25 percent, and high-verdict states push liability rates up across commercial lines.

Recommended

- Top factors affecting truck insurance rates in 2026

- Unveiling the Coverage Spectrum of General Liability Insurance with DiamondBack Insurance – Diamondback Insurance – Solutions with Instant Online Quotes

- Optimize your fleet: why reviewing insurance coverage saves money

- How insurers shape transportation risk and cost for fleets