Many fleet managers assume cargo insurance is just a legal checkbox, but that assumption can cost you a load, a relationship with a broker, or even your operating authority. The truth is that cargo insurance is one of the most nuanced and consequential protections your trucking business carries. Understanding what it covers, what the real-world requirements look like, and how to choose the right type for your operation can mean the difference between a recoverable loss and a business-ending one. This guide breaks down everything you need to know clearly and practically.

Table of Contents

- What is cargo insurance?

- Cargo insurance requirements and industry standards

- Types of cargo insurance and endorsements

- Avoiding costly cargo insurance mistakes

- Our take: Building a smarter cargo insurance strategy

- Fleet insurance solutions and next steps

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cargo insurance protects shipments | It covers loss, damage, theft, or destruction while goods are in transit and in your care. |

| Legal minimums vs. industry standards | Federal law only mandates minimum coverage for household goods, but most brokers require $100,000+ for all shipments. |

| Right endorsements matter | Refrigerated and high-value loads need specific endorsements to ensure full protection. |

| Premiums decrease with safe operations | Cargo insurance costs drop after two years of clean claims history, rewarding safe operation. |

| Avoid common mistakes | Underinsuring, skipping endorsements, and ignoring renewal dates can put your business at risk. |

What is cargo insurance?

Cargo insurance is the policy that protects the freight your trucks carry. When goods are damaged in an accident, stolen from a truck stop, or destroyed by a fire, cargo insurance is what steps in to cover that financial loss. Without it, you are personally responsible for the value of every load you haul.

The technical name you will often see is motor truck cargo insurance. As defined for truckers, this is a specialized policy that protects trucking companies, fleet managers, and owner-operators from financial losses due to damage, loss, theft, or destruction of goods while in their care, custody, and control during transit. The phrase “care, custody, and control” matters. It means your liability begins the moment freight is in your possession and does not end until the receiver signs for it.

It helps to understand this policy as separate from physical damage coverage or general liability. Trucking insurance explained as a whole package covers multiple risks, but cargo insurance specifically addresses the value of the goods being transported rather than the truck itself or third-party bodily injury claims.

What risks does cargo insurance typically cover?

The scope of coverage depends on the policy type you choose, but standard cargo policies generally protect against physical damage during transit, vehicle accidents that destroy or damage freight, theft and hijacking, loading and unloading incidents, and fire or extreme weather events. Some policies also cover cargo insurance basics like refrigeration breakdown for temperature-sensitive goods, though that usually requires a specific endorsement.

Who actually needs this coverage? If you haul freight for others under your authority, cargo insurance is essential. Owner-operators leased to a carrier may be covered under the carrier’s policy, but you should confirm this in writing. Fleet managers running multiple trucks need to verify that the per-vehicle and per-occurrence limits in their policy actually reflect the value of loads they regularly accept.

Understanding what transportation insurance includes in your overall coverage picture makes it easier to identify gaps before a claim reveals them. Now that you know cargo insurance is a vital shield for your shipments, let’s explore what minimum coverage the law and logistics partners actually require.

Cargo insurance requirements and industry standards

Here is where a lot of fleet managers run into trouble. They assume that because there is no universal federal mandate for cargo insurance on general freight, they can skip it or carry minimal amounts. That assumption is wrong in practice.

Federal requirements specify that the FMCSA mandates minimum cargo coverage of $5,000 per vehicle and $10,000 per occurrence only for household goods movers. For general freight carriers, there is no federal minimum. But that legal detail does not protect you from the market reality: nearly every freight broker and shipper requires a minimum of $100,000 in cargo coverage, and loads involving electronics, pharmaceuticals, or other high-value commodities often require $250,000 or more.

Legal minimums vs. industry expectations: a direct comparison

| Category | Legal minimum | Broker/shipper standard | High-value freight |

|---|---|---|---|

| Household goods | $5,000/vehicle, $10,000/occurrence | $100,000+ | $250,000+ |

| General freight | None federally required | $100,000 minimum | $250,000+ |

| Hazardous materials | Varies by commodity | $1,000,000+ | Negotiated per load |

| Refrigerated goods | None federally required | $100,000 minimum | $250,000+ with endorsement |

The gap between legal and practical requirements is wide. You can be technically compliant with federal law and still be disqualified from hauling most commercial freight because your limits do not satisfy broker requirements. This reality makes understanding fleet insurance requirements far more valuable than just reading the FMCSA rule book.

How to meet broker and shipper requirements

Meeting the industry standard is a process, not a one-time purchase. Start by reviewing the requirements of every broker you currently work with or plan to approach. Second, confirm your current policy limits and compare them to those requirements. Third, identify any commodity exclusions in your existing policy, since certain goods like fine art, tobacco, or cash are routinely excluded. Fourth, ask your insurer about increasing limits or adding endorsements before bidding on new lanes. Fifth, keep your certificate of insurance current and accessible, because brokers will request it before dispatching a load.

Working with established trucking insurance companies that specialize in freight operations makes this process faster and more reliable. They understand import cargo insurance types and domestic requirements and can flag gaps before they cost you a contract.

With a clearer sense of coverage requirements, you can better evaluate options. Next, let’s break down different types of cargo insurance and how to choose what is right for your operation.

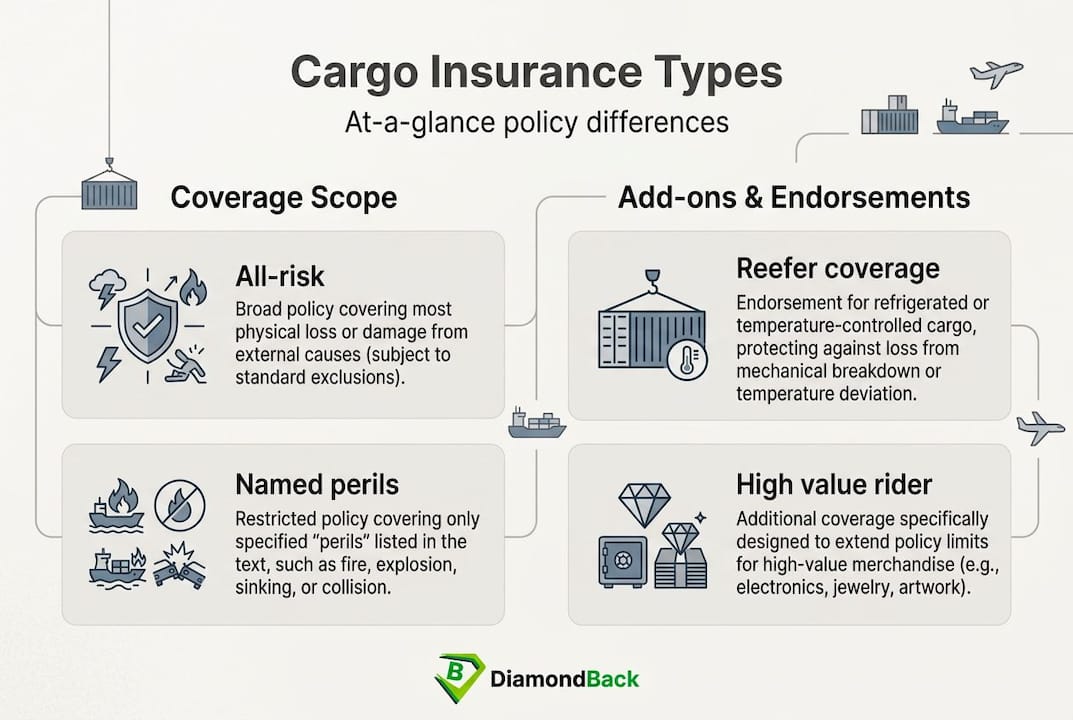

Types of cargo insurance and endorsements

Not all cargo policies are built the same. Choosing the wrong type means paying for coverage that does not match your actual risk, or worse, filing a claim only to discover your policy excludes the cause of loss.

All-risk coverage is the broadest policy available. It covers any cause of loss unless specifically excluded in the policy language. For fleet managers hauling diverse freight across multiple lanes, all-risk coverage gives the widest net of protection and reduces the chance of a claim being denied on a technicality.

Named perils coverage lists specific events that are covered, such as fire, collision, or theft. If the cause of loss is not on the list, the policy does not respond. This type is generally less expensive, but the lower premium reflects narrower protection. It can make sense for carriers hauling low-risk, low-value goods consistently.

Reefer-specific coverage is a critical category that many new operators overlook. Standard cargo policies do not cover spoilage caused by mechanical refrigeration breakdown. A reefer-specific endorsement must be added to the policy explicitly. Without it, a mechanical failure that ruins a $40,000 load of produce or frozen meat is entirely your financial responsibility.

High-value endorsements apply when the standard coverage limit falls short of the actual load value. If your policy covers up to $100,000 but you accept a $175,000 load of electronics, you need an endorsement or a separate policy to cover the gap. Always compare your policy limit to the declared value of each shipment before accepting a load.

Coverage type comparison

| Coverage type | Scope | Cost relative to all-risk | Best for |

|---|---|---|---|

| All-risk | Broadest, fewer exclusions | Baseline (highest) | Diverse freight, mixed lanes |

| Named perils | Specific causes only | 20-40% less | Consistent, low-risk freight |

| Reefer endorsement | Temperature/spoilage events | Added to base policy | Refrigerated cargo haulers |

| High-value endorsement | Excess value protection | Varies by load value | Electronics, pharma, jewelry |

How your operating history affects your premiums

Your costs are not fixed. New operations pay 40-100% more in premiums compared to established carriers initially, but that gap typically shrinks after two years of clean claims history. This means the investments you make in safety, driver training, and proper cargo handling today directly lower your insurance costs over time.

Pro Tip: When you add a reefer endorsement or high-value rider, ask your insurer to walk through the exact triggering conditions. Some reefer endorsements only activate if breakdown is mechanical, not if the driver failed to set the temperature correctly. Knowing the difference before a claim saves significant frustration.

Understanding your coverage options sets you up to avoid costly mistakes. Let’s look at how to sidestep common pitfalls and maximize value.

Avoiding costly cargo insurance mistakes

Even experienced fleet managers make errors that lead to denied claims, coverage gaps, or lost contracts. Most of these mistakes are preventable when you know what to look for.

Under-insuring your freight is the most common and damaging error. If your policy limit is $100,000 and you regularly haul loads worth $150,000, you are self-insuring that $50,000 gap every time you roll. Review your average load values annually and adjust your limits accordingly. The cost of increasing limits is almost always less than the cost of absorbing a partial loss.

Skipping the reefer endorsement continues to catch new operators off guard. Carriers assume their base cargo policy covers everything on the truck, including temperature-sensitive loads. It does not. Without the specific endorsement, spoilage from refrigeration failure is entirely out-of-pocket. This mistake is especially costly because produce and pharmaceutical loads often carry the highest per-pound values.

Misunderstanding commodity exclusions is another frequent issue. Most cargo policies exclude certain goods entirely, including tobacco, alcohol, electronics above a certain threshold, fine art, and currency. If you haul any excluded commodity without a supplemental policy or endorsement, you have no coverage. Always read the exclusions section of your policy before accepting new types of freight.

Letting coverage lapse during renewal creates a dangerous gap. Some fleet managers assume their coverage auto-renews without checking the terms. If a load is in transit during a lapsed period and damage occurs, the claim will be denied. Understanding how to file a shipment insurance claim is useful, but staying current on renewals prevents the need to file a claim with no coverage in place.

Carrying less than brokers require is a business-limiting mistake. Brokers will verify your certificate of insurance before dispatching loads. If your coverage does not meet their threshold, you lose the contract. Getting passed over repeatedly for loads because of inadequate limits is a slow, invisible drain on revenue that many small operators do not connect to their insurance decisions.

Pro Tip: Set a calendar reminder 60 days before your policy renewal date. Use that window to review your current limits against your last 12 months of load values, check your claims history, and compare insurance quotes to make sure you are getting competitive pricing. Waiting until renewal week leaves you no time to negotiate.

Finding the best trucker insurance match for your fleet means going beyond price and evaluating whether the coverage actually fits your operation’s specific freight types and lanes. Now that you know what to avoid, let’s look at a broader perspective on how fleet managers should approach cargo insurance this year.

Our take: Building a smarter cargo insurance strategy

The trucking industry tends to treat cargo insurance as a compliance item. You get what the broker requires, you file the certificate, and you move on. We think that approach leaves real money and real risk on the table.

Meeting the broker minimum of $100,000 keeps you in the game, but it is not a strategy. It is a floor, not a plan. Consider what actually happens when a $200,000 load of medical equipment is damaged and your policy only responds up to $100,000. You absorb half the loss, you face a lawsuit from the shipper, and your insurance relationship may take a hit at renewal. The better approach is to understand your actual freight exposure and set limits that reflect it, not limits that simply satisfy a form requirement.

Clean operations do more than keep your drivers safe. They build a claims history that insurers reward with lower premiums and better terms over time. Carriers who invest in driver training, GPS monitoring, and secure load practices are not just reducing accidents. They are building a financial track record that unlocks access to better pricing and more profitable lanes. Your insurance needs for your fleet will evolve as you grow, and carriers with clean records have far more flexibility in how they structure their coverage.

The lowest premium is rarely the best value. A policy that saves you $1,200 per year but excludes reefer spoilage, caps coverage at $75,000, and has a slow claims response process is a liability in disguise. We always recommend reviewing coverage terms alongside price rather than sorting by price alone.

Finally, audit your endorsements every year. The freight you haul today may be different from what you hauled two years ago. If you have added refrigerated loads, high-value commodities, or new states to your operating area, your policy needs to reflect those changes. Endorsements and riders should be reviewed as part of your annual renewal process, not added reactively after a claim is denied.

Fleet insurance solutions and next steps

Whether you are reviewing current policies or starting fresh, having the right tools and guidance makes cargo insurance decisions faster and less stressful.

At Diamondback Insurance, we help fleet managers and small business owners move through the insurance process efficiently without sacrificing coverage quality. You can read our trucking insurance guide to build a strong foundation, then get fleet insurance quotes from multiple top-rated insurers in minutes. If you are looking for coverage that fits your location and operation type, explore local commercial truck insurance options tailored to your region. Protecting your cargo starts with understanding your options, and we make that easier every step of the way.

Frequently asked questions

Is cargo insurance required by law for every shipment?

Cargo insurance is only federally mandated for household goods movers, but most brokers and shippers require coverage for all freight shipments regardless of legal mandates.

What does cargo insurance typically cover?

Cargo insurance covers damage, loss, theft, or destruction of goods during transit when the freight is in the carrier’s care, custody, and control.

How much cargo coverage do brokers and shippers expect?

Most brokers require at least $100,000 in cargo coverage as a baseline, and shipments involving high-value goods typically require $250,000 or more.

Do refrigerated (reefer) loads need special cargo insurance endorsements?

Yes. Without a reefer-specific endorsement, spoilage caused by refrigeration failure is not covered, and those losses come directly out of your pocket.

Can my cargo insurance costs decrease over time?

Absolutely. New operations initially pay 40-100% more in premiums, but carriers with two or more years of clean claims history typically see meaningful reductions in their rates.