Most trucking business owners assume their commercial truck policy will cover lost income if a fire, severe storm, or accident forces them to shut down. That assumption can be dangerously costly. Business interruption insurance (BI) is a separate and specific coverage that protects your revenue and ongoing expenses when a covered event stops your operation, and understanding exactly how it works is one of the most important risk management decisions you can make as a fleet owner or manager. This article breaks down what BI insurance covers, how claims are triggered, and what practical steps you can take to protect your company’s financial stability.

Table of Contents

- What is business interruption insurance?

- What does business interruption insurance cover?

- How business interruption insurance works: Triggers, exclusions, and restoration period

- Business interruption insurance for trucking and logistics: Industry-specific extensions

- Best practices for filing a business interruption claim

- What most trucking companies overlook about business interruption insurance

- Protect your trucking business with the right insurance partner

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Covers lost income | Business interruption insurance pays for lost revenue and key expenses if your trucking business is disrupted by a covered event. |

| Requires physical damage | Most policies only cover losses from physical damage at your location or a connected supplier or customer site. |

| Includes industry extensions | Trucking businesses can add coverage for road closures, utility outages, and dependent properties by choosing BI policy extensions. |

| Document claims thoroughly | Keeping detailed financial records is essential for maximizing your BI insurance claim. |

| Policy wording matters | Work with a trucking insurance specialist to align your coverage with your actual business risks and operations. |

What is business interruption insurance?

Business interruption insurance is a form of coverage designed to replace income your business loses when operations are suspended because of a covered physical loss. For trucking companies, that means BI steps in to help pay your bills when a fire destroys your terminal, a tornado damages your warehouse, or a major equipment loss forces you to suspend dispatch. It does not replace the damaged property itself. That is what your commercial property coverage handles. BI fills the financial gap between when the damage happens and when you are back to normal operations.

As truckers’ insurance specialists consistently emphasize, the mechanics of BI are more precise than most operators expect. Coverage is generally triggered by a policy-defined event and is commonly tied to a “period of restoration,” which can include a waiting period before payments begin. That waiting period is often 48 to 72 hours, meaning you absorb the first day or two of loss before the policy pays out.

BI insurance commonly pays for lost revenue and certain continuing fixed costs, and may be paired with “extra expense” or mitigation costs. For a trucking company, fixed costs include ongoing loan payments on equipment, employee payroll for drivers and office staff, property rent or lease payments, and insurance premiums that continue whether your trucks are rolling or sitting idle. Extra expense coverage is equally valuable because it allows you to spend money to speed up your recovery, such as renting substitute equipment, leasing a temporary office, or paying expedited shipping fees to serve clients through a third party.

Understanding your insurance needs for trucking companies starts with recognizing that BI is not typically a standalone product. It is added to or bundled with a commercial property policy, and its limits and terms are directly shaped by your policy language.

What does business interruption insurance cover?

Now that we know what BI insurance is, let us explore what it actually covers in a real-world trucking context. The core of any BI policy is the replacement of lost business income. For a trucking operation, that means the net profit your business would have earned plus the fixed expenses you still owe, even with your trucks parked.

BI insurance commonly pays for both lost revenue and certain continuing fixed costs, and may be paired with “extra expense” or mitigation costs. The table below summarizes what BI typically covers and how each item applies to trucking operations.

| Coverage category | What it includes | Trucking example |

|---|---|---|

| Lost business income | Net profits lost during shutdown | Revenue from suspended freight routes |

| Fixed operating expenses | Rent, payroll, loan payments, taxes | Terminal lease, driver salaries, truck financing |

| Extra expenses | Costs to accelerate recovery | Equipment rental, temporary dispatch office |

| Civil authority coverage | Income lost due to government access restriction | Loss during a mandated road or facility closure |

| Contingent BI | Losses from a supplier or customer shutdown | Loading dock closure at a major shipper |

Imagine your trucking terminal suffers a serious fire. Roof damage and smoke contamination force you to close the facility for six weeks while repairs are completed. During that time, you still owe rent on the property, payroll to your administrative staff, and monthly loan payments on your fleet. BI coverage would pay those continuing fixed costs, along with the net profit you would have earned from freight runs. If you also choose to rent a temporary dispatch space to keep partial operations going, your extra expense coverage handles that cost as well.

Choosing the best insurance for your trucking operation involves more than just comparing premiums. It means understanding exactly which expenses your BI policy will recognize and which ones it will not. Some policies have sublimits on payroll or exclude certain categories of overhead, so reviewing the fine print with a specialist before you file a claim is essential.

Review how your policy is structured against your insurance requirements for trucking companies to confirm your limits are high enough to cover all your actual monthly fixed costs and a realistic income loss period.

Pro Tip: Before any loss occurs, prepare a spreadsheet listing every fixed expense your operation carries each month. Include loan payments, lease obligations, payroll by category, utility costs, and recurring vendor invoices. Having this document ready at claim time can dramatically speed up the adjustment process and support a stronger payout.

How business interruption insurance works: Triggers, exclusions, and restoration period

Understanding what BI insurance covers leads to a deeper question: when does it actually apply, and when doesn’t it? This is where many trucking business owners run into problems, because the trigger for a BI claim is more specific than most people assume.

Most BI policies require direct physical loss or damage to property. Many BI policies require direct physical loss or damage at the insured premises, or at relevant “dependent property” locations for contingent BI, so some shutdowns without covered physical damage are often excluded. This matters enormously for trucking companies facing disruptions that do not involve obvious property damage, such as a regulatory shutdown, a labor dispute, or a drop in freight demand.

Here is how the claim process typically unfolds for a covered loss:

- A covered peril, such as fire, windstorm, or vandalism, causes physical damage to your insured premises or dependent property.

- The damage forces a full or partial suspension of your business operations.

- Your waiting period begins. This is commonly 48 to 72 hours after the triggering event.

- Once the waiting period passes, BI payments begin to accrue daily.

- Coverage continues through the restoration period, which ends when repairs are complete or when your business could reasonably resume operations, whichever comes first.

- Extra expense reimbursements are submitted alongside your ongoing loss documentation.

Common exclusions you need to know include economic losses from market downturns or contract cancellations, losses from events that do not cause physical damage, losses from events specifically excluded by your policy such as floods without a flood endorsement, and losses caused by government-mandated closures that are not tied to physical damage. The COVID-19 pandemic exposed this exclusion for countless businesses across all industries.

Cyber risk is another emerging concern for transportation companies. Cyber policies may offer BI-like coverage, but standard property-based BI policies often do not cover income losses from a cyberattack unless a cyber endorsement is specifically added. If your dispatch system or fleet management software is compromised and shuts down your operation, you may find your standard BI policy offers no protection without that endorsement.

Working with trucking insurance experts to review your policy language is not optional. It is a fundamental part of protecting your business. When you compare insurance providers for trucking companies, make sure you ask specifically about cyber endorsements and whether your policy requires physical damage as a trigger.

Pro Tip: Read the definition of “covered cause of loss” in your BI policy carefully. If that section does not explicitly include cyber events, utility failures, or government orders, your coverage for those scenarios is likely absent or severely limited.

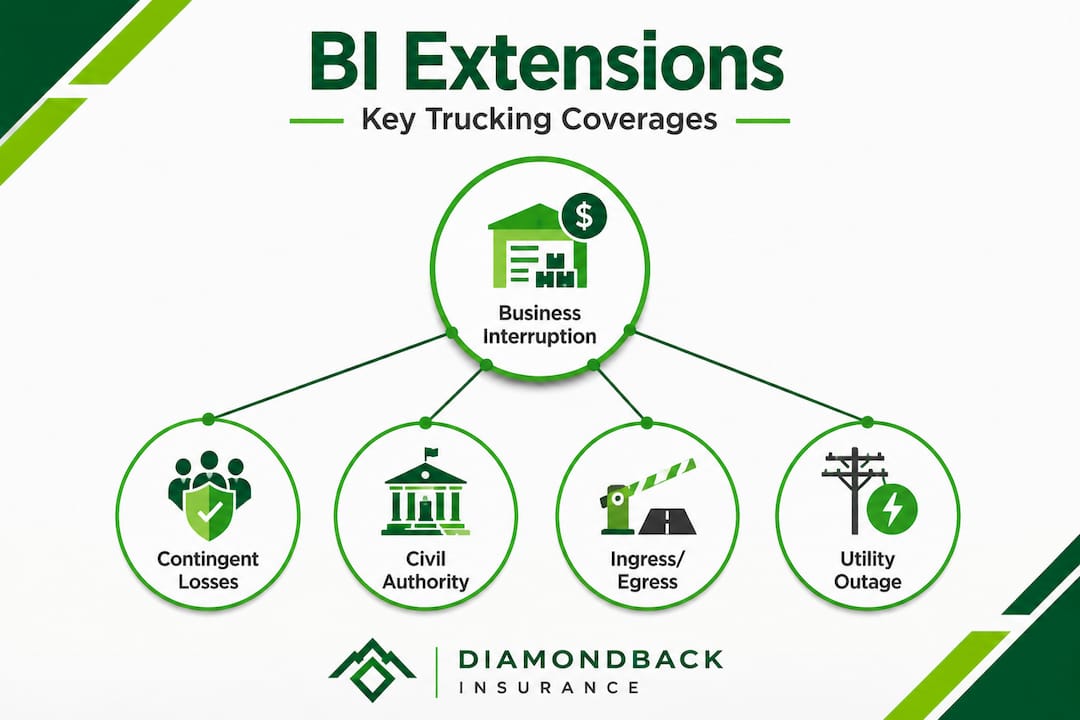

Business interruption insurance for trucking and logistics: Industry-specific extensions

Having reviewed general triggers, let us highlight BI features designed specifically for the complexities of trucking and logistics. The transportation sector faces unique disruption risks that standard BI policies may not address without targeted extensions. Fortunately, several endorsements exist to close those gaps.

In trucking and transportation risk management, BI concepts matter when operations or access are disrupted, but buyers need to understand how physical-damage triggers and endorsements apply. Here is a breakdown of the most relevant extensions for your operation.

Contingent business interruption. This extension covers income losses when a key supplier, customer, or dependent property suffers a covered physical loss. For a trucking company, this could mean a major shipper’s warehouse burns down and you lose a contract worth thousands of dollars per week.

Civil authority coverage. If a government agency, such as a fire marshal or emergency management office, restricts access to your facility because of a covered event at a nearby property, civil authority coverage pays your lost income during that restriction period. This is particularly relevant for trucking terminals located near industrial zones.

Ingress and egress coverage. Your terminal may be undamaged, but if road damage or debris blocks the only access routes, your operation still grinds to a halt. Ingress and egress coverage protects against exactly that scenario.

Utility service interruption. Power outages, water main breaks, or loss of natural gas can disable refrigerated storage or disrupt your facility. A utility service interruption extension can cover losses caused by those events, even when the outage originates off your property.

Knowing which of these extensions are attached to your current policy is part of a responsible risk management review. Protect your trucking business by auditing your existing coverage for these endorsements before a disruption forces the question.

Best practices for filing a business interruption claim

Knowing your coverage extensions is only half the battle. Here is how to maximize your benefit if you need to make a claim. The single most common reason BI claims fall short is inadequate pre-loss documentation. Insurers calculate your lost income by comparing what your business actually earned against what it would have earned without the interruption. If your financial records are incomplete, inconsistent, or hard to reconstruct, that calculation works against you.

BI claims can be disputed and hinge on claim documentation and adjustment methodology, for example, projecting revenue using financial history and selecting the baseline trend period. That means the time frame your insurer uses to project your pre-loss revenue trend can significantly affect your payout. If your business was growing fast in the months before a loss, you want that growth reflected in the projection. Disputes over this methodology are common and can be costly if you are unprepared.

Follow these steps to strengthen your claim:

- Assess the scope of the disruption immediately and note the date and time of the triggering event.

- Notify your insurer as soon as possible. Most policies require prompt notice, and delays can jeopardize coverage.

- Document all physical damage with photographs, repair estimates, and contractor invoices.

- Compile financial records including the past two to three years of tax returns, profit and loss statements, and monthly revenue reports.

- Track all extra expenses separately, keeping every receipt and vendor invoice from the moment operations are disrupted.

- Consider hiring a public adjuster or claims consultant if the loss is large or if your insurer disputes the revenue projection methodology.

“The strength of a BI claim is directly tied to the quality of the financial and operational records supporting it. Businesses that document proactively recover faster and more completely.”

Trucking insurance claims guidance from experienced professionals can make a measurable difference in the final settlement amount. Do not wait until a loss occurs to understand the claims process.

Pro Tip: Begin organizing your records at the very first sign of a potential disruption, even before the loss is fully confirmed. Early documentation protects your timeline and prevents memory gaps that adjusters may use to challenge your claim.

What most trucking companies overlook about business interruption insurance

Here is the perspective that most articles skip over. Trucking operators invest significant time comparing liability limits and physical damage deductibles, but many give BI coverage only a cursory review. The result is a dangerous coverage gap that only becomes visible at exactly the worst moment.

The most critical misunderstanding is this: BI is not simply a policy that pays whenever your trucks are not running. A recurring underwriting and claims nuance is that BI is not simply “economic loss from downtime.” Courts and insurers often require that the downtime be legally caused by a covered peril as defined in the policy wording. That distinction has denied legitimate-feeling claims for countless businesses, from small carriers to large fleets.

The lesson is straightforward but important. Policy intent and policy language are not the same thing. You might reasonably assume your BI coverage kicks in whenever a major disruption halts your operation, but if that disruption does not meet the exact definition of a covered cause of loss in your specific policy, coverage will not apply. Insurers are not being unreasonable when they deny these claims. They are enforcing the contract you agreed to.

The solution is to work with a specialist who can audit your actual operations against your policy wording, identify the gaps, and recommend specific endorsements to address them. Insuring your trucking company correctly is not a one-time transaction. It is an ongoing process of aligning your coverage to the real risks your business faces.

Protect your trucking business with the right insurance partner

Business interruption insurance is one of the most misunderstood yet most financially critical coverages available to trucking companies. Getting it right requires more than a standard policy review. It means understanding triggers, exclusions, restoration periods, and the extensions that apply specifically to transportation operations.

At Diamondback Insurance, we make it simple to compare trucking insurance explained options from multiple top-rated carriers in one place. Whether you need to close a BI coverage gap, add a contingent BI extension, or review your full fleet program, our platform lets you find trucking insurance companies and compare quotes instantly. Working with the right insurance partners for truckers means your operation has a complete risk management foundation, not just basic compliance coverage.

Frequently asked questions

Does business interruption insurance require physical damage to my property?

Many BI policies require direct physical loss or damage at the insured premises, so most standard policies only pay when a covered physical event such as a fire or storm affects your property or a dependent location.

How long does business interruption insurance coverage last?

Coverage is generally triggered by a policy-defined event and tied to a period of restoration, so coverage typically starts after a short waiting period and ends when repairs are complete or your business could reasonably reopen.

Can business interruption insurance cover losses from a power outage or road closure?

Yes, if your policy includes the right endorsements. BI-related extensions such as ingress and egress coverage and utility service interruption can apply to transportation logistics operations when those specific events are included in your policy.

What are extra expenses in a BI claim for truckers?

Extra expenses are costs you incur to keep your operation running or recover faster during a covered disruption. Mitigation-related items like temporary relocation, expedited shipping, and rental equipment are common examples that BI policies with extra expense coverage will reimburse.

How can I make a stronger BI insurance claim?

Keep detailed financial records going back at least two to three years and document all losses and extra expenses from the first day of the disruption. Projected revenue baselines are built from prior financial records, and disputes can occur over methodology choices, so the stronger your documentation, the better your position.